Werner Seebacher - Management Accounting. Workbook 1

Здесь есть возможность читать онлайн «Werner Seebacher - Management Accounting. Workbook 1» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Management Accounting. Workbook 1

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Management Accounting. Workbook 1: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Management Accounting. Workbook 1»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

The textbook «Management Accounting.» describes in detail the Big Picture – the central overall connection in accounting/controlling – as well as the elements which affect this connection: Balance Sheet | Profit/Loss Account | Profit Plan | Finance Plan | Budgeted Balance Sheet.

The «Workbook 1 – Balance Sheet | Profit/Loss Account» is based on the textbook «Management Accounting.» and presents and explains in detail – in form of numerical examples – the effects of concrete accounting activities and business cases in and on balance sheet and profit/loss account.

Target groups of «Management Accounting. Workbook 1 – Balance Sheet | Profit/Loss Account» are students of economic/business courses in the framework of their basic education or in the framework of their introductory courses, students doing post-graduate programmes, as well as managers in enterprises with practical experience – all of them facing the challenge of having to understand and to apply the basic connections of accounting in enterprises – presented in and through balance sheet and profit/loss account.

"Management Accounting. Workbook 1 – Balance Sheet | Profit/Loss Account" is supplemented and continued by «Management Accounting. Workbook 2 – Profit Plan | Finance Plan | Budgeted Balance Sheet»."

Management Accounting. Workbook 1 — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Management Accounting. Workbook 1», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

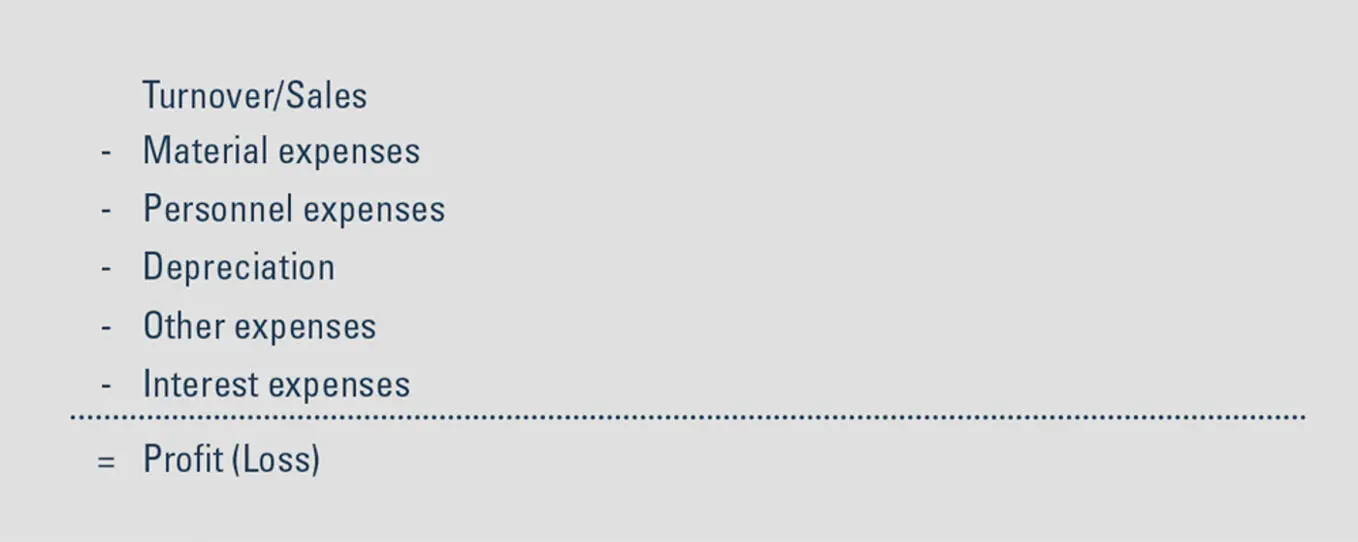

As an alternative to the account form, the profit/loss account can also be presented in the so called report form. Again in its simplest form the report form follows the following structure:

Figure 6: Profit/Loss Account, Report Form

The resulting profit or loss is identical in both versions. The difference between the two versions happens like that:

In the profit/loss account in the account form, a list of all expenses is compiled which is contrasted to all income (turnover). The difference between the total income (turnover) and the total expenses results in the profit or loss.

The profit/loss account in the report form, however, starts with the turnover/sales in the first line from which – step by step – the individual expense items are taken off in the following lines, until finally a profit or loss remains.

In the numerical examples which are presented in the “Workbook 1 – Balance Sheet | Profit/Loss Account”, for presenting the profit/loss account, the presentation in form of accounts has been chosen on purpose, in contrast to the presentation in a report form, as the effects of business activities in the context of profit/loss account and balance sheet (which is also presented in the account form) can be more easily presented and can be better and more easily understood in the form of accounts.

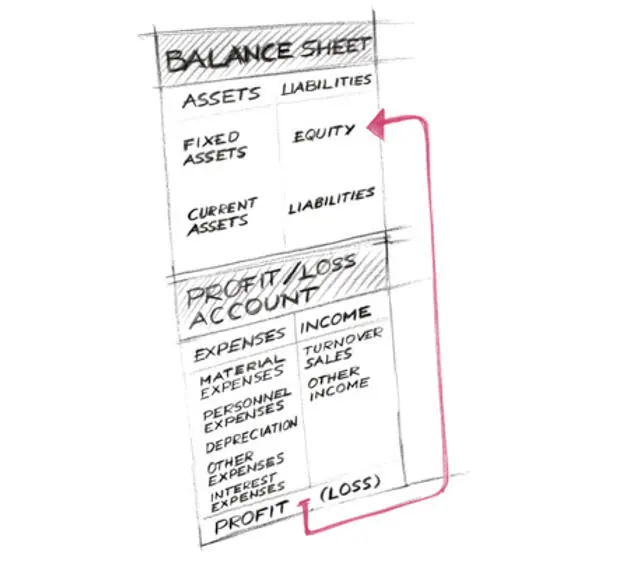

BALANCE SHEET | PROFIT/LOSS ACCOUNT – CONNECTION

Figure 7: Balance Sheet and Profit/Loss Account

The connection between balance sheet and profit/loss account can be seen in the result of the profit/loss account – in the profit or loss.

The basis for the presentation of the economic connections in an enterprise is the opening balance sheet at the beginning of the business year. When an enterprise is founded, it is the opening balance sheet, in an existing enterprise it is the closing balance sheet of the previous year that is taken as the opening balance sheet for the subsequent year.

The development or the result of the business year respectively is presented in the profit/loss account. All expenses and all income which have occurred in the course of a business year in an enterprise are incorporated into the profit/loss account. Like that, the profit/loss account summarizes the result or the profit respectively of the business activity of an enterprise.

The balance sheet at the end of a business year (the closing balance sheet) presents how the enterprise is structured at the end of the business year, how the assets are composed whether of fixed or current assets and how the capital is composed, of equity or debt capital. It must be considered however, that the equity capital was changed by the profit or loss that was transferred from the profit/loss account.

So, the profit or loss are the central elements in connection between the profit/loss account and the balance sheet, and this in two ways:

The profit or loss are the central result of the profit/loss account.

However, the profit or loss also form the central connection between profit/loss account and balance sheet: a profit from the profit/loss account increases the equity in the balance sheet, a loss reduces the equity in the balance sheet.

BALANCE SHEET | PROFIT/LOSS ACCOUNT – procedure

In its simplest form the compilation of balance sheet and profit/loss account follows the following procedure:

After presenting all business activities in balance sheet and profit/loss account, balance sheet and profit/loss account are closed.

In a first step, the sum total of the total expenses and the sum total of the total income are compiled. If the income exceeds the expenses for the business year, it results in a profit. If, however, the expenses exceed the income, it leads to a loss.

This profit or loss from the profit/loss account now affect the balance sheet: a profit from the profit/loss account increases the equity in the balance sheet, a possible loss reduces the equity in the balance sheet.

After allocating the profit or loss from the profit/loss account to equity capital in the balance sheet, the two sums on the left and on the right side are compiled finally. These two sums of the balance sheet must now match, if all business cases have been presented correctly and fully in the profit/loss account.

It is crucial for the numerically correct compilation of the balance sheet together with the profit/loss account to follow a quite simple rule: every figure that has been entered into a profit/loss account or a balance sheet respectively, must affect balance sheet or profit/loss account a second time.

Only like that, you can make sure that the balance sheet matches, that both sides of the balance sheet result in the same balance sheet total in the end.

In this connection it must be taken into account that certain business activities only affect the balance sheet of an enterprise, others however, affect the balance sheet and the profit/loss account.

Balance Sheet | Profit/Loss Account – Numerical Examples

The following numerical examples presented in the “Workbook 1 – Balance Sheet | Profit/Loss Account” are designed for making the context between Balance Sheet and Profit/Loss Account clear.

As explained at the beginning, the “Workbook 1 – Balance Sheet | Profit/Loss Account” contains no bookings or entry formulas – on purpose – to present the connections between balance sheet and profit/loss account. Instead, the content-oriented relationship of the business activities and their direct effects on balance sheet and profit/loss account are presented.

The numerical examples presented are based on a simplified structure of the balance sheet and a simplified structure of the profit/loss account.

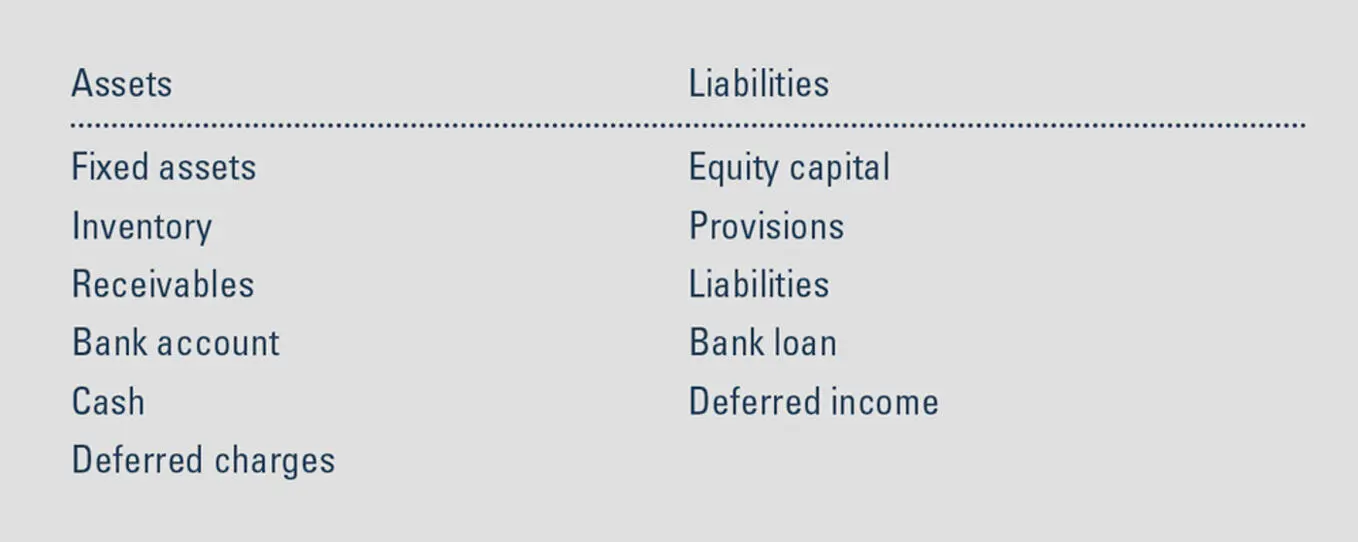

The simplified balance sheet structure of the numerical examples contains the following items – according to the design of the examples:

Figure 8: Balance Sheet, Structure for Numerical Examples

In the simplified structure of the profit/loss account used for the numerical examples, there are five central types of expenses which typically show up in the profit/loss account of an enterprise: material expenses, personnel expenses, depreciation, other expenses, interest paid.

The presentation is simplified in so far, as items such as Other Income, Income from Participations and Taxes are not taken into account. In the numerical examples presented, Other Income is added to the above mentioned expense items and to Turnover/Sales in the profit/loss account, if needed.

The simplified structure of the profit/loss account in the numerical examples contains the following items – according to the design of the example:

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Management Accounting. Workbook 1»

Представляем Вашему вниманию похожие книги на «Management Accounting. Workbook 1» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Management Accounting. Workbook 1» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.