Dr. Pass - Economics

Здесь есть возможность читать онлайн «Dr. Pass - Economics» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Economics

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Economics: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Economics»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

Economics — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Economics», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

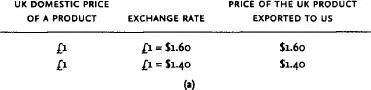

(b) internal price and income adjustments. The use of deflationary and reflationary (see DEFLATION, REFLATION) monetary and fiscal policies to alter the prices of domestically produced goods and services vis-à-vis products supplied by other countries so as to make exports relatively cheaper/dearer and imports more expensive/cheaper in foreign currency terms. For example, again with regard to exports, if it were possible to reduce the domestic price of a British product, as shown in Fig. 14 (b), given an unchanged exchange rate, this would allow the dollar price of the product in the American market to be reduced, thereby improving its price competitiveness vis-à-vis similar American products. The same policies are used to alter the level of domestic income and spending, including expenditure on imports.

(c) trade and foreign exchange restrictions. The use of TARIFFS, QUOTAS, FOREIGN-EXCHANGE CONTROLS, etc., to affect the price and availability of goods and services, and of the currencies with which to purchase these products.

Under a FIXED EXCHANGE-RATE SYSTEM, minor payments imbalances are corrected by appropriate domestic adjustments (b), but fundamental disequilibriums require, in addition, a devaluation or revaluation of the currency (a). It must be emphasized, however, that a number of favourable conditions must be present to ensure the success of devaluations and revaluations (see DEPRECIATION 1 for details).

Fig. 14 Balance-of-payments equilibrium.(b) Internal price adjustment.

In theory, a FLOATING EXCHANGE-RATE SYSTEM provides an ‘automatic’ mechanism for removing payments imbalances in their incipiency (that is, before they reach ‘fundamental’ proportions): a deficit results in an immediate exchange-rate depreciation, and a surplus results in an immediate appreciation of the exchange rate (see PURCHASING-POWER PARITY THEORY). Again, however, a number of favourable conditions must be present to ensure the success of depreciations and appreciations. See also ADJUSTMENT MECHANISM, J-CURVE, INTERNAL-EXTERNAL BALANCE MODEL, MARSHALL-LERNER CONDITION, TERMS OF TRADE.

balance of tradea statement of a country’s trade in GOODS (visibles) with the rest of the world over a particular period of time. The term ‘balance of trade’ specifically excludes trade in services (invisibles) and concentrates on the foreign currency earnings and payments associated with trade in finished manufactures, intermediate products and raw materials, which can be seen and recorded by a country’s customs authorities as they cross national boundaries. See BALANCE OF PAYMENTS.

balance sheetan accounting statement of a firm’s ASSETS and LIABILITIES on the last day of a trading period. The balance sheet lists the assets that the firm owns and sets against these the balancing obligations or claims of those groups of people who provided the funds to acquire the assets. Assets take the form of FIXED ASSETS and CURRENT ASSETS, while obligations take the form of SHAREHOLDERS’ CAPITAL EMPLOYED, long-term loans and CURRENT LIABILITIES.

balances with the Bank of Englanddeposits of money by the COMMERCIAL BANKS with the BANK OF ENGLAND. The Bank of England acts as the ‘bankers’ bank’ and commercial banks settle indebtedness between themselves by transferring ownership of these balances. Such balances are included as part of the commercial banks’ CASH RESERVES RATIO and RESERVE ASSET RATIO. In addition to the balances held for settling indebtedness, the banks may be required from time to time to make SPECIAL DEPOSITS with the Bank, which have the effect of reducing their reserve assets.

balancing itemsee BALANCE OF PAYMENTS.

banka deposit-taking institution that is licensed by the monetary authorities of a country (the BANK OF ENGLAND in the UK) to act as a repository for money deposited by persons, companies and institutions, and which undertakes to repay such deposits either immediately on demand (CURRENT ACCOUNT 2) or subject to due notice being given (DEPOSIT ACCOUNTS). Banks perform various services for their customers (money transmission, investment advice, etc.) and lend out money deposited with them in the form of loans and overdrafts or use their funds to purchase financial securities in order to operate at a profit. There are many types of banks, including COMMERCIAL BANKS, MERCHANT BANKS, SAVINGS BANKS and INVESTMENT BANKS. In recent years many BUILDING SOCIETIES have also established a limited range of banking facilities. See BANKING SYSTEM, CENTRAL BANK, FINANCIAL SYSTEM.

bank deposita sum of money held on deposit with a COMMERCIAL BANK (or SAVINGS BANK). Bank deposits are of two main types: sight deposits (CURRENT ACCOUNTS), which are withdrawable on demand; time deposits (DEPOSIT ACCOUNTS), which are withdrawable subject usually to some notice being given. Sight deposits represent instant LIQUIDITY: they are used to finance day-to-day transactions and regular payments either in the form of a CURRENCY withdrawal or a CHEQUE transfer. Time deposits are usually held for longer periods of time to meet irregular payments and as a form of savings.

Bank deposits constitute an important component of the MONEY SUPPLY. See BANK DEPOSIT CREATION, MONETARY POLICY.

bank deposit creation or credit creation or money multiplierthe ability of the COMMERCIAL BANK system to create new bank deposits and hence increase the MONEY SUPPLY. Commercial banks accept deposits of CURRENCY from the general public. Some of this money is retained by the banks to meet day-to-day withdrawals (see RESERVE-ASSET RATIO). The remainder of the money is used to make loans or is invested. When a bank on-lends, it creates additional deposits in favour of borrowers. The amount of new deposits the banking system as a whole can create depends on the magnitude of the reserve-asset ratio. In the example set out in Fig. 15, the banks are assumed to operate with a 50% reserve-asset ratio: Bank 1 receives initial deposits of £100 million from the general public. It keeps £50 million for liquidity purposes and on-lends £50 million. This £50 million, when spent, is redeposited with Bank 2; Bank 2 keeps £25 million as part of its reserve assets and on-lends £25 million; and so on. Thus, as a result of an initial deposit of £100 million, the banking system has been able to ‘create’ an additional £100 million of new deposits.

Fig. 15 Bank deposit creation.Deposit creation operated with a 50% reserve-asset ratio in a multibank system.

Since bank deposits constitute a large part of the MONEY SUPPLY, the ability of the banking system to ‘create’ credit makes it a prime target for the application of MONETARY POLICY as a means of regulating the level of spending in the economy.

Bank for International Settlements (BIS)an international bank, situated in Basle and established in 1930, that originally acted as a coordinating agency for the central banks of Germany, France, Italy, Belgium and the UK in settling BALANCE-OF-PAYMENTS imbalances and for other intercentral bank dealings. Nowadays its membership comprises all western European central banks together with those of the USA, Canada and Japan. Although the INTERNATIONAL MONETARY FUND is the main institution responsible for the conduct of international monetary affairs, the BIS is still influential in providing a forum for discussion and surveillance of international banking practices.

banking systema network of COMMERCIAL BANKS and other more specialized BANKS (INVESTMENT BANKS, SAVINGS BANKS, MERCHANT BANKS) that accept deposits and savings from the general public, firms and other institutions, and provide money transmission and other financial services for customers, operate loan and credit facilities for borrowers, and invest in corporate and government securities. The banking system is part of a wider FINANCIAL SYSTEM and exerts a major influence on the functioning of the ‘money economy’ of a country. Bank deposits occupy a central position in the country’s MONEY SUPPLY and hence the banking system is closely regulated by the money authorities. See BANK OF ENGLAND, CENTRAL BANK, CLEARING HOUSE SYSTEM.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Economics»

Представляем Вашему вниманию похожие книги на «Economics» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Economics» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.