Maria Cristina Mariani - Data Science in Theory and Practice

Здесь есть возможность читать онлайн «Maria Cristina Mariani - Data Science in Theory and Practice» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Data Science in Theory and Practice

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Data Science in Theory and Practice: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Data Science in Theory and Practice»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

will also earn a place in the libraries of practicing data scientists, data and business analysts, and statisticians in the private sector, government, and academia.

Data Science in Theory and Practice — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Data Science in Theory and Practice», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

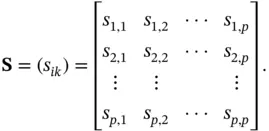

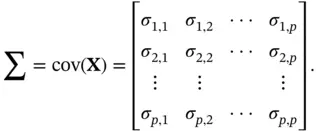

(3.1)

In ( 3.1), the covariance matrix consists of the variances of the variables along the main diagonal and the covariances between each pair of variables in the other matrix positions. The sample covariance of the  th and

th and  th variables,

th variables,  , is calculated using the

, is calculated using the  th and

th and  th columns of

th columns of  :

:

(3.2)

where  is the number of measurements.

is the number of measurements.

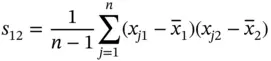

For example if  :

:

(3.3)

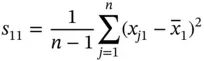

and if  :

:

(3.4)

we have the sample variance.

The sample covariance measures the association between the  th and

th and  th variables. The sample covariance reduces to the sample variance when

th variables. The sample covariance reduces to the sample variance when  as observed in ( 3.4). We note that the sample covariance matrix ( 3.1) is symmetric, i.e.

as observed in ( 3.4). We note that the sample covariance matrix ( 3.1) is symmetric, i.e.  for all

for all  and

and  because of its definition. Other names used for the covariance matrix are variance matrix, variance–covariance matrix, and dispersion matrix. In finance the concept of covariance is applied in portfolio theory, in the diversification method, that reduces the risk by choosing assets that do not present a high positive covariance with each other.

because of its definition. Other names used for the covariance matrix are variance matrix, variance–covariance matrix, and dispersion matrix. In finance the concept of covariance is applied in portfolio theory, in the diversification method, that reduces the risk by choosing assets that do not present a high positive covariance with each other.

If  is a random vector taking on any possible value in a multivariate population, the population covariance matrixis defined as

is a random vector taking on any possible value in a multivariate population, the population covariance matrixis defined as

(3.5)

Just like the sample covariance case defined in ( 3.1), the diagonal elements  are the population variances of the

are the population variances of the  's, and the off‐diagonal elements

's, and the off‐diagonal elements  are the population covariances of all possible pairs of

are the population covariances of all possible pairs of  s, i.e.

s, i.e.  for

for  .

.

The notation  for the covariance matrix is widely used and seems natural because

for the covariance matrix is widely used and seems natural because  is the uppercase version of

is the uppercase version of  .

.

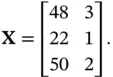

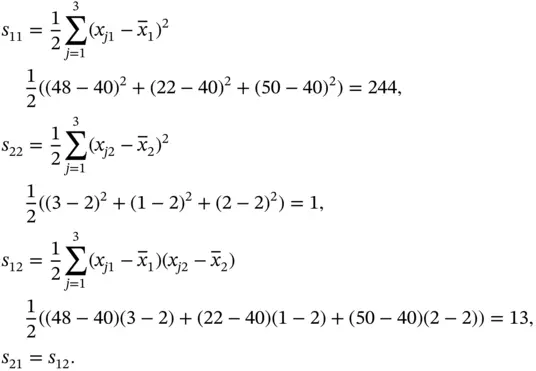

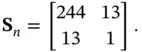

Example 3.3Consider the following data matrix introduced in Example 3.1:

Each receipt yields a pair of measurements, total dollar sales, and number of movies sold. Since there are three receipts, we have a total of three observations on each variable. We find the sample variances and covariance  as follows:

as follows:

Therefore,

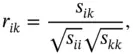

3.5 Correlation Matrices

A correlation matrix is a table showing correlation coefficients between variables. Correlation is a statistical technique that can show whether and how strongly pairs of variables are related. The sample correlation between the  th and

th and  th variables is defined as

th variables is defined as

(3.6)

Интервал:

Закладка:

Похожие книги на «Data Science in Theory and Practice»

Представляем Вашему вниманию похожие книги на «Data Science in Theory and Practice» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

![Роман Зыков - Роман с Data Science. Как монетизировать большие данные [litres]](/books/438007/roman-zykov-roman-s-data-science-kak-monetizirova-thumb.webp)

Обсуждение, отзывы о книге «Data Science in Theory and Practice» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.