John A. Tracy - Accounting For Dummies

Здесь есть возможность читать онлайн «John A. Tracy - Accounting For Dummies» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Accounting For Dummies

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Accounting For Dummies: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Accounting For Dummies»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Accounting For Dummies

Accounting For Dummies — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Accounting For Dummies», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

The financial statements of a business do not present a “history” of the business. Financial statements are, to a large extent, limited to the recent profit performance and financial condition of the business. A business may add some historical discussion and charts that aren’t strictly required by financial reporting standards. (Public corporations that have their ownership shares and debt traded in open markets are subject to various disclosure requirements under federal law, including certain historical information.)

The financial statements of a business do not present a “history” of the business. Financial statements are, to a large extent, limited to the recent profit performance and financial condition of the business. A business may add some historical discussion and charts that aren’t strictly required by financial reporting standards. (Public corporations that have their ownership shares and debt traded in open markets are subject to various disclosure requirements under federal law, including certain historical information.)

The illustrative financial statements that follow in this part and Part 2do not include a historical narrative of the business. Nevertheless, whenever you see financial statements, we encourage you to think about the history of the business. To help you out in this regard, here are some particulars about the business example we use in this chapter:

It sells products and services to other businesses (not on the retail level).

It sells on credit, and its customers take approximately a month or so before they pay.

It holds a fairly large stock of products awaiting sale.

It owns a wide variety of long-term operating assets that have useful lives from 3 to 30 years or longer (building, machines, tools, computers, office furniture, goodwill, intellectual property, and so on).

It has been in business for many years and has made a profit most years.

It borrows money for part of the total assets it needs.

It’s organized as a corporation and pays federal and state income taxes on its annual taxable income.

It has never been in bankruptcy and is not facing any immediate financial difficulties.

The following sections present the company’s annual income statement for the year just ended, its balance sheet at the end of the year, and its statement of cash flows for the year.

Looking at other aspects of reporting financial statements

Dollar amounts in financial statements are typically rounded off, either by not presenting the last three digits (when rounded to the nearest thousand) or by not presenting the last six digits (when rounded to the nearest million). We strike a compromise on this issue: We show the last three digits for each item as 000, which means that we rounded off the amount but still show all digits. Many smaller businesses report their financial statement dollar amounts to the last dollar or even the last penny, for that matter. Keep in mind that having too many digits in a dollar amount makes it hard to comprehend.

Dollar amounts in financial statements are typically rounded off, either by not presenting the last three digits (when rounded to the nearest thousand) or by not presenting the last six digits (when rounded to the nearest million). We strike a compromise on this issue: We show the last three digits for each item as 000, which means that we rounded off the amount but still show all digits. Many smaller businesses report their financial statement dollar amounts to the last dollar or even the last penny, for that matter. Keep in mind that having too many digits in a dollar amount makes it hard to comprehend.

The financial statements in this chapter are more in the nature of an outline. Actual financial statements use only one- or two-word account titles on the assumption that you know what all these labels mean. What you see in this chapter, on the other hand, are the basic information components of each financial statement. We explain the full-blown, classified, detailed financial statements in Part 2. (We know you’re eager to get to those chapters.) In this chapter, we offer descriptions for each financial statement element rather than the terse and technical account titles you find in actual financial statements. Also, we strip out subtotals that you see in actual financial statements because they aren’t necessary at this point.

Oops! We forgot to mention a few things about financial reports. Financial reports are rather stiff and formal. No slang or street language is allowed, and we’ve never seen a swear word in one. Financial statements would get a G in the movies rating system. Seldom do you see any graphics or artwork in a financial statement itself, although you do see a fair amount of photos and graphics on other pages in the financial reports of public companies. And there’s virtually no humor in financial reports. However, we might mention that Warren Buffett, in his annual letter to the stockholders of Berkshire Hathaway, includes some wonderful humor to make his points.

The Income Statement

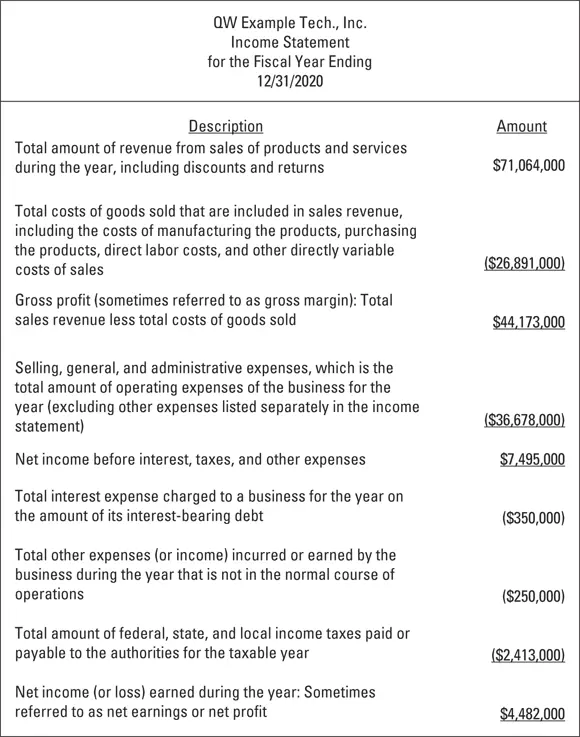

First on the minds of financial report readers is the profit performance of the business. The income statement is the all-important financial statement that summarizes the profit-making activities of a business over a period of time. Figure 2-1 shows the basic information content of an external income statement for our company example. External means that the financial statement is released outside the business to those entitled to receive it — primarily its shareowners and lenders. Internal financial statements stay within the business and are used mainly by its management; they aren’t circulated outside the business because they contain competitive and confidential information.

Presenting the components of the income statement

Figure 2-1 presents the major ingredients, or information packets, in the income statement for a technology company that sells products and services. As you may expect, the income statement starts with sales revenue on the top line. There’s no argument about this, although in the past, certain companies didn’t want to disclose their annual sales revenue (to hide the large percent of profit they were earning on sales revenue).

Sales revenue is the total amount that has been or will be received from the company’s customers for the sales of products and services to them. Simple enough, right? Well, not really. The accounting profession is currently reexamining the technical accounting standards for recording sales revenue, and this has proven to be a challenging task. Our business example, like most businesses, has adopted a certain set of procedures for the timeline of recording its sales revenue.

Recording expenses involves much more troublesome accounting problems than revenue problems for most businesses. Also, there’s the fundamental question regarding which information to disclose about expenses and which information to bury in larger expense categories in the external income statement. We say much more about expenses in later chapters. At this point, direct your attention to the five kinds of expenses in Figure 2-1. Expenses are deducted from sales revenue to determine the final profit for the period, which is referred to as the bottom line. Actually, the preferred label is net income, as you see in the figure.

The five expense categories you see in Figure 2-1 should almost always be disclosed in external income statements. These constitute the minimum for adequate disclosure of expenses. The cost of goods sold or cost of sales (for service companies) is just what it says: the cost of the products sold or services delivered to customers. The cost of the products or services delivered should be matched against the revenue from the sales, of course.

© John Wiley & Sons, Inc.

FIGURE 2-1:Income statement information components for a technology company that sells products and services.

Only one conglomerate operating expense has to be disclosed. In Figure 2-1, it’s called selling, general, and administrative expenses, which is a popular title in income statements. This is an all-inclusive expense total that mixes together many kinds of expenses, including administrative employee wages and benefit costs, advertising expenses, depreciation of assets, and so on. But it doesn’t include interest expenses, income tax expenses, or other expenses; these three expenses are generally reported separately in an income statement.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Accounting For Dummies»

Представляем Вашему вниманию похожие книги на «Accounting For Dummies» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Accounting For Dummies» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.