Scott Pape - The Barefoot Investor

Здесь есть возможность читать онлайн «Scott Pape - The Barefoot Investor» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:The Barefoot Investor

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

The Barefoot Investor: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «The Barefoot Investor»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

That’s a bold claim, given there are thousands of finance books on the shelves.

Yet there’s a reason this book is in one in every 20 Australian homes.

You’ll find out how to create an entire financial plan that is so simple you can sketch it on the back of a serviette … and you’ll be able to manage your money in 10 minutes a week.

The Barefoot Steps stand the test of time. In this classic edition, you’ll get the skinny on:

Saving up a six-figure house deposit in 20 months Doubling your income using the ‘Trapeze Strategy’ Saving $77641 on your mortgage and wiping out almost 7 years of payments Handing your kids (or grandkids) a $140000 cheque on their 21st birthday Why you don’t need $1 million to retire …with the ‘Donald Bradman Retirement Strategy’ Sound too good to be true? It’s not.

This book is full of stories from everyday Aussies—single people, young families, empty nesters, retirees—who have applied the Barefoot Steps, freed themselves from crippling debt and achieved amazing, life-changing results.

The Barefoot Investor — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «The Barefoot Investor», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

So let's get into it.

Now, I'm not just going to waffle on about generic accounts — we're in this together, so I'm also going to show you exactly the accounts I used myself.

I'm going to take you through them one by one, and at the end I'll put it all together for you in a simple ‘menu’ for you to follow when you go on your first Barefoot Date Night.

Banishing bank fees from your life forever

‘What do you look for in your banking relationship?’ a bank executive once asked me.

‘I'm sorry, but I'm just not looking for a relationship with a bank right now,’ I told him, and then added, ‘it's not me, it's you'.

I am not loyal to any financial institution.

Banks are giant corporate octopuses with tentacles that wrap around you and squeeze out as much money as they can.

In 2020, the average Australian household was getting whacked $395 a year. Makes sense when you think about it — how else could four businesses make $30 billion a year in profits in a country with just 25.5 million people?

Rant over.

The bottom line is that it doesn't pay to be loyal.

What you need from your bank is a dead-simple, zero-fee solution.

Spare me all the convoluted ‘Terms & Conditions’ and fine print: ‘If you deposit $125 a month and don't withdraw it for 3 years, we'll pay you a bonus 0.16 per cent for the first 2 months, at which time it will revert back to our standard variable rate’.

Huh?

Just give me zero fees. As in doughnuts. None. Ever.*

(*And that includes no ATM fees. Ever.)

I don't care if I'm at one of those weirdly named convenience stores that has one of those weirdly named ATMs charging you an arm and half a leg to get your dough. Not my problem. I'm not paying for it.

Contrast this with what happened a few years ago to a friend of mine who banks with ANZ. I spent 30 minutes with him one night trudging around the city in the rain looking for his ATM: ‘I swear it was on the corner of Collins and Swanston!’ he moaned while I stood there shivering, hating him.

My zero-fee everyday transaction account

If you had stolen my wallet back in 2016, here's what you'd have found:

A picture of me and my golden retriever, Buffett, frolicking on the grass, and …

My ING Orange Everyday debit card.

At the time, this was a corker of an account. Maybe it still is. (And remember: I got paid nothing for that mention. I'm fiercely independent and have no tie-ups with any financial institution, whatsoever.)

I chose that account because it had zero fees. As in none. Not even when you're overseas.

Whip out your phone and do a quick search to find the best deal right now.

Zero fees. That's what you're looking for. Google it.

In fact, I like this kind of account so much I want you to set up two of them.

And I want you to give them nicknames (this is easy to do with online banking — just ask your bank if you're not sure how it works).

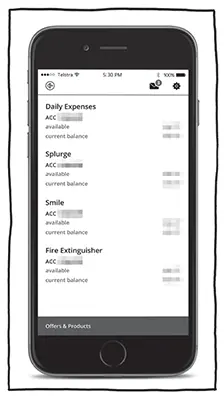

Call one ‘Daily Expenses’ and the other ‘Splurge’. Trust me on this — exactly why I'm asking you to give them these nicknames will be revealed in Step 2.

Any downsides to look out for? Well, you might find that you need to deposit a minimum amount into one of the accounts every month. You can easily make this your wage, for example, straight into ‘Daily Expenses’.

Since this book has sold a truckload of copies, there are plenty of banks piggybacking off the buckets set-up. A quick google will reveal who they are.

Steal my wife's purse

Now if you stole my wife's purse … she'd be very upset.

And you'd find the same debit card as mine (and a lovely picture of our family — no dogs).

See, one of our iron-clad rules is that we keep the same account.

No, not like cute matching cards so that we're colour coordinated. And no, not just one card between us. (That would be weird: ‘Honey, I'm just popping down the shops. Can I have the card?’)

What I mean is that we have separate cards for the same bank accounts.

And, most importantly, we have an agreement that we can each spend up to $400 on whatever we choose. No need to ask for permission. Anything over that we talk about, and make a joint decision.

(And that's a good thing. Personally, I am deeply offended by how much her hairdresser charges. My barber hasn't changed his ‘$20 short back and sides’ pricing in 15 years. Though, admittedly, she looks a lot better than I do.)

It's my firm belief that if you're in a healthy, trusting relationship, you should be sharing the same bank account, and all your finances.

That said, I've sat across the table from many women (and yes it's almost always women), whose partners have used money as a form of control. One of the first things I do is help them to set up a separate escape fund, so they can (eventually) get the hell out of there. If you think this could happen to you, don't share any accounts.

If you're already in this situation, I strongly suggest you sit down with a financial counsellor (call 1800 007 007) and get a game plan sorted.

Get some interest, brah!

You need to earn a decent interest rate on your savings. Granted, when interest rates are low, earning enough interest each year to buy a soap on a rope is almost mission impossible .

Yet that doesn't mean you should keep all your dough in your everyday transaction account, which pays ‘two parts of bugger-all’ (that is actually a finance term) in interest.

What you want is separate online saver accounts that are linked to your everyday transaction account.

In addition, you want the ability to move your money when needed and to set up automated triggers (we'll get to that later in Step 2, where we'll put your money on autopilot so you don't have to continually make decisions).

My linked high-interest online savings accounts

Back in 2016, for high-interest online savings accounts I used ING Savings Maximisers that were linked to my ING Orange Everyday account.

I want you to set up two of these accounts — and again I want you to give them nicknames. Call one ‘Smile’ and the other ‘Fire Extinguisher’.

(WTF, Barefoot! These names are getting crazier by the minute! Trust me on this and I'll explain all in Step 2.)

Here's a screenshot of my set-up.

By the way, with these online saver accounts I am not a ‘rate tart’. I have no interest in switching accounts every time some other institution offers a piddly 0.15 per cent extra interest. It's just not worth my time.

(You may have more time on your hands, perhaps because you live at home with your mum and she does your ironing and plaits your hair, leaving you free to pore over spreadsheets on a Saturday night. If that's you, feel free to check out comparison sites like RateCity, Mozo or finder.com.au, where you can usually find bank accounts paying a bee's dick — another finance term — more interest than the one you have chosen.)

In summary:

Zero fees. Good interest. All in one account.

Simple.

In any event you'll notice that I deal exclusively with online banks for these accounts. There's a reason for this: they do better deals because they've got lower overheads.

Plus, they're fighting against the Big Four, who rely on a mixture of apathy and a reputation for safety (which is rubbish, because the government guarantees all deposits — up to $250 000 per financial institution — for all local and international authorised deposit-taking institutions).

Читать дальшеИнтервал:

Закладка:

Похожие книги на «The Barefoot Investor»

Представляем Вашему вниманию похожие книги на «The Barefoot Investor» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «The Barefoot Investor» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.