SS

Здесь есть возможность читать онлайн «SS» весь текст электронной книги совершенно бесплатно (целиком полную версию без сокращений). В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: Справочники, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:SS

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

SS: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «SS»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

SS — читать онлайн бесплатно полную книгу (весь текст) целиком

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «SS», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

5.1.3 Methods, models, activities and techniques

This section of the chapter is intended to provide guidance in the form of sample model s, methods, activities and techniques for key areas. The guidance provided in this section is not intended to include all possibilities or alternatives, but to provide a sampling of best practice .

5.1.3.1 Service valuation

During the activities of service valuation , regardless of the lifecycle , time horizon or service chosen, decisions will need to be made regarding various issues. This section discusses the more common points of contention that all IT centres will need to address.

Direct versus indirect costsare those that are either: 1) clearly directly attributable to a specific service, versus 2) indirect cost s that are shared among multiple services. These costs should be approached logically to first determine which line items are sensible to maintain, given the data available and the level of effort required. For example, hardware maintenance service component s can be numerous and detailed, and it may not be of value to decompose them all for the purpose of assigning each to a line item cost element .

Once the depth and breadth of cost components are appropriately identified, rules or policy to guide how costs are to be spread among multiple services may be required. In the hardware maintenance example, rules can be created so that a percentage of the maintenance is allocated to any related services equally, or allocation rules could be based on some logical unit of consumption. Perceived equality of consumption often drives such decisions.

Labour costsare another key expenditure requiring a decision to be made. This decision is similar to that of ‘direct versus indirect’ above, compounded by the complexity and accuracy of time tracking system s. If the capability to account for resources allocated across services is not available, then rules and assumptions must be created for allocation of these costs. In its simplest form, organizing personnel costs across financial centres based on a service orientation is a viable method for aligning personnel costs to services. Similarly, administration costs for all IT Services can be collected at a macro level within a financial centre, and rules created for allocation of this cost amongst multiple services.

Variable cost elementsinclude expenditures that are not fixed, but which vary depending on things such as the number of user s or the number of running instances. Decisions need to be made based on the ability to pinpoint services or service components that cause increases in variability, since this variability can be a major source of price sensitivity. Pricing variability over time can cause the need for rules to allow for predictability. Associating a cost with a highly variable service requires the ability to track specific consumption of that service over time in order to establish ranges. Predictability of that cost can be addressed through:

Tiers – identifying price breaks where plateaus occur within a provider so that customers are encouraged to obtain scale efficiencies familiar to the provider.

Maximum cost – prescribing the cost of the service based on the maximum level of variability. This would then most likely cause overcharging, but the business may prefer ‘rebates’ versus additional costs.

Average cost – this involves setting the cost of the service based on historical averaging of the variability. It would leave some amount of over- or under-charge to be addressed at the end of the planning cycle.

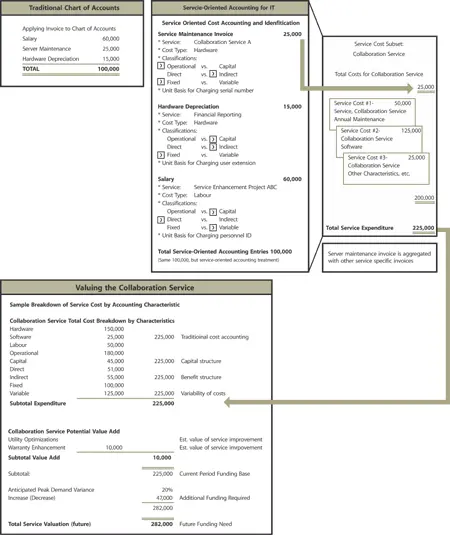

Translation from cost account data to service valueis only possible once costs are attributed to services rather than, or in addition to, traditional cost accounts. The example shown in Figure 5.3 illustrates the FM translation of traditional cost account data into service account information, and ultimately into the valuation of the service. This metamorphosis provides a powerful layer of visibility to the cost structures of services.

Figure 5.3 Translation of cost account data to service account information

In this example, detailed service-oriented cost entries are captured and applied in order to establish the underlying cost baseline for the service (the first component of service valuation ). Once this baseline has been established, monetary conversion of the value of any anticipated marginal enhancement to the utility and warranty of a customer’s existing service asset s occurs in order for the total potential value of the service to be determined.

After determining the fixed and variable cost s for each service, steps should be taken to determine the variable cost driver s and range of variability for a service. This drives any additional amount that should be added to the calculation of potential service value in order to allow for absorption of consumption variability. Determining the perceived or requisite value to add to the calculation is also dependent on the operating model chosen since this takes into account culture , organization, and strategic direction.

Pricing the perceived value portion of a service involves resolving a grey area between historical costs, perceived value-added, and planned demand variance s. Through this exercise, depending on the level of cost visibility present, even if actual costs are not recovered, the goal of providing cost visibility and value is demonstrated.

5.1.3.2 Service provisioning models and analysis

As companies analyse their current methods for providing services there are some basic alternatives to be considered that assist in framing the discussion and the analysis. There are distinct advantages to the various provisioning service model s available, and while there are non-financial aspects to consider, such as service quality and transition readiness, this section will only address the financial analysis of the presented models.

The Managed Services provisioning model is the more traditional variant commonly known in the industry. In its simplest form, it is where a business unit requiring a service funds the provision of that service for itself. The service provider attempts to calculate the cost of the service in terms of development , infrastructure, manpower etc. so that the business and the service provider can plan for funding accordingly. In this simple example, the service is managed through the customer -specific application of service-related hardware, software and manpower, and the business unit pays for the entire service.

This is typically the most expensive service provisioning model because the resource s used to provide the service are completely dedicated to the service of a single entity. If the consumer does not utilize the service and related resources to the fullest extent technically possible, then unused capacity and the opportunity to provide additional services using the same capacity and resources is lost.

The model for Shared Servicestargets the provisioning of multiple services to one or more business units through use of shared infrastructure and resources (Figure 5.4). This concept is also widely applied throughout industry and represents significant cost savings to practitioners over the managed services model through the increased utilization of existing resources.

Читать дальшеИнтервал:

Закладка:

Обсуждение, отзывы о книге «SS» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.