Dr. Pass - Economics

Здесь есть возможность читать онлайн «Dr. Pass - Economics» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Economics

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Economics: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Economics»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Economics — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Economics», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

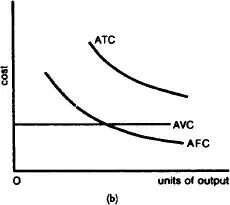

average cost (short-run)the unit cost (TOTAL COST divided by the number of units produced) of producing particular volumes of output in a plant of a given (fixed) size.

Average total cost (ATC) can be split up into average FIXED COST (AFC) and average VARIABLE COST (AVC). AFC declines continuously as output rises as a given total amount of fixed cost is ‘spread’ over a greater number of units. For example, with fixed costs of £1,000 per year and annual output of 1,000 units, fixed costs per unit would be £1, but if annual output rose to 2,000 units, the fixed cost per unit would fall to 50 pence – see AFC curve in Fig. 11 (a).

Over the whole potential output range within which a firm can produce, AVC falls at first (reflecting increasing RETURNS TO THE VARIABLE FACTOR INPUT output increases faster than costs), but then rises (reflecting DIMINISHING RETURNS to the variable inputs – costs increase faster than output), as shown by the AVC curve in Fig. 11 (a). Thus the conventional SHORT-RUN ATC curve is U-shaped.

Fig. 11 Average cost (short-run).(a) The characteristic curves of average total cost (ATC), average variable cost (AVC), and average fixed cost (AFC), over the whole output range. (b) The characteristic curves of ATC and AFC and constant line of AVC over the restricted output range.

Over the more restricted output range in which firms typically operate, however, constant returns to the variable input are more likely to be experienced, where, as more variable inputs are added to the fixed inputs employed in production, equal increments in output result. In such circumstances, AVC will remain constant over the whole output range, as in Fig. 11 (b), and as a consequence ATC will decline in parallel with AFC. Compare AVERAGE COST (LONG-RUN). See LOSS, LOSS MINIMIZATION.

average-cost pricing1 a pricing method that sets the PRICE of a product by adding a percentage profit mark-up to AVERAGE COST or unit total cost. This method is identical in most respects to FULL-COST PRICING; indeed, the terms are often used interchangeably.

2 a pricing principle that argues for setting PRICES equal to the AVERAGE COST of production and distribution, so that prices cover both MARGINAL COSTS and FIXED OVERHEADS costs incurred through past investments. This involves the (sometimes arbitrary) apportionment of fixed (overhead) costs to individual units of output, though it does seek to recover in the price charged all the costs that would have been avoided by not producing the product. See MARGINAL-COST PRICING, TWO-PART TARIFF.

average fixed costsee AVERAGE COST (SHORT-RUN).

average physical productthe average OUTPUT in the SHORT-RUN theory of supply produced by each extra unit of VARIABLE FACTOR INPUT (in conjunction with a given amount of FIXED FACTOR INPUT). This is calculated by dividing the total quantity of OUTPUT produced by the number of units of input used. In the SHORT RUN theory of supply, average physical product, together with AVERAGE REVENUE per unit of output, indicates to a firm how many factor inputs to employ in order to maximize profit. See MARGINAL PHYSICAL PRODUCT, DIMINISHING RETURNS, VARIABLE-FACTOR INPUT.

average propensity to consume (APC)the fraction of a given level of NATIONAL INCOME that is spent on consumption:

Alternatively, consumption can be expressed as a proportion of DISPOSABLE INCOME. See CONSUMPTION EXPENDITURE, PROPENSITY TO CONSUME, MARGINAL PROPENSITY TO CONSUME.

average propensity to import (APM)the fraction of a given level of NATIONAL INCOME that is spent on IMPORTS:

Alternatively, imports can be expressed as a proportion of DISPOSABLE INCOME. See also PROPENSITY TO IMPORT, MARGINAL PROPENSITY TO IMPORT.

average propensity to save (APS)the fraction of a given level of NATIONAL INCOME that is saved (see SAVING):

Alternatively, saving can be expressed as a proportion of DISPOSABLE INCOME. See also PROPENSITY TO SAVE, MARGINAL PROPENSITY TO SAVE.

average propensity to tax (APT)the fraction of a given level of NATIONAL INCOME that is appropriated by the government in TAXATION:

See also PROPENSITY TO TAX, MARGINAL PROPENSITY TO TAX, AVERAGE RATE OF TAXATION.

average rate of taxationthe total TAX paid by an individual divided by the total income upon which the tax was based. For example, if an individual earned £10,000 in one year upon which that individual had to pay tax of £2,500, the average rate of taxation would be 25%. See STANDARD RATE OF TAXATION, MARGINAL RATE OF TAXATION, PROPENSITY TO TAX, PROPORTIONAL TAXATION, REGRESSIVE TAXATION, PROGRESSIVE TAXATION.

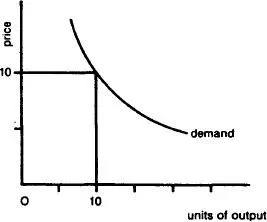

average revenuethe total revenue received (price X number of units sold) divided by the number of units. Price and average revenue are in fact equal: i.e. in Fig. 12, the price £10 = average revenue (£10 × 10 ÷ 10) = £10. It follows that the DEMAND CURVE is also the average revenue curve facing the firm.

average revenue productthe total REVENUE obtained from using a given quantity of VARIABLE-FACTOR INPUT to produce and sell output, divided by the number of units of input. The average revenue product of a factor is given by the factor’s AVERAGE PHYSICAL PRODUCT multiplied by the AVERAGE REVENUE or PRICE of the product. The average revenue product, together with average cost, indicates to a firm how many factor inputs to employ in order to maximize profit in the SHORT RUN. See MARGINAL REVENUE PRODUCT.

Fig. 12 Average revenue.The demand curve or average revenue curve.

average total cost (ATC)see AVERAGE COST (SHORT-RUN), AVERAGE COST (LONG-RUN).

average variable cost (AVC)see AVERAGE COST (SHORT-RUN), AVERAGE COST (LONG-RUN).

b

back doorthe informal mechanism whereby the BANK OF ENGLAND buys back previously issued TREASURY BILLS in the DISCOUNT MARKET at their ruling market price in order to release money to help the DISCOUNT HOUSES overcome temporary liquidity shortages. This is done as a means of increasing the liquid funds available not only to the discount houses themselves but also to the COMMERCIAL BANKS at prevailing interest rates to enable them to maintain their lending. Compare FRONT DOOR.

back-to-back loan or parallel loanan arrangement under which two companies in different countries borrow each other’s currency and agree to repay the loans at a specified future date. At the expiry date of the loans, each company receives the full amount of its loan in its domestic currency without risk of losses from exchange-rate changes. In this way back-to-back loans serve to minimize EXCHANGE-RATE EXPOSURE.

backward integrationthe joining together in one firm of two or more successive stages in a vertically related production/distribution process, with a later stage (for example, bread making) being combined with an earlier stage (for example, flour milling) Backward integration is undertaken to cut costs and secure supplies of inputs. See VERTICAL INTEGRATION, FORWARD INTEGRATION.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Economics»

Представляем Вашему вниманию похожие книги на «Economics» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Economics» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.