Michael M. Pompian - Behavioral Finance and Your Portfolio

Здесь есть возможность читать онлайн «Michael M. Pompian - Behavioral Finance and Your Portfolio» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Behavioral Finance and Your Portfolio

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Behavioral Finance and Your Portfolio: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Behavioral Finance and Your Portfolio»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

, acclaimed investment advisor and author Michael M. Pompian delivers an insightful and thorough guide to countering the negative effect of cognitive and behavioral biases on your financial decisions. You’ll learn about the “Big Five” behavioral biases and how they’re reducing your returns and leading to unwanted and unnecessary costs in your portfolio.

Designed for investors who are serious about maximizing their gains, in this book you’ll discover how to:

● Take control of your decision-making—even when challenging markets push greed and fear to intolerable levels

● Reflect on how to make investment decisions using data-backed and substantiated information instead of emotion and bias

● Counter deep-seated biases like loss aversion, hindsight and overconfidence with self-awareness and hard facts

● Identify your personal investment psychology profile, which you can use to inform your future financial decision making

Behavioral Finance and Your Portfolio

Behavioral Finance and Your Portfolio — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Behavioral Finance and Your Portfolio», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

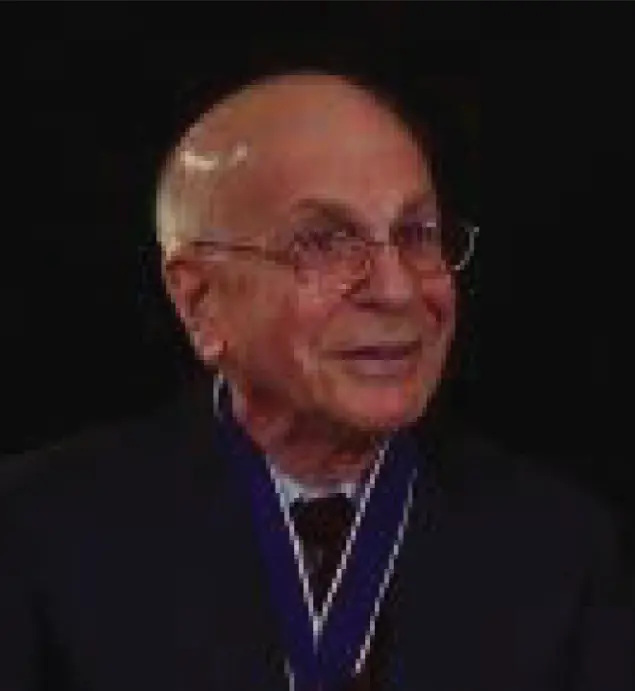

Figure 1.6 Daniel Kahneman, 2002 Nobel Prize Winner in Economic Sciences

Source: The White House

Professor Kahneman (Figure 1.6) found that under conditions of uncertainty, human decisions systematically depart from those predicted by standard economic theory. Kahneman, together with Amos Tversky (deceased in 1996), formulated prospect theory. An alternative to standard models, prospect theory provides a better account for observed behavior and is discussed at length in later chapters. Kahneman also discovered that human judgment may take heuristic shortcuts that systematically diverge from basic principles of probability. His work has inspired a new generation of research employing insights from cognitive psychology to enrich financial and economic models.

Another notable figure is Professor Dan Ariely (Figure 1.7). Professor Ariely is the James B. Duke Professor of Psychology and Behavioral Economics at Duke University and a founding member of the Center for Advanced Hindsight. He does research in behavioral economics on the irrational ways people behave. His immersive introduction to irrationality took place as he overcame injuries sustained in an explosion. He began researching ways to better deliver painful and unavoidable treatments to patients. Ariely became engrossed with the idea that we repeatedly and predictably make the wrong decisions in many aspects of our lives, and that research could help change some of these patterns.

Figure 1.7 Professor Dan Ariely, James B. Duke Professor of Marketing

Source: Yael Zur, for Tel Aviv University Alumni Organization, https://commons.wikimedia.org/wiki/File:Dan_Ariely_January_2019.jpg. CC BY-SA 4.0.

His works include Irrationally Yours, Predictably Irrational, The Upside of Irrationality, The (Honest) Truth About Dishonesty , the movie Dishonesty and the card game Irrational Game . These works describe his research findings in non-academic terms, so that more people will discover the excitement of behavioral economics and use some of the insights to enrich their own lives.

Behavioral Finance Micro versus Behavioral Finance Macro

As we have observed, behavioral finance models and interprets phenomena ranging from individual investor conduct to market-level outcomes. Therefore, it is a difficult subject to define. For practitioners and investors reading this book, this is a major problem, because our goal is to develop a common vocabulary so that we can apply behavioral finance. For purposes of this book, we adopt an approach favored by traditional economics textbooks; we break our topic down into two subtopics: behavioral finance micro and behavioral finance macro.

1 Behavioral finance micro (BFMI) examines behaviors or biases of individual investors that distinguish them from the rational actors envisioned in classical economic theory.

2 Behavioral finance macro (BFMA) detects and describe anomalies in the efficient market hypothesis that behavioral models may explain.

Each of the two subtopics of behavioral finance corresponds to a distinct set of issues within the standard finance versus behavioral finance discussion. With regard to BFMA, the debate asks: Are markets “efficient,” or are they subject to behavioral effects? With regard to BFMI, the debate asks: Are individual investors perfectly rational, or can cognitive and emotional errors impact their financial decisions? These questions are examined in the next section of this chapter; but to set the stage for the discussion, it is critical to understand that much of economic and financial theory is based on the notion that individuals act rationally and consider all available information in the decision-making process. In academic studies, researchers have documented abundant evidence of irrational behavior and repeated errors in judgment by adult human subjects.

Finally, one last thought before moving on. It should be noted that there is an entire body of information available on what the popular press has termed the psychology of money . This subject involves individuals' relationship with money—how they spend it, how they feel about it, and how they use it. There are many useful books in this area; however, this book will not focus on these topics, it will focus on building better portfolios.

Standard Finance versus Behavioral Finance

This section reviews two basic concepts in standard finance that behavioral finance disputes: rational markets and the rational economic man. It also covers the basis on which behavioral finance proponents challenge each tenet and discusses some evidence that has emerged in favor of the behavioral approach.

Overview

On Monday, October 18, 2004, a significant but mostly unnoticed article appeared in the Wall Street Journal . Eugene Fama, one of the leading scholars of the efficient market school of financial thought, was cited admitting that stock prices could become “somewhat irrational.” 8 Imagine a renowned and rabid Boston Red Sox fan proposing that Fenway Park be renamed Mariano Rivera Stadium (after the outstanding New York Yankees pitcher), and you may begin to grasp the gravity of Fama's concession. The development raised eyebrows and pleased many behavioralists. (Fama's paper “Market Efficiency, Long-Term Returns, and Behavioral Finance” noting this concession at the Social Science Research Network is one of the most popular investment downloads on the web site.) The Journal article also featured remarks by Roger Ibbotson, founder of Ibbotson Associates: “There is a shift taking place,” Ibbotson observed. “People are recognizing that markets are less efficient than we thought.” 9

As Meir Statman eloquently put it, “Standard finance is the body of knowledge built on the pillars of the arbitrage principles of Miller and Modigliani, the portfolio principles of Markowitz, the capital asset pricing theory of Sharpe, Lintner, and Black, and the option-pricing theory of Black, Scholes, and Merton.” 10 Standard finance theory is designed to provide mathematically elegant explanations for financial questions that, when posed in real life, are often complicated by imprecise, inelegant conditions. The standard finance approach relies on a set of assumptions that oversimplify reality. For example, embedded within standard finance is the notion of Homo economicus, or rational economic man. It prescribes that humans make perfectly rational economic decisions at all times. Standard finance, basically, is built on rules about how investors “should” behave, rather than on principles describing how they actually behave. Behavioral finance attempts to identify and learn from the human psychological phenomena at work in financial markets and within individual investors. Standard finance grounds its assumptions in idealized financial behavior; behavioral finance grounds its assumptions in observed financial behavior.

Efficient Markets versus Irrational Markets

During the 1970s, the standard finance theory of market efficiency became the model of market behavior accepted by the majority of academics and a good number of professionals. The efficient market hypothesis had matured in the previous decade, stemming from the doctoral dissertation of Eugene Fama. Fama persuasively demonstrated that in a securities market populated by many well-informed investors, investments will be appropriately priced and will reflect all available information. There are three forms of the efficient market hypothesis:

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Behavioral Finance and Your Portfolio»

Представляем Вашему вниманию похожие книги на «Behavioral Finance and Your Portfolio» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Behavioral Finance and Your Portfolio» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.