John A. Tracy - Accounting For Dummies

Здесь есть возможность читать онлайн «John A. Tracy - Accounting For Dummies» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Accounting For Dummies

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Accounting For Dummies: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Accounting For Dummies»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Accounting For Dummies

Accounting For Dummies — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Accounting For Dummies», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

The cost of goods sold or cost of sales expense and the selling, general, and administrative expenses take the biggest bites out of sales revenue. The other three expenses (interest, income tax, and other expenses) are relatively small as a percent of annual sales revenue but are important enough in their own right to be reported separately. And though you may not need this reminder, bottom-line profit (net income) is the amount of sales revenue in excess of the business’s total expenses. If either sales revenue or any of the expense amounts are wrong, then profit is wrong.

A service business does not sell products; therefore, it doesn’t have the traditional cost of goods sold expense (as it is not selling any tangible goods). In place of cost of goods sold, a service business often simply refers to the direct costs as costs of sales, which generally capture labor expenses for wages, payroll taxes, benefits, and other expenses that directly vary with sales revenue. Most service businesses are labor intensive; they have relatively large labor costs as a percent of sales revenue. Service companies differ in how they report their operating expenses. For example, United Airlines breaks out the cost of aircraft fuel and landing fees. The largest expense of the insurance company State Farm is payments on claims. The movie chain AMC reports film exhibition costs separate from its other operating expenses. We offer these examples to remind you that accounting should always be adapted to the way the business operates and makes profit. In other words, accounting should follow the business model.

A service business does not sell products; therefore, it doesn’t have the traditional cost of goods sold expense (as it is not selling any tangible goods). In place of cost of goods sold, a service business often simply refers to the direct costs as costs of sales, which generally capture labor expenses for wages, payroll taxes, benefits, and other expenses that directly vary with sales revenue. Most service businesses are labor intensive; they have relatively large labor costs as a percent of sales revenue. Service companies differ in how they report their operating expenses. For example, United Airlines breaks out the cost of aircraft fuel and landing fees. The largest expense of the insurance company State Farm is payments on claims. The movie chain AMC reports film exhibition costs separate from its other operating expenses. We offer these examples to remind you that accounting should always be adapted to the way the business operates and makes profit. In other words, accounting should follow the business model.

Income statement pointers

Most businesses break out one or more expenses instead of disclosing just one very broad category for all selling, general, and administrative expenses. For example, Apple, in its 2020 consolidated income statement, discloses research and development expenses separate from its selling, general, and administrative expenses. A business could disclose expenses for advertising and sales promotion, salaries and wages, research and development (as does Apple), and delivery and shipping — though reporting these expenses varies quite a bit from business to business. Businesses do not disclose the compensation of top management in their external financial reports, although this information can be found in the proxy statements of public companies that are filed with the Securities and Exchange Commission (SEC). In summary, the extent of details disclosed about operating expenses in externally reported financial reports varies quite a bit from business to business. Financial reporting standards are rather permissive on this point.

Most businesses break out one or more expenses instead of disclosing just one very broad category for all selling, general, and administrative expenses. For example, Apple, in its 2020 consolidated income statement, discloses research and development expenses separate from its selling, general, and administrative expenses. A business could disclose expenses for advertising and sales promotion, salaries and wages, research and development (as does Apple), and delivery and shipping — though reporting these expenses varies quite a bit from business to business. Businesses do not disclose the compensation of top management in their external financial reports, although this information can be found in the proxy statements of public companies that are filed with the Securities and Exchange Commission (SEC). In summary, the extent of details disclosed about operating expenses in externally reported financial reports varies quite a bit from business to business. Financial reporting standards are rather permissive on this point.

Inside most businesses, a profit statement is called a P&L (profit and loss) report. These internal profit performance reports to the managers of a business include more detailed information about expenses and about sales revenue — a good deal more! Reporting just five expenses to managers (as shown in Figure 2-1) would not do. Chapter 13explains P&L reports to managers.

Sales revenue refers to sales of products or services to customers. In some income statements, you also see the term income, which generally refers to amounts earned by a business from sources other than sales. For example, a real estate rental business receives rental income from its tenants. (In the example in this chapter, the business has only sales revenue.)

The income statement gets the most attention from business managers, lenders, and investors (not that they ignore the other two financial statements). The much-abbreviated versions of income statements that you see in the financial press, such as in The Wall Street Journal, report the top line (sales revenue and income) and the bottom line (net income) and not much more. Refer to Chapter 6for more information on income statements.

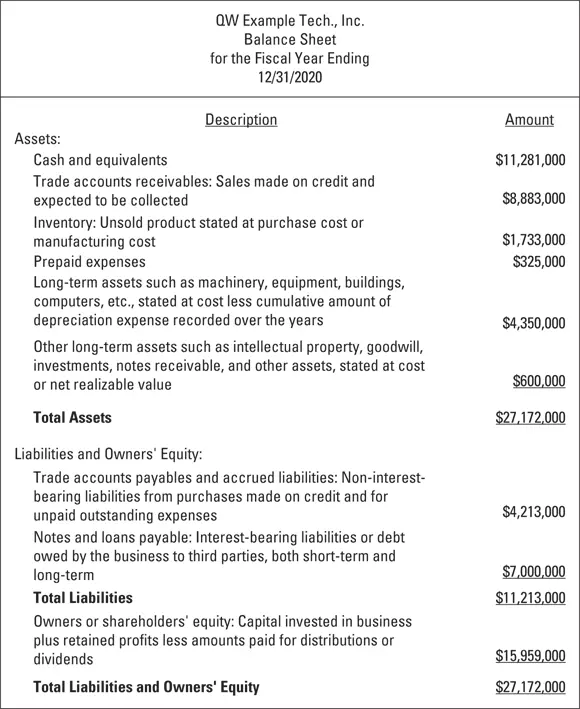

The Balance Sheet

A more accurate name for a balance sheet is statement of financial condition or statement of financial position, but the term balance sheet has caught on, and most people use this term. The most important thing is not the “balance” but rather the information reported in this financial statement.

In brief, a balance sheet summarizes on the one hand the assets of the business and on the other hand the sources of the assets. However, looking at assets is only half the picture. The other half consists of the liabilities and owner equity of the business. Cash is listed first, and other assets are listed in the order of their nearness to cash. Liabilities are listed in order of their due dates (the earliest first, and so on). Liabilities are listed ahead of owners’ equity. We discuss the ordering of the components in a balance sheet in Chapter 7.

Presenting the components of the balance sheet

Figure 2-2 shows the building blocks of a typical balance sheet for a business that sells products and services on credit. As mentioned, one reason the balance sheet is called by this name is that its two sides balance, or are equal in total amounts. In this example, the $27.172 million total assets equals the $27.172 million total liabilities and owners’ equity. The balance or equality of total assets on the one side of the scale and the sum of liabilities plus owners’ equity on the other side of the scale is expressed in the accounting equation, which we discuss in Chapter 1. Note: The balance sheet in Figure 2-2 shows the essential elements in this financial statement. In a financial report, the balance sheet includes additional features and frills, which we explain in Chapter 7.

© John Wiley & Sons, Inc.

FIGURE 2-2:Balance sheet information components for a technology business that sells products and services on credit.

Take a quick walk through the balance sheet. For a technology company that sells products and services on credit, assets are reported in the following order: First is cash, then receivables, then cost of products held for sale, and finally the long-term operating assets of the business. Moving to the other side of the balance sheet, the liabilities section starts with the trade liabilities (from buying on credit) and liabilities for unpaid expenses. Following these operating liabilities is the interest-bearing debt of the business. Owners’ equity sources are then reported below liabilities. So a balance sheet is a composite of assets on one hand and a composite of liabilities and owners’ equity sources on the other hand.

A balance sheet is a reflection of the fundamental two-sided nature of a business (expressed in the accounting equation, which we discuss in Chapter 1). In the most basic terms, assets are what the business owns, and liabilities plus owners’ equity are the sources of the assets. The sources have claims against the assets. Liabilities and interest-bearing debt have to be paid, of course, and if the business were to go out of business and liquidate all its assets, the residual after paying all its liabilities would go to the owners.

A company that sells services doesn’t have an inventory of products being held for sale. A service company may or may not sell on credit. Airlines don’t sell on credit, for example. If a service business doesn’t sell on credit, it won’t have two of the sizable assets you see in Figure 2-2: receivables from credit sales and inventory of products held for sale. Generally, this means that a service-based business doesn’t need as much total assets compared with a products-based business with the same size sales revenue.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Accounting For Dummies»

Представляем Вашему вниманию похожие книги на «Accounting For Dummies» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Accounting For Dummies» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.