The Digital Transformation of Logistics

Здесь есть возможность читать онлайн «The Digital Transformation of Logistics» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:The Digital Transformation of Logistics

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

The Digital Transformation of Logistics: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «The Digital Transformation of Logistics»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

The book is divided into three themed-sections:

Technologies

The Digital Transformation of Logistics: Demystifying Impacts of the Fourth Industrial Revolution

Platforms

The Digital Transformation of Logistics: Demystifying Impacts of the Fourth Industrial Revolution,

People

The Digital Transformation of Logistics: Demystifying Impacts of the Fourth Industrial Revolution

The Digital Transformation of Logistics: Demystifying Impacts of the Fourth Industrial Revolution

The Digital Transformation of Logistics — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «The Digital Transformation of Logistics», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

New Entrants Threaten Status Quo

Where larger outsourced logistics companies have already offshored many of their back‐office functions to shared service centers, there is now an effort to automate those same functions, and medium‐sized logistics companies now are directly comparing outsourcing with automation. As the cost of these documentation, coordination, and billing tasks, which had previously been done in the more expensive labor consumer nations, decreases, so will the margin on the overall price arbitrage. These previously low‐ and mid‐skill‐level positions who had been dependent on labor inputs will be offshored or automated.

Aggressive competition and agile startups will seize market share by reducing their selling rates. This is hypothetically made possible in highly automated and technologically savvy companies that have little overhead and a low marginal cost. It is also worth noting that startups chasing market share and revenue, while ignoring profitability in hopes of raising seed capital, have the potential to impact things as well. As an example, Morgan Stanley's analysis of Uber Freight, a platform designed to facilitate the movement of cargo by matching truck drivers with cargo owners, shows that Uber Freight is giving 99% of its revenue back to its throughput carriers and keeping only a 1% margin for itself (Aouad 2019). This is a prime example of how a hub economy, and in this case a sharing economy company, is crossing industry segments and threatening the role of domestic trucking brokers just as it did with the taxi industry.

The impacts of technology on logistics from a product perspective are worth examining. The US trucking industry, estimated at $700 billion, still uses “phone, fax, and email as primary methods of connecting”; however companies like Transfix are building online marketplaces to remove that inefficiency (McAfee and Brynjolfsson 2017). Since 2017, there has been a boom in companies offering the same services from Uber Freight to Next Trucking. Many warehousing companies sit on excess space in which Flexe, a Seattle‐based company, is looking to optimize by offering a platform for those companies to rent that space out (McAfee and Brynjolfsson 2017). The Neighbor application has taken that a step further, and now anyone can rent the extra space in their home (Holder 2019). These new products are causing major disruptions for logistics companies in the same way the Uber and Netflix have disrupted the transportation and television industries while also maintaining low overhead costs. These new entrants are pushing logistic companies to respond by increasing technological capabilities to offer similar products and customer experiences.

Disintermediation Threat Looming

The rise of Uber Freight and many others like it through the supply chain and logistics ecosystem should frighten logistics companies as the comparison with a travel agency is strikingly real. Disintermediation, defined as suppliers dealing directly with customers and eliminating the needless cost and interaction of an intermediary, happened in the travel agency as the number of sales went 80% online within seven years of its commercial and technological enablement (Dodu, 2008). Whether it is expedia.comor Uber Freight, there is a lesson to be learned. Freight forwarders must move up the value stream. Beneficial cargo owners (BCOs), otherwise known as the direct customers of logistics and freight forwarding companies, typically have limited knowledge on evaluating different carrier options and even less experience dealing with all the formalities involved in booking directly (Gasparik et al. 2017); therefore the value that a freight forwarder provides is in the knowledge that they have in terms of carrier and customs (Burkovskis 2008). The ultimate value that they offer is in being a single source of information and a centralized window to provide their clients with the services and relevant information needed to move a shipment (Gasparik et al. 2017).

The challenge remains on how to move that centralized point away from phone calls and emails to a more efficient medium that offers system connectivity and instant access. The first step in the digitalization journey for logistics companies is not abundantly clear as often they are heavily reliant on outside stakeholders, including customers, governments, and vendors. With $1.5 trillion of value at play in the logistics industry, there is an influx of new players, and incumbents are scrambling to figure out their strategy (Gould 2018).

Navigating a Digital Transformation

Budget Considerations for Technological Upgrades

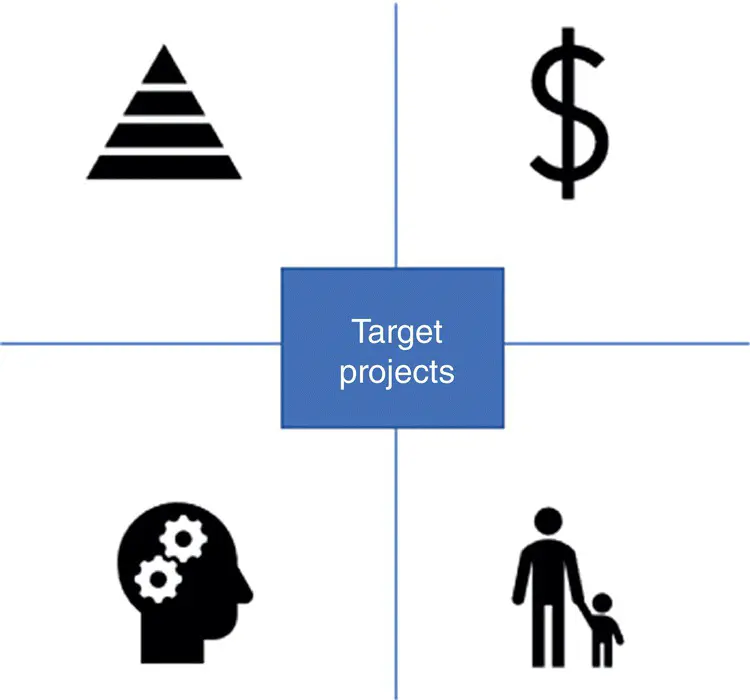

Struggling with where to start and how to keep their business afloat, talent‐strapped logistics companies must face the difficult discussion of where the money will come from to fund their digitalization journey. Logistics is a fixed cost heavy business in that there are many pass‐through costs, which are generally much higher than the final margin, and therefore there are inherent risks if things go wrong. Profit in the logistics industry is quite low compared with the sharing economy companies mentioned above. Even within the logistics industry, there is a large gap between the courier/express/parcel (CEP) companies who could have double‐digit EBIT margins compared with the logistics service providers whose profitability is usually between −1% and 8%(Tipping and Kauschke 2016). The necessity of logistics as it facilitates the movement of goods around the world and the inability for one company to control each step along that supply chain will ensure that logistics providers have a vital role for the foreseeable future. Logistics companies need to focus on projects that are within their control where they have the foundations in place, the budget to realistically invest, the talent to drive, and lastly, the permissions from shareholders to execute (see Figure 1.2).

Figure 1.2 Target digitalization projects.

Shipment coordination is necessary, and for a long time, it was a profitable business to buy space along the chain and resell it at a higher rate by offering an integrated seamless solution to the world's market. The ability to move goods efficiently in and out of international markets independent of the distance but dependent on the speed, quality, and price of coordination determines the value of logistics (Tseng et al. 2005). In other words, logistics companies are not going to get an injection of additional margin from their customers to facilitate this digital transformation; this will need to be a capital expense that will be recouped through either reducing payroll, which often means cutting high‐paid executive staff, or procuring from their suppliers at a lower rate.

Lessons Learned from Other B2B Industries

A multitude of traditional service industry businesses has been disrupted by the advancements of technologies associated with cloud computing, faster processing power, and the beginnings of AI through sophisticated algorithmic filtering processes. From international logistics to international communication, there will continue to be further economic growth, and new markets emerge as supply‐side gains will enable efficiency that will lead to reduced costs (Schwab 2015). For example, there has been a large shift in the way that the publishing, taxi, hotel, finance, music, movie, and travel agency businesses all operate as they fight to compete against their zero marginal cost platform model competitors.

Automation Leading in Terms of Return on Investment

Интервал:

Закладка:

Похожие книги на «The Digital Transformation of Logistics»

Представляем Вашему вниманию похожие книги на «The Digital Transformation of Logistics» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «The Digital Transformation of Logistics» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.