Benoîte de Saporta - Martingales and Financial Mathematics in Discrete Time

Здесь есть возможность читать онлайн «Benoîte de Saporta - Martingales and Financial Mathematics in Discrete Time» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Martingales and Financial Mathematics in Discrete Time

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Martingales and Financial Mathematics in Discrete Time: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Martingales and Financial Mathematics in Discrete Time»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Martingales and Financial Mathematics in Discrete Time — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Martingales and Financial Mathematics in Discrete Time», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

– If (An)n∈ℕ is decreasing (for the inclusion), then,

We will now review the concept of independent events and σ -algebras.

DEFINITION 1.8.– Let (Ω,  , ℙ) be a probability space .

, ℙ) be a probability space .

– Two events, A and B, are independent if ℙ(A ∩ B) = ℙ(A) × ℙ(B).

– A family of events (Ai ∈ i, i ∈ I) is said to be mutually independent if for any finite family J ⊂ I, we have

– Two σ-algebras and are independent if for any A ∈ and B ∈ , A and B are independent.

– A family of sub-σ-algebra i ⊂ , i ∈ I is mutually independent if any family of events (Ai ∈ i, i ∈ I) is mutually independent.

EXAMPLE 1.10.– We roll a six-faced die and write

– A1 the event “the number obtained is even”; and

– A2 the event “the number obtained is a multiple of 3” .

The universe of possible outcomes is Ω = {1, 2, 3, 4, 5, 6} which has a finite number of elements and as all its elements have the same chance of occurring, we can endow it with the uniform probability . Since

we have

Therefore, A 1 and A 2 are two independent events .

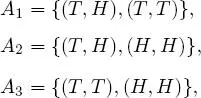

EXAMPLE 1.11.– A coin is tossed twice. The following events are considered:

– A1 “Obtaining tails (T) on the first toss”;

– A2 “Obtaining heads (H) on the second toss”; and

– A3 “Obtaining the same face on both tosses”.

The universe of possible outcomes is

which has four elements, and as all elements have the same chance of occurring, it can be endowed with uniform probability. Since

we have

and  Thus, the events A 1, A 2 and A 3 are pairwise independent, but are not mutually independent. Unless specified, the notion of independence by default always signifies mutual independence and not pairwise independence .

Thus, the events A 1, A 2 and A 3 are pairwise independent, but are not mutually independent. Unless specified, the notion of independence by default always signifies mutual independence and not pairwise independence .

1.2.2. Random variables

Let us now recall the definition of a generic random variable, and then the specific case of discrete random variables.

DEFINITION 1.9.– Let (Ω, , ℙ) be a probabilizable space and ( E , ε ) be a measurable space. A random variable on the probability space (Ω, , ℙ) taking values in the measurable space ( E , ε ), is any mapping X : Ω → E such that, for any B in ε, X −1( B ) ∈ ; in other words, X : Ω → E is a random variable if it is an ( , ε ) -measurable mapping. We then write the event “ X belongs to B ” by

In the specific case where E = ℝ and = ε =  (ℝ), the mapping X is called a real random variable. If E = ℝ d with d ≥ 2, and ε = (ℝ d), the mapping X is said to be a real random vector .

(ℝ), the mapping X is called a real random variable. If E = ℝ d with d ≥ 2, and ε = (ℝ d), the mapping X is said to be a real random vector .

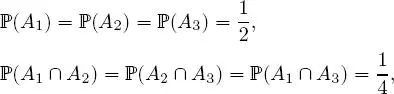

EXAMPLE 1.12.– Let us return to the experiment where a six-sided die is rolled, where the set of possible outcomes is Ω = {1, 2, 3, 4, 5, 6}, which is endowed with the uniform probability. Consider the following game:

– if the result is even, you win 10 ;

– if the result is odd, you win 20 .

This game can be modeled using the random variable defined by:

This mapping is a random variable, since for any B ∈  ({10, 20}), we have

({10, 20}), we have

and all these events are in (Ω).

DEFINITION 1.10.– The distribution of a random variable X defined on (Ω, , ℙ) taking values in ( E , ε ) is the mapping ℙ X: ε → [0, 1] such that, for any B ∈ ε,

The distribution of X is a probability distribution on ( E , ε ) ; it is also called the image distribution of ℙ by X .

DEFINITION 1.11.– A random real variable is discrete if X (Ω) is at most countable. In other words, if X (Ω) = x i, i ∈ I , where I ⊂ ℕ . In this case, the probability distribution of X is characterized by the family

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Martingales and Financial Mathematics in Discrete Time»

Представляем Вашему вниманию похожие книги на «Martingales and Financial Mathematics in Discrete Time» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Martingales and Financial Mathematics in Discrete Time» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.