Werner Seebacher - Management Accounting. Workbook 2

Здесь есть возможность читать онлайн «Werner Seebacher - Management Accounting. Workbook 2» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Management Accounting. Workbook 2

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Management Accounting. Workbook 2: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Management Accounting. Workbook 2»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

The textbook «Management Accounting.» deals with the «Big Picture» – the Accounting/Controlling Overall Context – as well as with the elements presenting this connection: Balance Sheet | Profit/Loss Account | Profit Plan | Finance Plan | Budgeted Balance Sheet.

In the «Workbook 2 – Profit Plan | Finance Plan | Budgeted Balance Sheet» the effects of concrete accounting/controlling activities and business cases in and on profit plan, finance plan and budgeted balance sheet are presented and explained. The presentation is in form of case studies.

Following the examples which deal with individual business activities each, the mathematical connections between profit plan, finance plan and budgeted balance sheet are presented in a comprehensive case study.

"Management Accounting. Workbook 2 – Profit Plan | Finance Plan | Budgeted Balance Sheet" is directed towards students and practitioners – to students doing business courses in the framework of their basic education or their introductory semesters respectively, to students doing postgraduate programs as well as practitioners in management jobs."

Management Accounting. Workbook 2 — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Management Accounting. Workbook 2», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

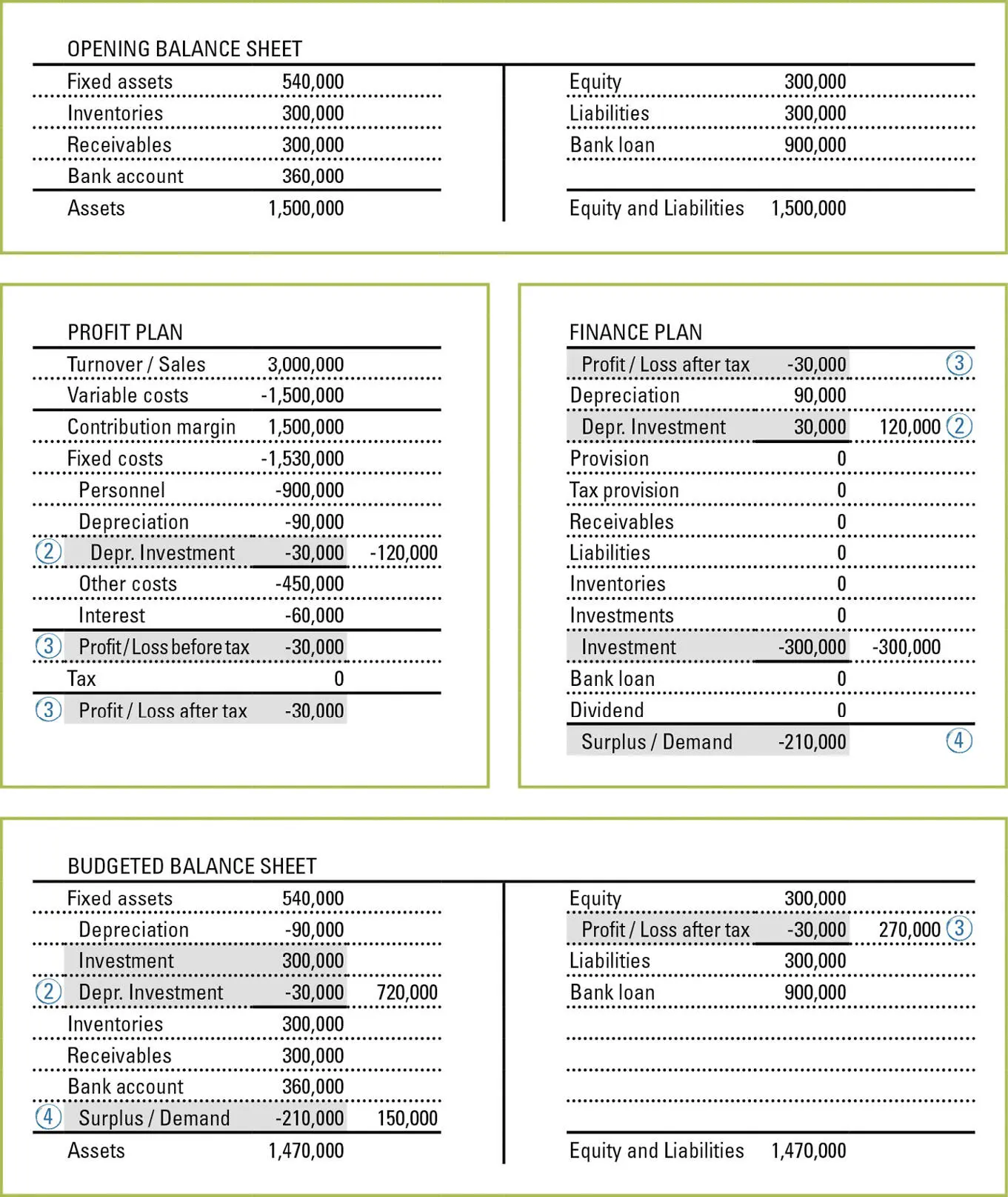

The planned investment of 300,000 has a deteriorating effect on the liquidity in the finance plan of the enterprise.

Together with the depreciation of 90,000 which is incorporated into the finance plan with a positive mathematical sign, the investment so leads (based on a planned profit or loss of 0 in the profit plan which forms the basis for the finance plan) to a cash requirement of 210,000 as result of the finance plan.

The investment of 300,000 increases the fixed assets in the budgeted balance sheet of the enterprise whereas at the same time the depreciation of 90,000, which was stated in the basic data, reduces the fixed assets.

The cash requirement of 210,000 in the finance plan reduces the balance of the bank account in the budgeted balance sheet.

Answer Key Step 2-4/4

Figure 25: Investment | Answer Key Step 2-4/4

Subsequently the steps 2 to 4 arise in an automatic order:

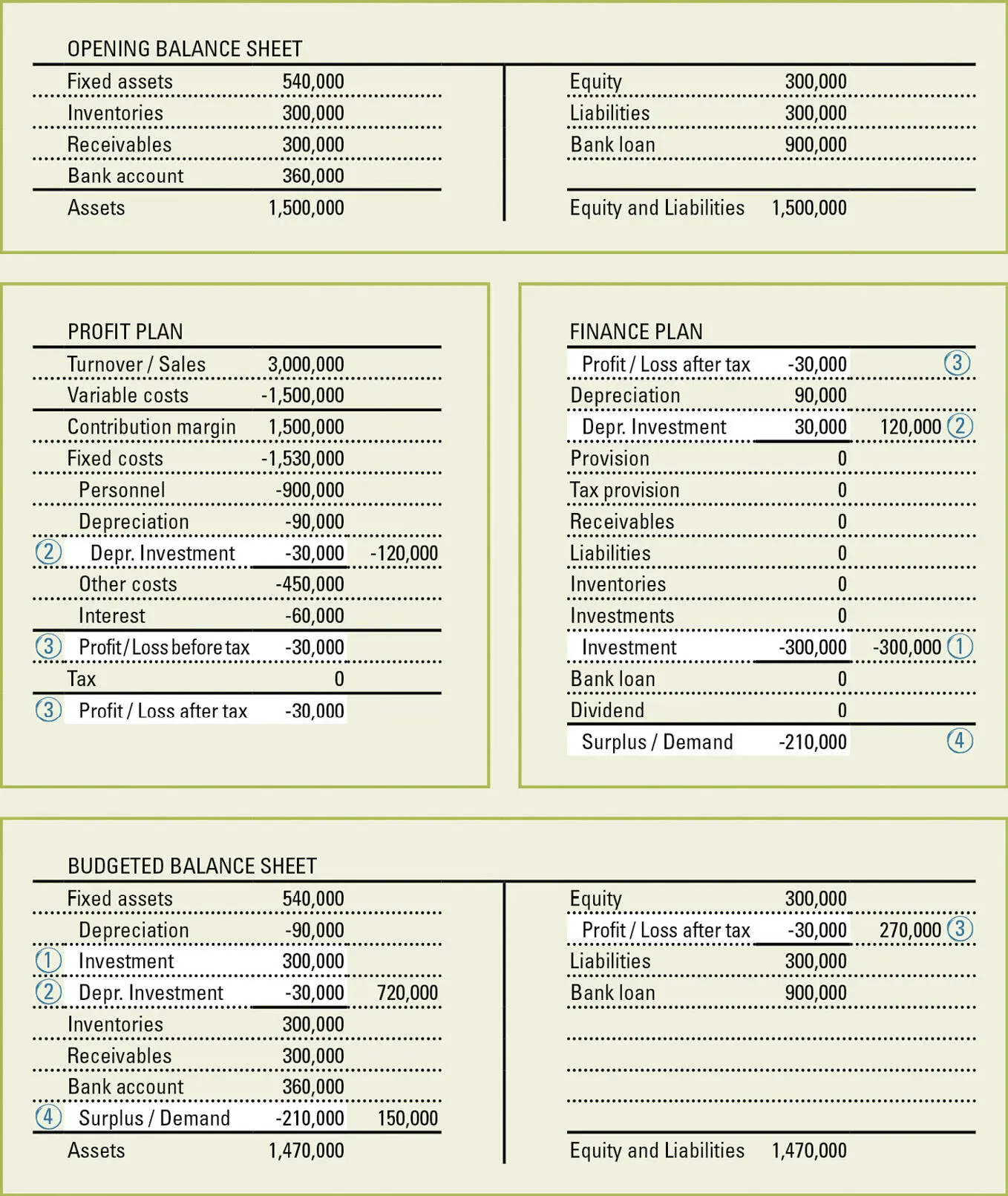

The depreciation amount of 30,000 results from dividing the invested amount of 300,000 by the depreciation period or useful life of 10 years.

The depreciation of 30,000 has a deteriorating effect on the result in the profit plan of the enterprise. (2) Due to the additional depreciation amount of 30,000 the fixed costs rise in the profit plan. As the profit plan in the example given is based on the assumption of a profit or loss of 0 the increased fixed costs lead to loss amounting to 30,000. (3) This loss which was compiled in the profit plan forms simultaneously the new basis for the finance plan.

By the new loss of 30,000 which forms the basis for the finance plan (3), by the depreciation of 90,000 which was transferred from the basic data, by the new depreciation of 30,000 (2) and by the investment of 300,000 which has already been presented in step 1, a cash requirement of 210,000 arises as result of the finance plan. (4)

In addition all changing values are incorporated from the finance plan into the budgeted balance sheet:

The new depreciation of 30,000 (2), additionally to the depreciation which has been transferred from the basic data, reduces the fixed assets in the budgeted balance sheet.

The loss which was transfered from the profit plan as the basis for the finance plan reduces the equity in the budgeted balance sheet. (3)

The cash requirement as the result of the finance plan reduces the bank account in the budgeted balance sheet. (4)

Complete Answer Key Step 1-4/4

Figure 26: Investment | Complete Answer Key Step 1-4/4

The planned investment of 300,000 has a deteriorating effect on the liquidity in the finance plan of the enterprise. (1)

The depreciation amount of 30,000 results from dividing the investment amount of 300,000 by the depreciation period or useful life of the investment object of 10 years.

Due to the additional depreciation amount of 30,000 the fixed cost rise in the profit plan by 30,000. So, the depreciation has a negative effect on the result in the profit plan of the enterprise. At the same time the depreciation is corrected in the finance plan with a positive mathematical sign as it doesn’t lead to a payment in cash. (2)

As the profit plan in the example given is based on the assumption of a profit or loss of 0 the increased fixed costs result in a loss amounting to 30,000. This loss of 30,000 which was compiled in the profit plan forms simultaneously the new basis for the finance plan. (3)

By the new loss of 30,000 which forms the basis for the finance plan ((3)), by the existing depreciation of 90,000 (see basic data), by the new depreciation of 30,000 ((2)) and by the investment of 300,000 ((1)) cash requirements of 210,000 arise as a result of the finance plan. (4)

All changing values are incorporated from the finance plan into the budgeted balance sheet:

The investment of 300,000 increases the fixed assets in the budgeted balance sheet. (1)

The existing depreciation of 90,000 (basic data) and the new depreciation of 30,000 (2) reduce the fixed assets in the budgeted balance sheet.

The loss of 30,000 which was transfered from the profit plan to the finance plan reduces the equity in the budgeted balance sheet. (3)

The demand for cash as the result of the finance plan reduces the bank account in the budgeted balance sheet. (4)

Assignment of tasks

In the enterprise in the example given the existing bank loan is planned to be increased by the amount of 150,000 at the beginning of the business year. The interest rate for the additional loan is 5 % annually and is debited against the existing bank account.

On the next page, opening balance sheet, as well as profit plan, finance plan and budgeted balance sheet of the enterprise are presented before taking the above described business activity into consideration.

Please, present in what way the increase of the loan and the interest payment for this additional loan affect profit plan, finance plan and budgeted balance sheet of the enterprise.

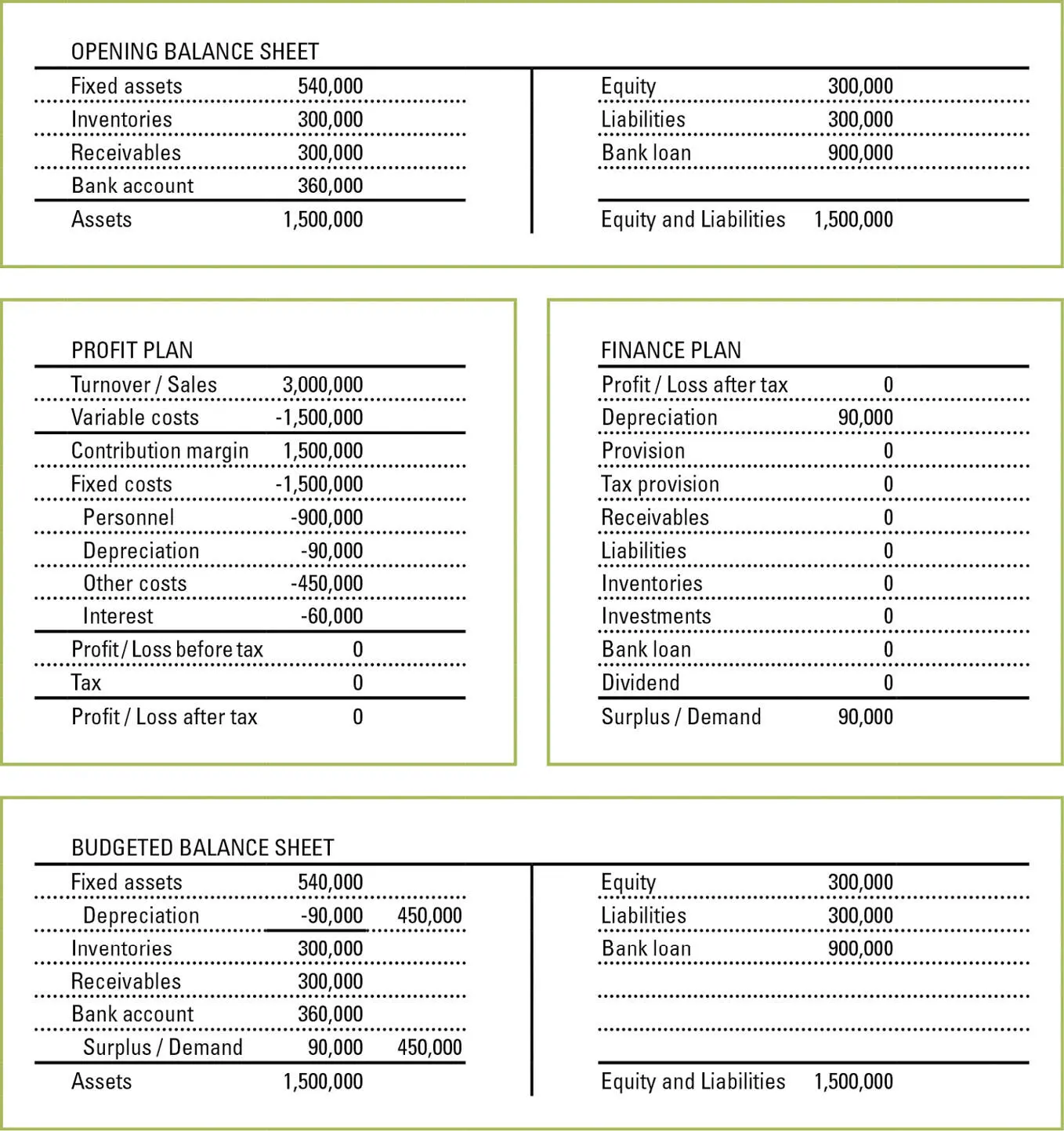

Basic Data

Figure 27: Financing | Basic Data

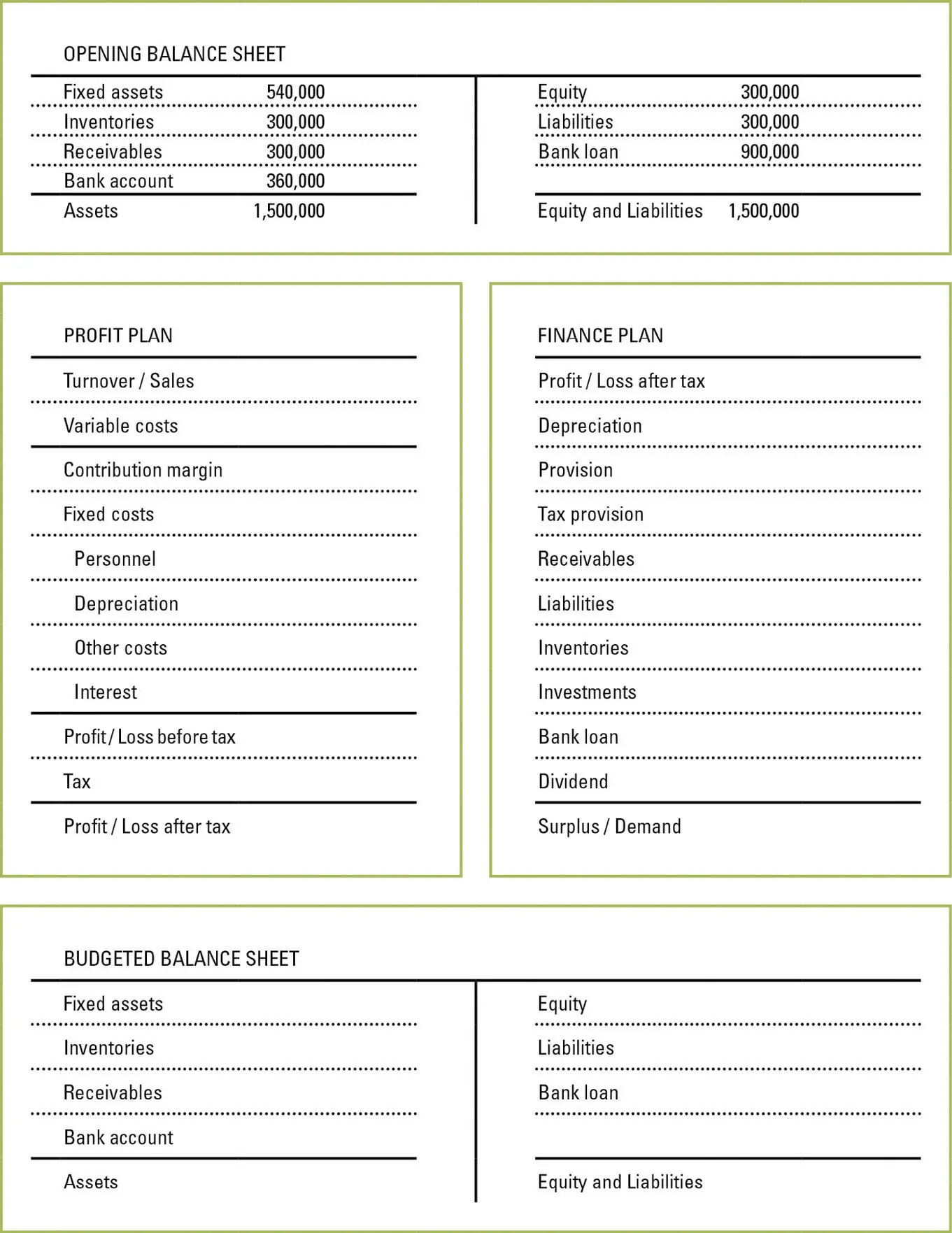

Answer Form

Figure 28: Financing | Answer Form

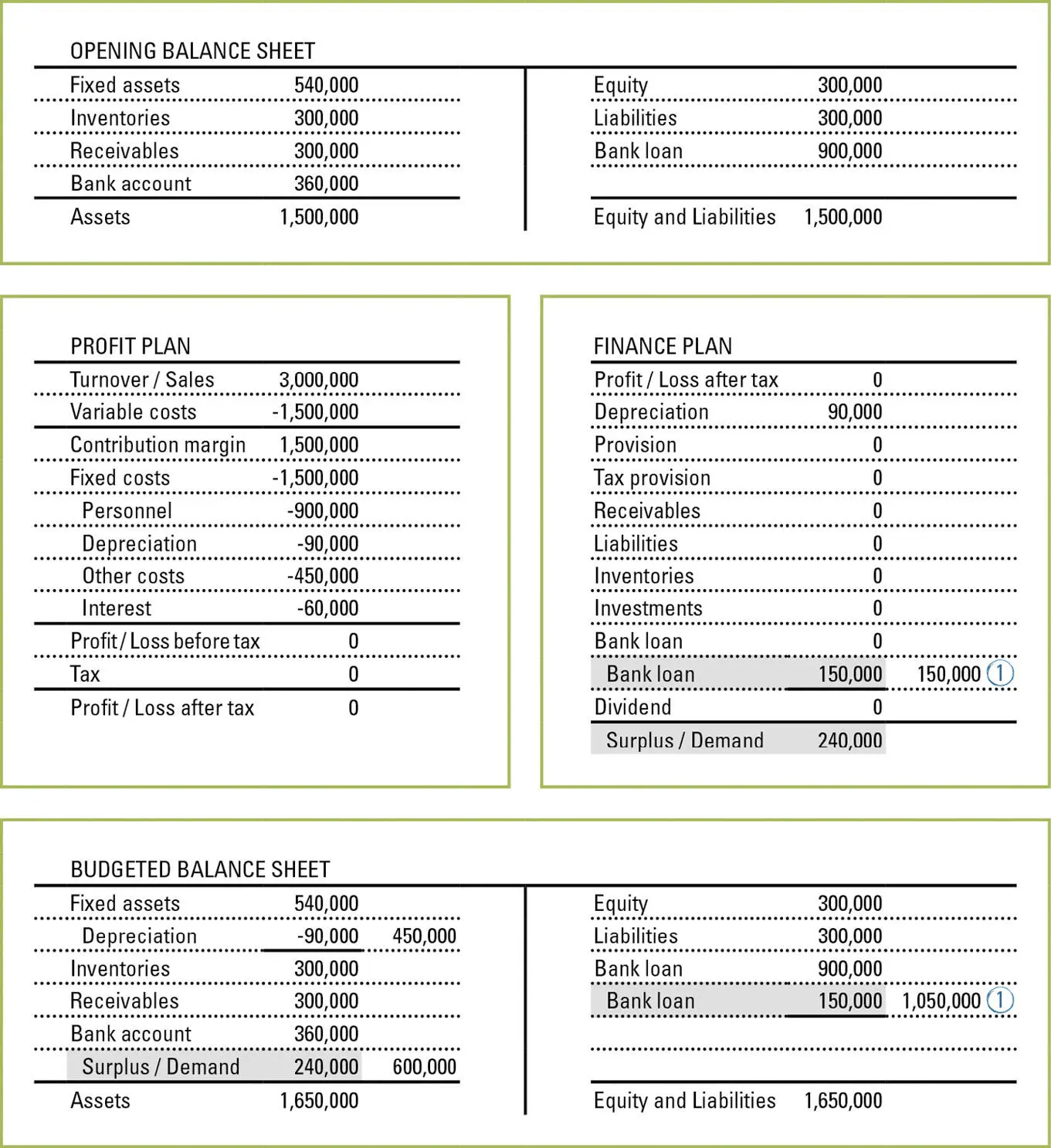

Answer Key Step 1/4

Figure 29: Financing | Answer Key Step 1/4

The planned increase of the loan by 150,000 has an improving effect on the liquidity in the finance plan of the enterprise.

Together with the depreciation of 90,000 which is incorporated into the finance plan with a positive mathematical sign, the increase of the loan (based on a planned profit or loss of 0 in the profit plan which is the basis for the finance plan) so leads to a surplus of cash of 240,000 as result of the finance plan.

The raising of the loan rises the bank loan in the budgeted balance sheet of the enterprise, the depreciation of 90,000 which has already been stated in the basic data, reduces the fixed assets.

The surplus of cash of 240,000 in the finance plan increases the balance of the bank account in the budgeted balance sheet.

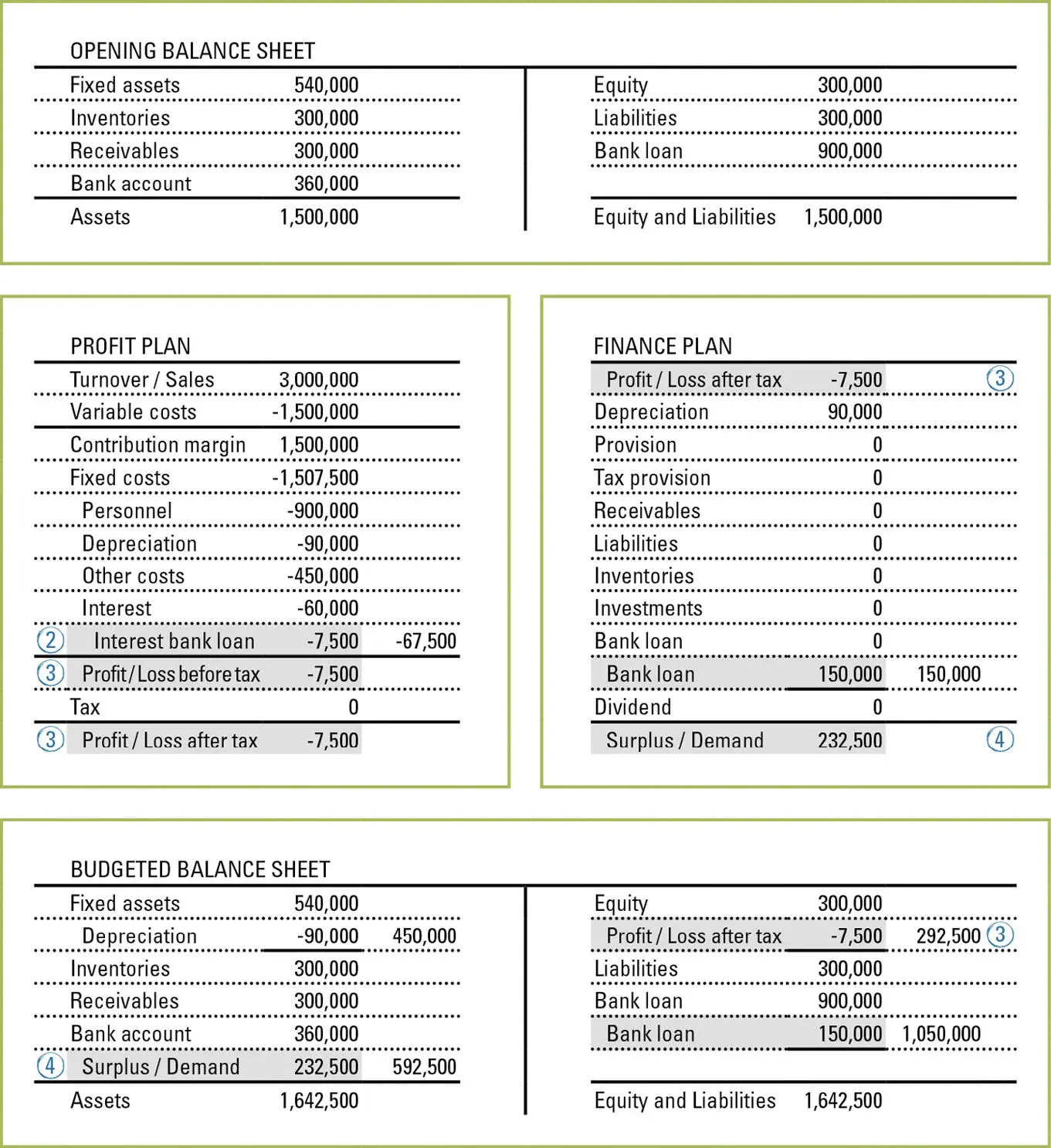

Answer Key Step 2-4/4

Figure 30: Financing | Answer Key Step 2-4/4

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Management Accounting. Workbook 2»

Представляем Вашему вниманию похожие книги на «Management Accounting. Workbook 2» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Management Accounting. Workbook 2» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.