Hans Lind - Advanced Issues in Property Valuation

Здесь есть возможность читать онлайн «Hans Lind - Advanced Issues in Property Valuation» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Advanced Issues in Property Valuation

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Advanced Issues in Property Valuation: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Advanced Issues in Property Valuation»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

, real estate valuation experts and authors Hans Lind and Bo Nordlund provide a deep understanding of the concepts, theories, methods and controversies in property valuation. The book introduces readers to controversies and discussions in real estate valuation, including the relevance of market value for valuation for lending purposes, how uncertainty in property valuations should be interpreted, and the relationship between market value and fair value in financial reporting.

Readers will also benefit from the inclusion of:

A thorough introduction to the concepts, theories, methods and problems in real estate property valuation An exploration of the relevance of market value for valuation for lending purposes A practical discussion of how uncertainty in property valuations should be interpreted A concise treatment of the relationship between market value and fair value in financial reporting An examination of how concerns about sustainability and other structural changes can affect property valuation Perfect for graduate level students in courses involving valuation or real estate,

is also an excellent resource for real estate practitioners who wish to update and deepen their knowledge about property valuation.

Advanced Issues in Property Valuation — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Advanced Issues in Property Valuation», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

A market value should not be mixed up with a ‘forced sales’ value. A forced sale could end up with a lower price than what could have been expected because of limited time to expose the property on the market. Therefore, transactions classified as forced sales may not be appropriate to use as comparable sales. However, a valuer should also take the following into account when evaluating whether a transaction should be regarded as forced or not (see IVSC 2019 , p. 26):

Sales in an inactive or falling market are not automatically ‘forced sales’ simply because a seller might hope for a better price if conditions improved. Unless the seller is compelled to sell by a deadline that prevents proper marketing, the seller will be a willing seller within the definition of Market Value

(see IVSC 2019, paras 30.1–30.7).

2.8 Problem 5: Market Value and Turnover

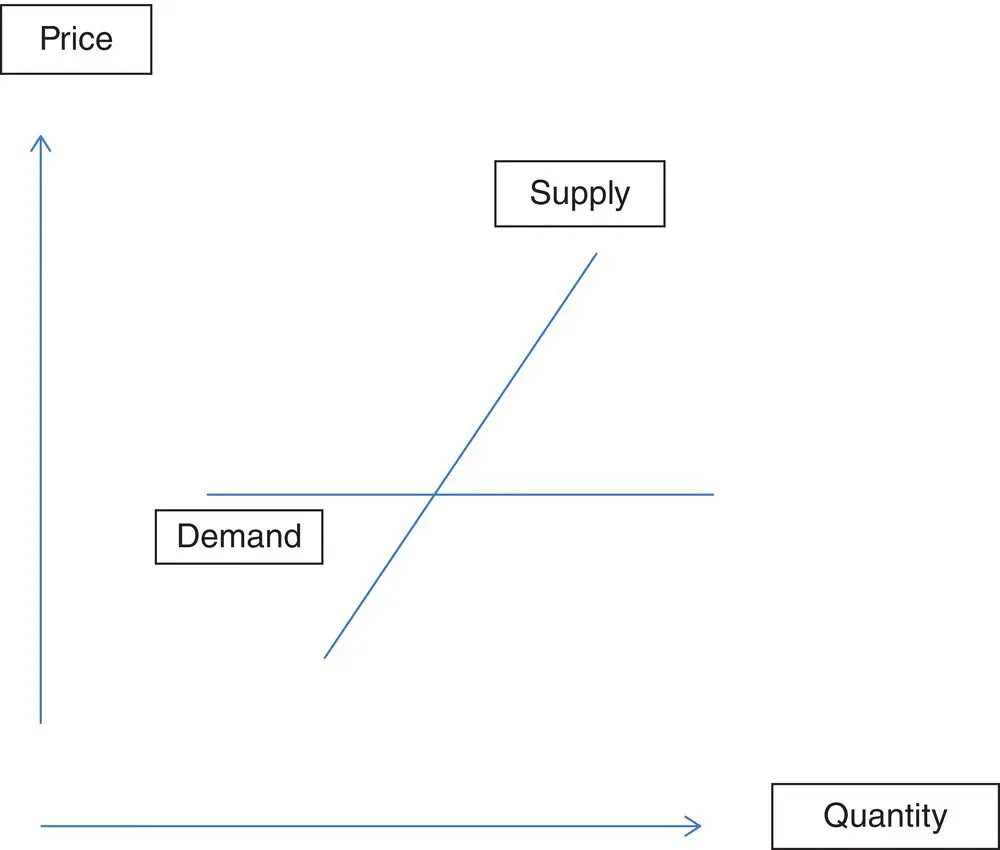

There are no references to turnover in either of the definitions of market value presented in the beginning of this chapter. The most probable explanation for this is that the definitions assume that there is a considerable number of potential buyers that are willing to buy a property for roughly the same price, e.g. on an active housing market with many similar properties. In such a situation, the demand curve is almost horizontal in a rather large interval on the quantity‐axis. A consequence of this is that changes in turnover will not have a strong effect on the price. This is illustrated in Figure 2.1.

But how realistic is really this assumption? In the commercial real estate market, possible buyers may have rather different views on the potential of a property and the future development of the market where the property is located. On the residential market, actors might differ in preferences, in their incomes and in their expectations about the future development of the market. In both cases, the reservation prices of the actors on the market might differ considerably. Differences in knowledge may also lead to differences in reservation prices. The effect of these differences in reservation prices is that there will be a downward sloping demand curve, and that the expected price – the market value ‐ will depend on the number of properties that are put on the market during a certain period of time. However, it is also important to bear in mind that the market value concept in itself is independent of the numbers of transactions in the market. If there is a small number of transactions, or maybe no transactions at all, the aim when estimating market value is still to find a hypothetical price in a transaction on market terms at the value date. (We will discuss issues connected to valuation methods that may be applied in thin markets more in detail in Chapter 3, and especially in the context of so‐called ‘actor‐based methods’.)

Figure 2.1 Price and quantity with an almost horizontal demand curve.

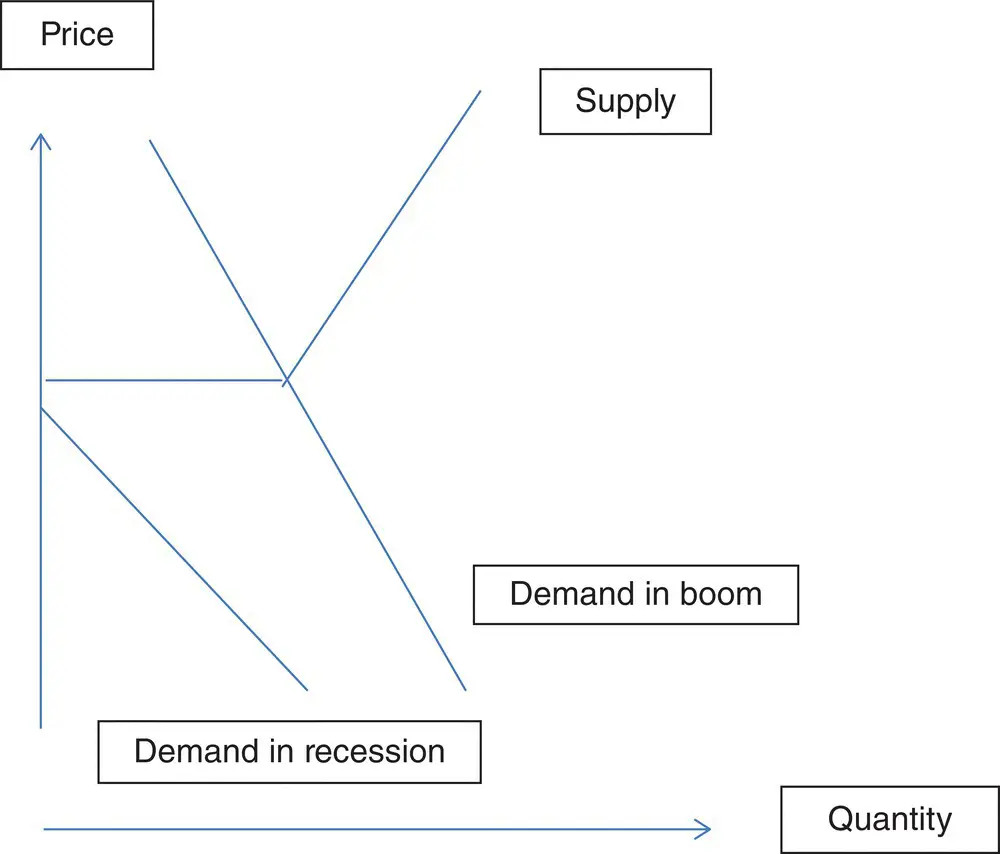

Haurin (2005 ) discusses changes in liquidity/turnover in the context of creating a real estate price index. The variation in turnover during the business cycle will smooth prices, as prices will not rise so much when more properties are put on the market during the boom, and not fall so much when turnover goes down during a recession. An extreme case is illustrated in Figure 2.2, where no property owner is willing to sell at a price below the current one. The supply curve is then horizontal at the current price up to the current level of turnover. A fall in demand will in such a situation lead to a fall in turnover, but the observed prices will not fall. It has been argued that this is actually what happened in Sweden when the financial crisis hit the real estate market in the fall of 2008. The current owners were financially stable and did not sell when demand fell. The market died and there were almost no transactions and no new prices were observed on the market, which created problems for valuers.

A low interest rate can make these fluctuations in turnover stronger. The low interest rate can make it easier to hold out when there is a downturn in demand as debt costs fall. A low interest rate also makes it less costly to wait and therefore the expected future prices do not have to be so much higher than the current price in order to make it rational to wait. Assume that the current market value – in the recession – is 100. If the rate of return demanded is 10%, then it is rational to wait if the price in a year is expected to be higher than 110. But if the rate of return demanded is 4%, then it is rational to wait if the price in a year is expected to be higher than 104.

Figure 2.2 Price and quantity with a partly horizontal supply curve.

The underlying ‘problem’ is that transactions are voluntary and that the willingness to buy and sell depends on market conditions. Observed transactions are not the result of a random selection of properties that is put on the market. Given the economic conditions, institutional structure and the beliefs of the actors, a certain change in demand can lead to very different reactions on the market: In some cases, transaction volumes fall much and prices only a little, while in other cases, observed prices fall much but turnover only a little. The development during the financial crisis 2008 can illustrate this where observed prices for commercial property hardly fell at all in Sweden while they fell much and quickly in England (see Crosby et al. 2010 ) – even though the underlying fall in GDP was roughly the same.

It might not be necessary to make assumptions about turnover explicit in the definition of market value, but it could be an advantage to add a clause saying ‘given expected turnover’ in the definition. The relation between turnover and price, when there is a downward sloping demand curve, will, however, affect uncertainty in the estimation of market value. This will be returned to both in Chapter 4on uncertainty and in Chapter 6, where we discuss exit prices in thin markets in the context of valuation for financial reports.

2.9 Highest and Best Use

Both IVSC (2019 ) and Appraisal Institute (2013 ) use the concept of ‘Highest and best use’. IVSC (2019 , p. 25) writes, ‘The market value of an asset will reflect its highest and best use’ and this is explained in terms of the use that maximizes its potential (given what is possible, legally permissible and financially feasible). Similar formulations can be found in Appraisal Institute (2013 , p. 42).

There are problems with this concept and our recommendation is that it should be used with a great degree of caution when market value is discussed. The requirements for empirically extracted ‘evidence’ should be high if, or when, this concept is claimed to have affected an estimated market value‐figure. As will be returned to in Chapter 8, the typical situation in a market is that actors have different knowledge, different expectations and different plans for a specific property. One actor may see possibilities that other actors initially are not aware of. An example discussed in Chapter 7is that one investor sees that a certain building can be made green with a rather small investment. More theoretically, this can be described in terms of different views on the real options that a property has. In a market, actors typically gain by not giving away information and not telling others what their plans are. Investors may have plans that valuers are not aware of. If only one actor is aware of certain profitable opportunities that ‘highest and best use’ will not affect the bids of others are therefore not the price if the property is sold by a standard English auction, where bids are presented in ascending order until there is only one bidder left.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Advanced Issues in Property Valuation»

Представляем Вашему вниманию похожие книги на «Advanced Issues in Property Valuation» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Advanced Issues in Property Valuation» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.