Daniel J. Duffy - Numerical Methods in Computational Finance

Здесь есть возможность читать онлайн «Daniel J. Duffy - Numerical Methods in Computational Finance» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Numerical Methods in Computational Finance

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Numerical Methods in Computational Finance: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Numerical Methods in Computational Finance»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Part A Mathematical Foundation for One-Factor Problems

Chapters 1 to 7 introduce the mathematical and numerical analysis concepts that are needed to understand the finite difference method and its application to computational finance.

Part B Mathematical Foundation for Two-Factor Problems

Chapters 8 to 13 discuss a number of rigorous mathematical techniques relating to elliptic and parabolic partial differential equations in two space variables. In particular, we develop strategies to preprocess and modify a PDE before we approximate it by the finite difference method, thus avoiding ad-hoc and heuristic tricks.

Part C The Foundations of the Finite Difference Method (FDM)

Chapters 14 to 17 introduce the mathematical background to the finite difference method for initial boundary value problems for parabolic PDEs. It encapsulates all the background information to construct stable and accurate finite difference schemes.

Part D Advanced Finite Difference Schemes for Two-Factor Problems

Chapters 18 to 22 introduce a number of modern finite difference methods to approximate the solution of two factor partial differential equations. This is the only book we know of that discusses these methods in any detail.

Part E Test Cases in Computational Finance

Chapters 23 to 26 are concerned with applications based on previous chapters. We discuss finite difference schemes for a wide range of one-factor and two-factor problems.

This book is suitable as an entry-level introduction as well as a detailed treatment of modern methods as used by industry quants and MSc/MFE students in finance. The topics have applications to numerical analysis, science and engineering.

More on computational finance and the author’s online courses, see www.datasim.nl.

Numerical Methods in Computational Finance — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Numerical Methods in Computational Finance», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

We state this theorem in more general terms: consistency and stability of a multistep scheme are sufficient for convergence.

Finally, the discussion in this section is also applicable to systems of ODEs. For more discussions, we recommend Henrici (1962) and Lambert (1991).

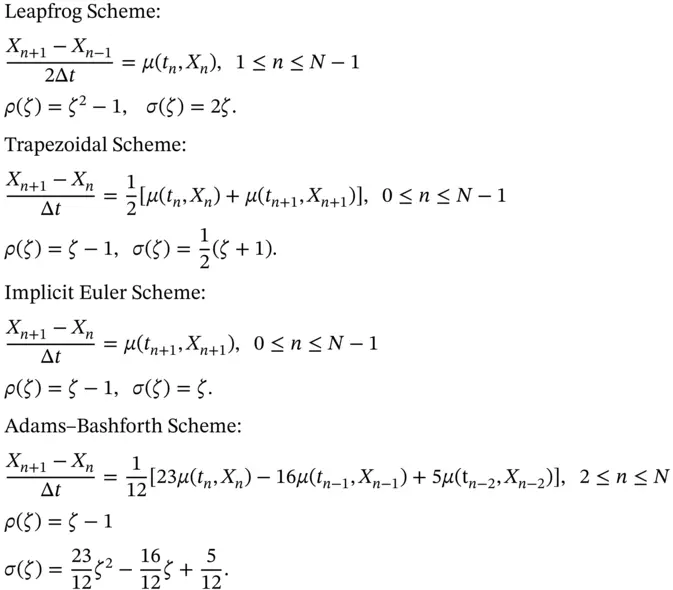

Finally, we present four finite difference schemes for the IVP (2.31)and their generating polynomials as defined by Equations (2.34):

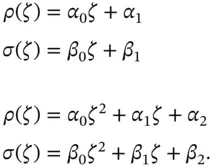

We recommend that you verify the results using the forms of the generating polynomials for one-step and two-step methods, respectively. The general forms are:

2.6 STIFF ODEs

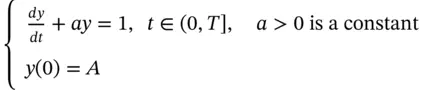

We now discuss special classes of ODEs that arise in practice and whose numerical solution demands special attention. These are called stiff systems whose solutions consist of two components; first, the transient solution that decays quickly in time, and second, the steady-state solution that decays slowly. We speak of fast transient and slow transient , respectively. As a first example, let us examine the scalar linear initial value problem:

(2.40)

whose exact solution is given by:

In this case the transient solution is the exponential term, and this decays very fast (especially when the constant a is large) for increasing t . The steady-state solution is a constant, and this is the value of the solution when t is infinity. The transient solution is called the complementary function , and the steady-state solution is called the particular integral (when  ), the latter including no arbitrary constant. The stiffness in the above example is caused when the value a is large; in this case traditional finite difference schemes can produce unstable and highly oscillating solutions. One remedy is to define very small time steps. Special finite difference techniques have been developed that remain stable even when the parameter a is large. These are the exponentially fitted schemes , and they have a number of variants. The variant described in Liniger and Willoughby (1970) is motivated by finding a fitting factor for a general initial value problem and is chosen in such a way that it produces an exact solution for a certain model problem. To this end, let us examine the scalar ODE:

), the latter including no arbitrary constant. The stiffness in the above example is caused when the value a is large; in this case traditional finite difference schemes can produce unstable and highly oscillating solutions. One remedy is to define very small time steps. Special finite difference techniques have been developed that remain stable even when the parameter a is large. These are the exponentially fitted schemes , and they have a number of variants. The variant described in Liniger and Willoughby (1970) is motivated by finding a fitting factor for a general initial value problem and is chosen in such a way that it produces an exact solution for a certain model problem. To this end, let us examine the scalar ODE:

(2.41)

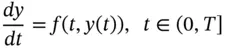

and let us approximate it using the Theta method :

(2.42)

where the parameter  has not yet been specified. We determine it using the heuristic that this so-called Theta method should be exact for the linear constant-coefficient model problem :

has not yet been specified. We determine it using the heuristic that this so-called Theta method should be exact for the linear constant-coefficient model problem :

(2.43)

Based on this heuristic and by using the exact solution from (2.43)in scheme (2.42)  , we get the value (you should check that this formula is correct; it is a bit of algebra). We get:

, we get the value (you should check that this formula is correct; it is a bit of algebra). We get:

(2.44)

Note: this is a different kind of exponential fitting.

We need to determine if this scheme is stable (in some sense). To answer this question, we introduce some concepts.

Definition 2.3The region of (absolute) stability of a numerical method for an initial value problem is the set of complex values  for which all discrete solutions of the model problem (2.43)remain bounded when n approaches infinity.

for which all discrete solutions of the model problem (2.43)remain bounded when n approaches infinity.

Definition 2.4A numerical method is said to be A-stable if its region of stability is the left-half plane, that is:

Returning to the exponentially fitted method, we can check that it is A-stable because for all  we have

we have  , and this condition can be checked using the scheme (2.42)for the model problem (2.43).

, and this condition can be checked using the scheme (2.42)for the model problem (2.43).

We can generalise the exponential fitting technique to linear and non-linear systems of equations. In the case of a linear system, stiffness is caused by an isolated real negative eigenvalue of the matrix A in the equation:

(2.45)

where  and A is a constant

and A is a constant  matrix with eigenvalues

matrix with eigenvalues  and eigenvectors

and eigenvectors

The solution of Equation (2.45)is given by:

where  are arbitrary constants and

are arbitrary constants and  is a particular integral. In this case we can employ exponential fitting by fitting the dominant eigenvalues which can be computed by the Power method , for example.

is a particular integral. In this case we can employ exponential fitting by fitting the dominant eigenvalues which can be computed by the Power method , for example.

Интервал:

Закладка:

Похожие книги на «Numerical Methods in Computational Finance»

Представляем Вашему вниманию похожие книги на «Numerical Methods in Computational Finance» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Numerical Methods in Computational Finance» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.