John E. Boylan - Intermittent Demand Forecasting

Здесь есть возможность читать онлайн «John E. Boylan - Intermittent Demand Forecasting» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Intermittent Demand Forecasting

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Intermittent Demand Forecasting: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Intermittent Demand Forecasting»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

The first text to focus on the methods and approaches of intermittent, rather than fast, demand forecasting

Intermittent Demand Forecasting No prior knowledge of intermittent demand forecasting or inventory management is assumed in this book. The key formulae are accompanied by worked examples to show how they can be implemented in practice. For those wishing to understand the theory in more depth, technical notes are provided at the end of each chapter, as well as an extensive and up-to-date collection of references for further study. Software developments are reviewed, to give an appreciation of the current state of the art in commercial and open source software.

“Intermittent demand forecasting may seem like a specialized area but actually is at the center of sustainability efforts to consume less and to waste less. Boylan and Syntetos have done a superb job in showing how improvements in inventory management are pivotal in achieving this. Their book covers both the theory and practice of intermittent demand forecasting and my prediction is that it will fast become the bible of the field.” —

, Professor, University of Nicosia, and Director, Institute for the Future and the Makridakis Open Forecasting Center (MOFC).

“We have been able to support our clients by adopting many of the ideas discussed in this excellent book, and implementing them in our software. I am sure that these ideas will be equally helpful for other supply chain software vendors and for companies wanting to update and upgrade their capabilities in forecasting and inventory management.”—

, VP, Research and Development, Blue Yonder.

“As product variants proliferate and the pace of business quickens, more and more items have intermittent demand. Boylan and Syntetos have long been leaders in extending forecasting and inventory methods to accommodate this new reality. Their book gathers and clarifies decades of research in this area, and explains how practitioners can exploit this knowledge to make their operations more efficient and effective.”—

, Professor Emeritus, Rensselaer Polytechnic Institute.

Intermittent Demand Forecasting — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Intermittent Demand Forecasting», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

(2.2)

The ordering cost is usually a fixed cost per order, reflecting such things as raising invoices, cost of the personnel working in relevant organisational departments (e.g. purchasing, supplier management), and transportation and logistics costs, depending on whether customers, suppliers, or both assume such expenses. The true ordering costs sometimes depend on the size of the replenishment orders. For example, if logistics and transportation costs are shared between customers and suppliers, then a large order would attract a higher cost than a smaller one. However, these costs are customarily assumed fixed for modelling purposes.

Different stock control policies balance ordering, holding, and backorder costs in different ways, depending on the priorities and constraints set in the system, resulting in different decisions as to how much to stock and how often to replenish. The policies most relevant to managing intermittent demand inventories are discussed in Section 2.5. In this section, we focus on two precursors of the operation of any policy, namely:

1 How often an accurate indication is available of the stock levels for a particular item (which depends on how the stock status is maintained).

2 How often a test for reordering is made, to determine whether an order should be placed or not.

These issues constitute fundamental decisions in inventory management, and are integral to the selection of an appropriate stock rule.

2.4.1 How Should Stock Records be Maintained?

With regard to the first question, there are only two ways of ‘posting’ the stock status records. One is to add receipts and to subtract sales as they occur. In this case, each transaction triggers an immediate updating of the status and, consequently, this type of control is known as ‘transactions reporting’ (Silver et al. 2017) or as a continuous recording system. The second method of updating the stock status records is to do it periodically so that an interval of time elapses between the moments at which the stock level is updated.

Once the stock status records have been updated, the inventory control system can then check the stock status against one or more inventory parameters, so that a decision can be made about when and how much to order. Inventory parameters are essentially control numbers that tell us what actions are required. For example, in certain inventory policies if the stock levels drop at, or below, some minimum critical point, most often called an order point, then a replenishment order will be placed. In this case, the order point is the inventory parameter of interest. We discuss inventory parameters in detail in Section 2.5.

It is important to consider the relationship between continuous recording of transactions and continuous review of inventory. It is certainly true that we cannot have continuous review without continuous recording. However, a continuous recording of each transaction does not necessarily mean that there will be a continuous review of the stock requirements. Porteus (1985, p. 145) commented, ‘What really matters is not how the inventory levels are monitored but the relationship between recognising that an order should be placed, placing the order, and receipt of that order. Many, if not most, transactions reporting systems are equivalent to periodic review systems.’ The same is true at the time of writing, over 30 years later. For example, if the inventory records are up to date online continuously but the orders to a given supplier are issued at the end of the day (or at the end of any unit time period) then the system is one of periodic review with inventory levels being reviewed once a day (or once per time period). Transactions reporting systems are often referred to as continuous review systems although, strictly speaking, they are not the same thing.

There are two fundamental differences between continuous and periodic review systems. These differences relate to the following: (i) what triggers a new test for reordering and (ii) the time interval over which uncertainties in demand need to be taken into account.

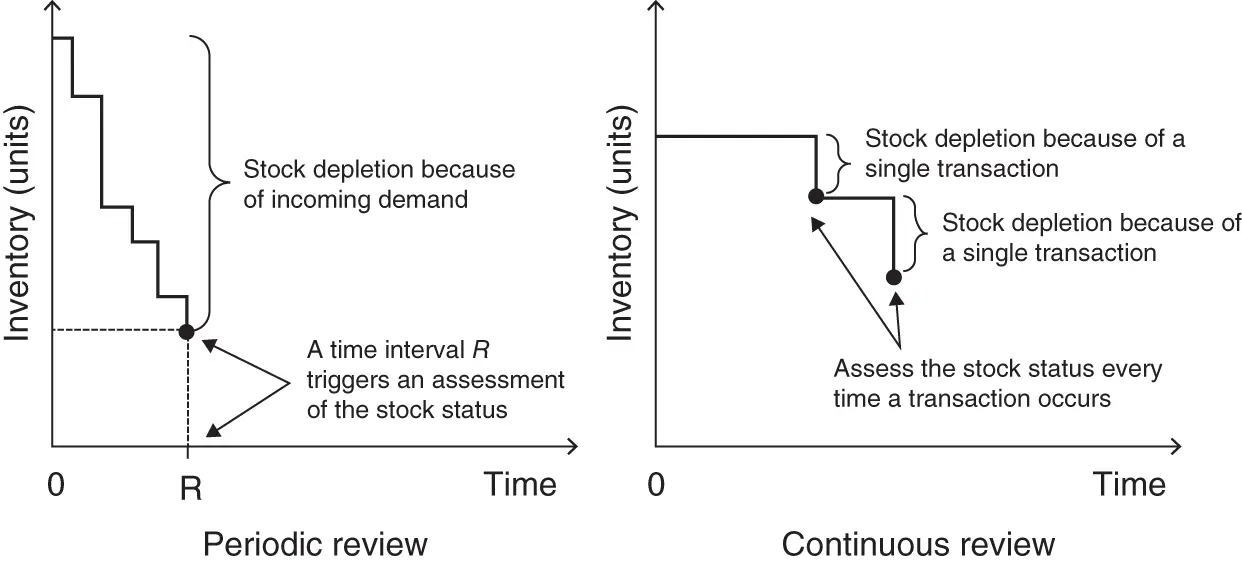

With regard to the former, in periodic review systems an elapsed fixed time interval (the review interval) is what triggers an assessment of the stock status to decide whether a replenishment order should be raised. The test for reordering is triggered by time‐interval considerations, and this is the reason why periodic review systems are also referred to as reorder interval systems. In continuous review systems, a reduction of the stock level (when a new transaction occurs, regardless of its magnitude) is what triggers the assessment of whether a new order should be placed on the supplier(s). So, the test for reordering is triggered by inventory level related considerations, and this is the reason why continuous review systems are also referred to as reorder level systems. The difference between the two types of systems is depicted graphically in Figure 2.2. This issue is further discussed in Section 2.4.2.

With regard to the time interval over which uncertainties need to be compensated, there are two major sources of uncertainty. The first one is that demand is ‘stochastic’. This means its occurrence and magnitude are subject to variations due to chance; demand can take on different values, each with an associated probability. This issue is discussed in detail in Chapter 4. Stochastic demand varies over time and is uncertain, and thus needs to be predicted. If demand were ‘deterministic’ (i.e. constant or non‐constant over time but known with certainty), then it would be straightforward to decide how much we need to keep in stock to satisfy future demands.

Figure 2.2 Periodic review and continuous review systems.

The second source of uncertainty relates to the passage of time during which uncertain demand poses a risk of a stockout. This time lapse differs between continuous and periodic review systems. For continuous review, it is the time interval between placing an order and the received order being available for customers. This time interval is called the lead time, of length  , and includes not only the external lead time (until receipt of order) but also the internal lead time (until availability for customers). (See Technical Note 2.3for further discussion.) If the lead time were zero, and inventory review continuous, then inventory control would be redundant because there would be no need to keep anything in stock. However, the lead time will never be zero in practice and so enough needs to be held in stock to satisfy demand from the point in time when an order is placed to the point in time when the order is received and available for customers.

, and includes not only the external lead time (until receipt of order) but also the internal lead time (until availability for customers). (See Technical Note 2.3for further discussion.) If the lead time were zero, and inventory review continuous, then inventory control would be redundant because there would be no need to keep anything in stock. However, the lead time will never be zero in practice and so enough needs to be held in stock to satisfy demand from the point in time when an order is placed to the point in time when the order is received and available for customers.

For continuous review, the lead time is called the protection interval, because stocks are held to protect against a stockout during that period of time. (See Technical Note 2.4for a discussion of an exception to this rule.) If the lead time is constant and known to be  , then we have the problem of forecasting stochastic demand over lead time (

, then we have the problem of forecasting stochastic demand over lead time (  ). So if the lead time is, say, two months then the uncertainty we need to account for every time we place an order is the magnitude of the demand over the subsequent two months. In many real‐world applications, the lead time varies, as demand does, contributing further to the uncertainty underlying the inventory control system. We assume for the time being (as often happens in practice when modelling inventories) that the lead time is known and constant, but we will relax this assumption in Chapter 7.

). So if the lead time is, say, two months then the uncertainty we need to account for every time we place an order is the magnitude of the demand over the subsequent two months. In many real‐world applications, the lead time varies, as demand does, contributing further to the uncertainty underlying the inventory control system. We assume for the time being (as often happens in practice when modelling inventories) that the lead time is known and constant, but we will relax this assumption in Chapter 7.

Интервал:

Закладка:

Похожие книги на «Intermittent Demand Forecasting»

Представляем Вашему вниманию похожие книги на «Intermittent Demand Forecasting» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Intermittent Demand Forecasting» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.