Applied Modeling Techniques and Data Analysis 2

Здесь есть возможность читать онлайн «Applied Modeling Techniques and Data Analysis 2» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Applied Modeling Techniques and Data Analysis 2

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Applied Modeling Techniques and Data Analysis 2: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Applied Modeling Techniques and Data Analysis 2»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Applied Modeling Techniques and Data Analysis 2 — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Applied Modeling Techniques and Data Analysis 2», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

From Lorig et al . (2017), Lemma 3.4, we have

[2.11]

where

and where

is the m th Hermite polynomial.

We must still calculate the expression in the third line of equation [2.6]for h ≥ 2 (it is equal to 1 when h = 1). From Lorig et al . (2017), Proposition 3.5, we have

[2.12]

where the coefficients ch,h−2q are defined recursively by

Using equations [2.7]and [2.10], we explicitly calculate:

and

where the dots denote the terms containing  and

and  ∙ The functions

∙ The functions  take the form

take the form

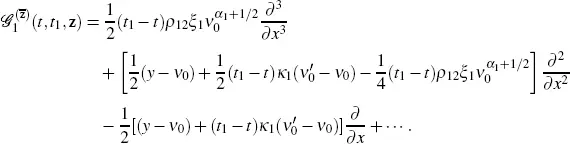

Equation [2.6]gives

Then,

and

As T → t and k → x, the second and third terms disappear. Calculating the derivative with respect to k , we obtain

and Theorem 2.2 follows.

PROOF OF THEOREM 2.3.-

Equation [2.6]takes the form

[2.13]

The sets I 2, h are I 2, 1= {(2)}, I 2, 2= {( 1, 1)}. We have a 11, 2(x,y,z) = 0. It follows that equation [2.10]with n = 2 includes only summation over the set I 2, 2and takes the form

While calculating the operator  using equation [2.8], we need to calculate only the coefficients of the three partial derivatives with respect to the variable x . We obtain

using equation [2.8], we need to calculate only the coefficients of the three partial derivatives with respect to the variable x . We obtain

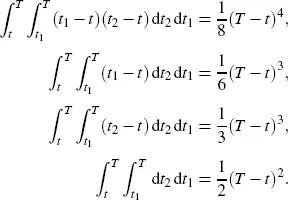

The following integrals are important for calculations:

The operator  takes the form

takes the form

Calculation of the first term on the right-hand side of equation [2.13]using equation [2.11]may be left to the reader.

Next, we calculate the left-hand side of equation [2.12]for h = 2. Using the Hermite polynomials H0(ζ) = 1, H1 (ζ) = 2ζ and H2(ζ) = 4ζ2 - 2, we obtain

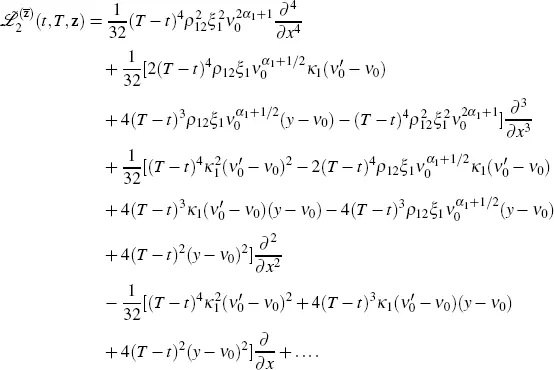

Combining everything together, we obtain the formula for

[2.14]

where the ellipsis denotes the terms satisfying the following condition: the limits of the term, its first partial derivative with respect to T and its first two partial derivatives with respect to k as ( T,k ) approaches ( t,x ) within  are all equal to 0.

are all equal to 0.

On the right-hand side of equation [2.14], the first term, the partial derivatives with respect to T of the second, fourth and sixth terms, the first partial derivative with respect to k of the third term, and the second partial derivative with respect to k of the fifth term give nonzero contributions to the right-hand side of the asymptotic expansion [2.4].

2.4. References

Gatheral, J. (2008). Consistent modelling of SPX and VIX options. The Fifth World Congress of the Bachelier Finance Society, London.

Latané, H.A. and Rendleman Jr., R.J. (1976). Standard deviations of stock price ratios implied in option prices. J. Finance, 31(2), 369–381.

Lorig, M., Pagliarani, S., Pascucci, A. (2017). Explicit implied volatilities for multifactor local-stochastic volatility models. Math. Finance , 27(3), 926–960.

Orlando, G. and Taglialatela, G. (2017). A review on implied volatility calculation. J. Comput. Appl. Math ., 320, 202–220.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Applied Modeling Techniques and Data Analysis 2»

Представляем Вашему вниманию похожие книги на «Applied Modeling Techniques and Data Analysis 2» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Applied Modeling Techniques and Data Analysis 2» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.