Werner Seebacher - Management Accounting. Workbook 2

Здесь есть возможность читать онлайн «Werner Seebacher - Management Accounting. Workbook 2» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Management Accounting. Workbook 2

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Management Accounting. Workbook 2: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Management Accounting. Workbook 2»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

The textbook «Management Accounting.» deals with the «Big Picture» – the Accounting/Controlling Overall Context – as well as with the elements presenting this connection: Balance Sheet | Profit/Loss Account | Profit Plan | Finance Plan | Budgeted Balance Sheet.

In the «Workbook 2 – Profit Plan | Finance Plan | Budgeted Balance Sheet» the effects of concrete accounting/controlling activities and business cases in and on profit plan, finance plan and budgeted balance sheet are presented and explained. The presentation is in form of case studies.

Following the examples which deal with individual business activities each, the mathematical connections between profit plan, finance plan and budgeted balance sheet are presented in a comprehensive case study.

"Management Accounting. Workbook 2 – Profit Plan | Finance Plan | Budgeted Balance Sheet" is directed towards students and practitioners – to students doing business courses in the framework of their basic education or their introductory semesters respectively, to students doing postgraduate programs as well as practitioners in management jobs."

Management Accounting. Workbook 2 — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Management Accounting. Workbook 2», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

Profit Plan | Finance Plan | Budgeted Balance Sheet

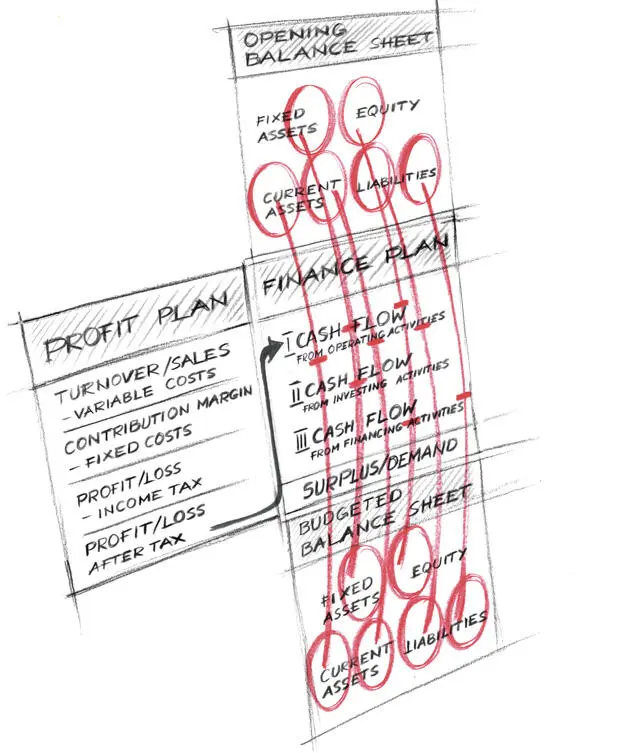

Profit Plan, Finance Plan and Budgeted Balance Sheet are compiled, building one on top of the other and together they result in the “Accounting/Controlling Overall Connection” – the Big Picture:

Figure 1: Big Picture

In the profit plan, based on the planned turnover/sales, the planned variable and fixed costs are deducted and lead to the planned result before or after taxes on income. The result of the profit plan is the planned profit or loss respectively of the enterprise.

The compilation of the profit plan is followed by the finance plan. In the finance plan, based on the planned profit/loss after taxes from the profit plan, the liquidity or solvency of the enterprise is planned. The result of the finance plan is the planned surplus of or demand for cash of the enterprise.

Building on the finance plan, the budgeted balance sheet of the enterprise is compiled in the next step. The basis for compiling the budgeted balance sheet for the end of the planned year is the opening balance sheet of the planned year (or the closing balance sheet of the previous business year respectively). Basing on the opening balance sheet, each individual item of the finance plan changes the opening balance sheet towards the budgeted balance sheet.

Profit plan, finance plan and budgeted balance sheet present the planned future development of the economic or financial situation of the enterprise.

In a past-oriented presentation, the profit plan is replaced by the results statement or the profit/loss account respectively. The finance plan is replaced by the cash flow statement; the budgeted balance sheet is replaced by the balance sheet.

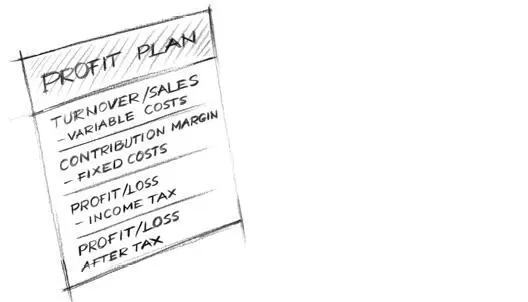

Profit Plan

The profit plan which is shown here based on the structure of a results statement or contribution margin costing, presents – in a future-oriented consideration – the expected or planned profit situation of an enterprise.

Figure 2: Profit Plan

Referring to the content or the result which is to be determined (profit or loss), the profit plan represents a results statement or profit/loss account (that helps to assess the profit situation of an enterprise in a past-oriented way).

The result of both calculation schemes – as well that of the profit plan as that of the profit/loss account – is the (planned) profit or loss of the enterprise for which differing terms are used – depending on the structure it is based on: Corporate Result before or after tax or, as an alternative, Profit from Ordinary Activities or Net Profit/Net Loss.

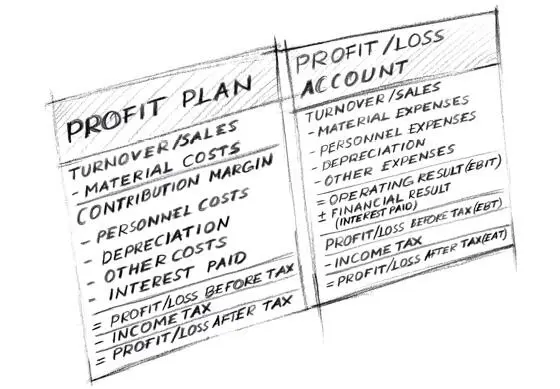

In a more detailed presentation the structures can be compared as follows:

Figure 3: Profit Plan and Profit/Loss Account

Figure 3: Profit Plan and Profit/Loss Account

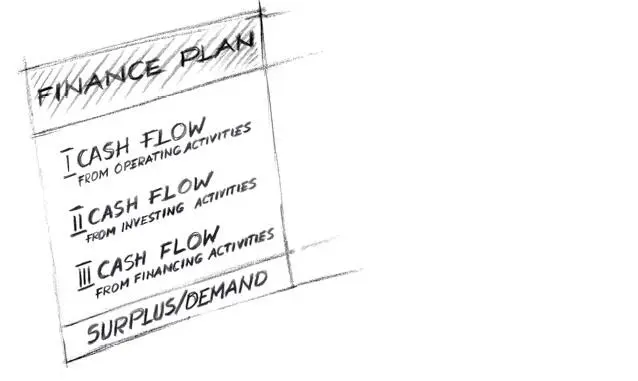

Finance Plan

The compilation of the profit plan is followed by the finance plan. Basing on the planned result after tax from the profit plan, the liquidity or solvency respectively of the enterprise is planned in the finance plan. Result of the finance plan is the planned surplus of or demand for cash of the enterprise.

Figure 4: Finance Plan

The planned profit from the profit plan is converted into cash flows in the finance plan.

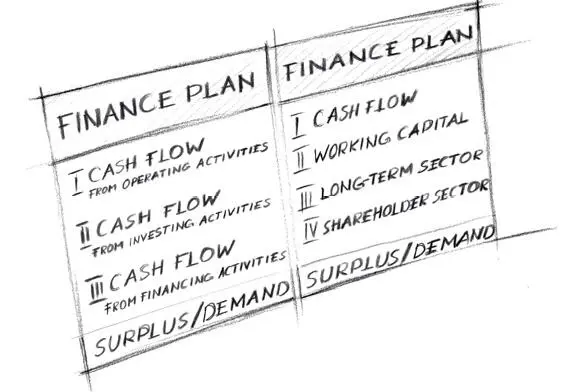

In the framework of presenting finance plans, two central schemes are contrasted to each other which are sub-divided into three or four sub-sectors. The basis for both schemes (the result after tax that is transferred from the profit plan) is the same, as well as the result of the two schemes (the surplus of or demand for cash). Also the items that are incorporated into the finance plan as well as the order of the presentation of the individual items equal each other.

The differences between the two schemes result from the number of sub-sectors presented and the terms that are connected with them (Cash Flow from Operating Activities, Cash Flow from Investing Activities, Cash Flow from Financing Activities or Cash Flow, Working Capital, Long-term Sector and Shareholder Sector, respectively).

Figure 5: Finance Plan 3-Step Scheme and Finance Plan 4-Step Scheme

The differing structures refer only to the presentation form or break-down of the finance plan and has no effect on the result of the finance plan or the connections between profit plan, finance plan and budgeted balance sheet.

Profit Plan | Finance Plan

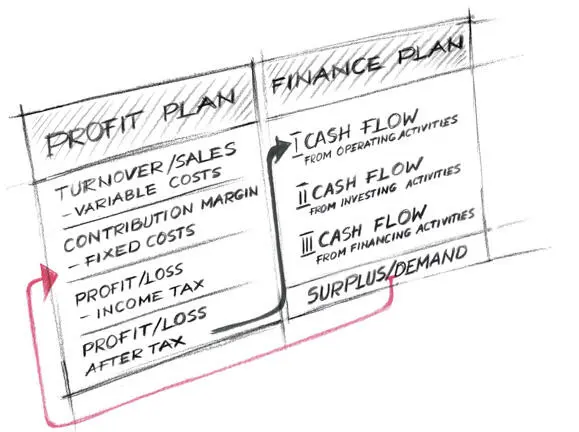

Profit plan and finance plan are linked to each other in two directions. There are links and connections from profit plan to finance plan and also back again from finance plan to profit plan.

On the one hand, the profit/loss after tax from the profit plan forms the basis for the finance plan. The result of the finance plan, the surplus of or the demand for cash, must either be financed or can be invested. The resulting income from interest or interest paid affects the profit plan.

Figure 6: Profit Plan and Finance Plan

In detail, starting from the profit plan, there are a number of connections towards the finance plan.

Like that, the profit/loss after tax from the profit plan forms the starting point for the finance plan. Further connections between profit plan and finance plan result from depreciation and provisions which have already been considered in the profit plan – as well as possibly from reserves and goods on own account (capitalized).

Depending on the time allowed for payment of receivables and liabilities, connections arise between the variable part of the profit plan (turnover and use of goods respectively as well as possibly varying purchase of goods) and the finance plan. Changes of inventory or stock respectively in the finance plan have either a liquidity improving or deteriorating effect, similar to the changes in deferred charges or deferred income.

Further effects on the liquidity which also are presented in the finance plan – which however, have not been derived from the profit plan compiled before – result from taking into account the effects of investments, credit increases or redemptions, capital increases or dividends.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Management Accounting. Workbook 2»

Представляем Вашему вниманию похожие книги на «Management Accounting. Workbook 2» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Management Accounting. Workbook 2» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.