Mahendra Ramsinghani - The Business of Venture Capital

Здесь есть возможность читать онлайн «Mahendra Ramsinghani - The Business of Venture Capital» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:The Business of Venture Capital

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

The Business of Venture Capital: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «The Business of Venture Capital»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

has been hailed as the definitive, most comprehensive book on the subject. Now in its third edition, this market-leading text explains the multiple facets of the business of venture capital, from raising venture funds, to structuring investments, to generating consistent returns, to evaluating exit strategies. Author and VC Mahendra Ramsinghani who has invested in startups and venture funds for over a decade, offers best practices from experts on the front lines of this business.

This fully-updated edition includes fresh perspectives on the Softbank effect, career paths for young professionals, case studies and cultural disasters, investment models, epic failures, and more. Readers are guided through each stage of the VC process, supported by a companion website containing tools such as the LP-GP Fund Due Diligence Checklist, the Investment Due Diligence Checklist, an Investment Summary format, and links to white papers and other industry guidelines. Designed for experienced practitioners, angels, devils, and novices alike, this valuable resource:

Identifies the key attributes of a VC professional and the arc of an investor’s career Covers the art of raising a venture fund, identifying anchor investors, fund due diligence, negotiating fund investment terms with limited partners, and more Examines the distinct aspects of portfolio construction and value creation Balances technical analyses and real-world insights Features interviews, personal stories, anecdotes, and wisdom from leading venture capitalists

is a must-read book for anyone seeking to raise a venture fund or pursue a career in venture capital, as well as practicing venture capitalists, angel investors or devils alike, limited partners, attorneys, start-up entrepreneurs, and MBA students.

The Business of Venture Capital — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «The Business of Venture Capital», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

Those who have analyzed his historic investment track record point to the fact that even if you slice off the biggest win — his Alibaba investment — the rest of his portfolio shows above 40 percent internal rate of return (IRR). When the industry average performance is in the mid-teens, having such a significant edge in investment performance helps. Combine that with a boldness of vision and the ability to execute on a global investment strategy and voilà — you have $45 billion in 45 minutes.

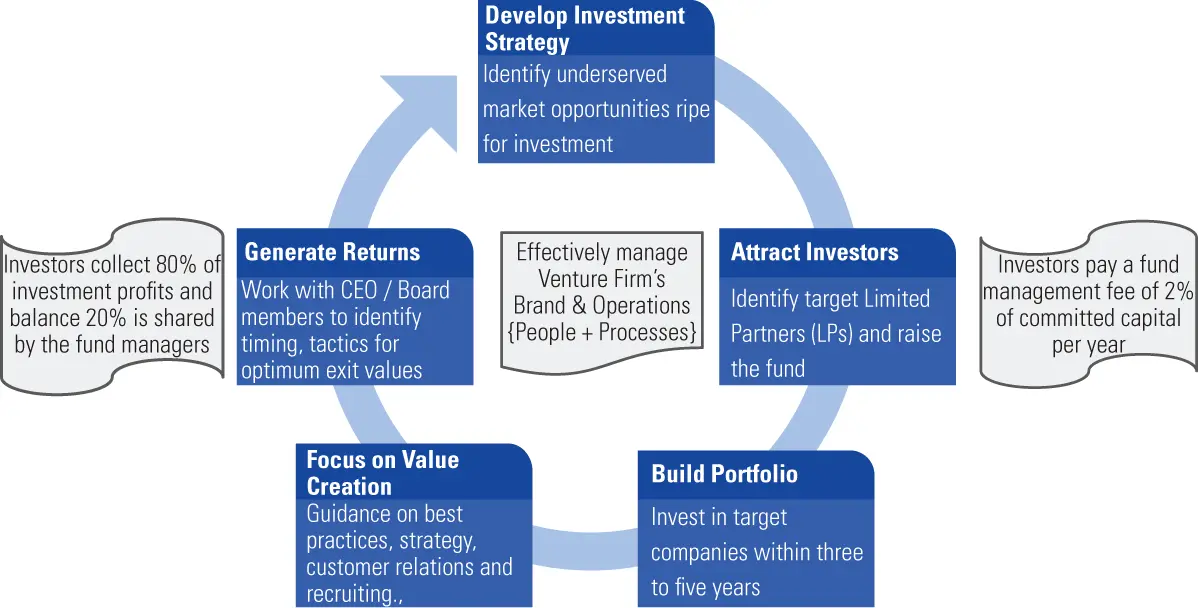

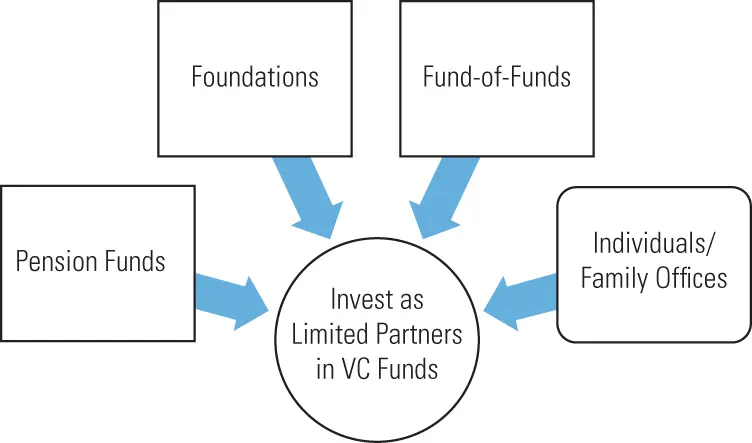

The venture capitalist's journey often begins with the ability to raise a venture fund ( Exhibit 1.1). The universe of investors in any venture fund includes two broad categories: (a) institutional investors such as pension funds, foundations, university endowments, sovereign wealth funds, business corporations, and (b) high-net-worth individuals (HNWIs) and their family offices (see Exhibit 1.2). Institutional investors primarily view venture funds as an asset class, a money-making machine that promises to deliver an annualized “risk-adjusted” IRR.

Exhibit 1.1 Venture capital business model.

Exhibit 1.2 Limited partners.

The VC business model is simple: a venture capitalist, or general partner (GP), knocks on the door of various investors, known as limited partners (LP), to raise a fund. LPs agree to invest in venture funds based on the venture capitalist's background, investment expertise and past performance, a compelling investment strategy, and, to some extent, that mystical X factor — an amalgamation of ability, skills, and luck that defies any logical construct and makes one practitioner more successful than the others.

The two groups — the GP as the investment manager and the LP as the provider of capital — form a 10-year partnership. The LP agrees to pay the GP a management fee each year and a share in a percentage of the profits. In turn, the GP agrees to work night and day to find hot, blazing startups, to invest the capital, turn them into unicorns (billion-dollar valued companies), and harvest the money back in large multiples. The end game for the LP is to make a superior risk-adjusted financial return. The primary measure of success for the venture firm is the IRR and cash-on-cash (C-on-C) return, a multiple of the original investment amount or multiple of invested capital (MOIC). Venture firms and GPs live, and are slaughtered by, these two metrics.

To better understand the economics, take the example of a $100 million fund. The GPs of the fund would invest this capital in, say, about a dozen companies and after building value aspire to “exit” the investments, meaning to sell the ownership. Should these investments generate profits, the investors (or LPs) keep 80 percent of the profits, and the GPs take home 20 percent. The profit, called carried interest or carry, where one-fifth profits were shared, has evolved from the time of Phoenicians, who in the year 1200 CE commanded 20 percent of profits earned from trade and shipping merchandise. In addition to the carry, the LPs also pay the GPs an annual management fee, typically 2 to 2.5 percent of the committed capital per year. Thus, for a $100 million fund with a predetermined life of 10 years, annual fees of 2 percent yield $2 million for the firm. The fees provide for the day-to-day operations of the firm and are used to pay for salaries, travel, operational, and legal expenses. The responsibilities and compensation packages are determined by the professional's responsibilities and experience.

A venture fund is defined as a fixed pool of capital raised for investing per an agreed-upon investment strategy. A venture firm manages this fund, and, over time, a firm can manage multiple funds. The GPs are the primary investment decision makers and are supported by a team of investment and administrative professionals.

To get a venture fund off the ground, several such investors have to be pitched, engaged, convinced, cajoled, and even threatened to commit to a fund. This is often a long, arduous journey for most venture professionals. Fundraising stretches every thread — salesmanship, tenacity, and fortitude. To start with, it's never easy to identify the right target set of investors. It's like searching for a black cat in a dark room — often, the cat does not exist and you can spin around in the dark room. Assuming you can build a target list of fund investors, all the classical challenges of any sales process come into play. Getting in the door, engagement with the decision makers, pushing to a close with not one but at least a dozen or more investors requires special talents. Seldom do investors respond promptly, offer clear feedback on their decision-making criteria, process, and time lines.

Building momentum amongst a group of disparate investors to reach a satisfactory fund size takes as much as 18 months and is often compared to an uphill crawl on broken glass. Attracting, engaging, and assembling a large number of investors is often like a game of house of cards. If one of them pulls out early in the process, a cascading effect can occur. For every fund that makes it to the finish line, at least three die a premature death, littering the venture graveyards with unfulfilled ambitions, ill-timed strategies, and broken partnerships that never got off the ground.

Once the “fund” is subscribed to its target amount, it is closed and no new investors are admitted. The life of such a fund is typically 10 years, during which the venture professionals build a portfolio of companies and aspire to generate returns. The fund is typically dissolved after the tenth year, or when all portfolio investments have been liquidated.

After the fundraising process is complete, venture professionals are under pressure to deploy the capital. During this investment period, startups come in, investors check them out, and the mating dance begins. Pitch decks, term sheets, valuations, and board seats are negotiated as a venture fund builds a portfolio of 20–24 companies within three to five years. A typical portfolio size for any fund can be 10–30 companies, based on the sector and stage of investment.

ROLES, RESPONSIBILITIES, AND COMPENSATION

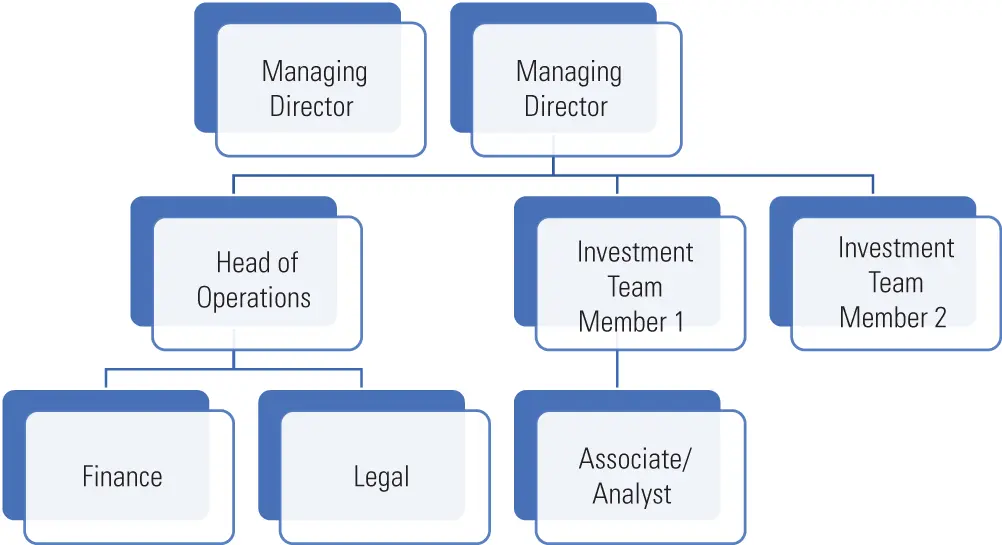

In any venture firm, the cast of characters includes the GPs (also known as managing directors or managing GPs), vice presidents, principals, associates, and analysts ( Exhibit 1.3). These primary investment professionals are responsible for generating returns. Newer titles have evolved as fund operations have become more focused. For example, in larger funds, roles such as director of business development or the head of deal sourcing have emerged. The administrative team, also referred to as the back office, is responsible for the day-to-day operational aspects. This team includes chief operating officer, chief financial officer, general counsel administrative, and human resources.

Exhibit 1.3 Fund organization chart.

The primary responsibilities of the investment team differ along the lines of seniority. On any typical day, the GPs would juggle a number of activities: negotiating terms for investment opportunities, participating in boards of current portfolio companies, responding to any LP/investor requests, and putting out a few fires along the way. On a rare day, exit negotiations may occur. An entry-level analyst is expected to source investment opportunities and conduct the first screening of due diligence. At the other end of the spectrum, the partners keep a close watch on portfolio construction, governance, exits, and strategy and timing of the next fund. The typical compensation package includes a salary, annual performance bonus, and a share of the profits called carry, which stands for carried interest.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «The Business of Venture Capital»

Представляем Вашему вниманию похожие книги на «The Business of Venture Capital» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «The Business of Venture Capital» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.