Andrew E. Baum - Property Investment Appraisal

Здесь есть возможность читать онлайн «Andrew E. Baum - Property Investment Appraisal» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Property Investment Appraisal

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Property Investment Appraisal: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Property Investment Appraisal»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

This book explains the process of property investment appraisal: the process of estimating both the most likely selling price (market value) and the worth of property investments to individuals or groups of investors (investment value).

Valuations are important. They are used as a surrogate for transactions in the measurement of investment performance and they influence investors and other market operators when transacting property. Valuations need to be trusted by their clients and valuers need to produce rational and objective solutions. Appraisals of worth are even more important, as they help to determine the prices that should be paid for assets, even in times of crisis, and they can indicate market under- or over-pricing.

In a style that makes the theory as well as the practice of valuation accessible to students and practitioners, the authors provide a valuable critique of conventional valuation methods and argue for the adoption of more contemporary cash-flow methods. They explain how such valuation models are constructed and give useful examples throughout. They also show how these contemporary cash-flow methods connect market valuations with rational appraisals.

The UK property investment market has been through periods of both boom and bust since the first edition of this text was produced in 1988. As a result, the book includes examples generated by vastly different market states. Complex reversions, over-rented properties and leaseholds are all fully examined by the authors.

This Fourth Edition includes new material throughout, including brand new chapters on development appraisals and bank lending valuations, heavily revised sections on discounted cash flow models with extended examples, and on the measurement and analysis of risk at an individual property asset level. The heart of the book remains the critical examination of market valuation models, which no other book addresses in such detail.

Property Investment Appraisal — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Property Investment Appraisal», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

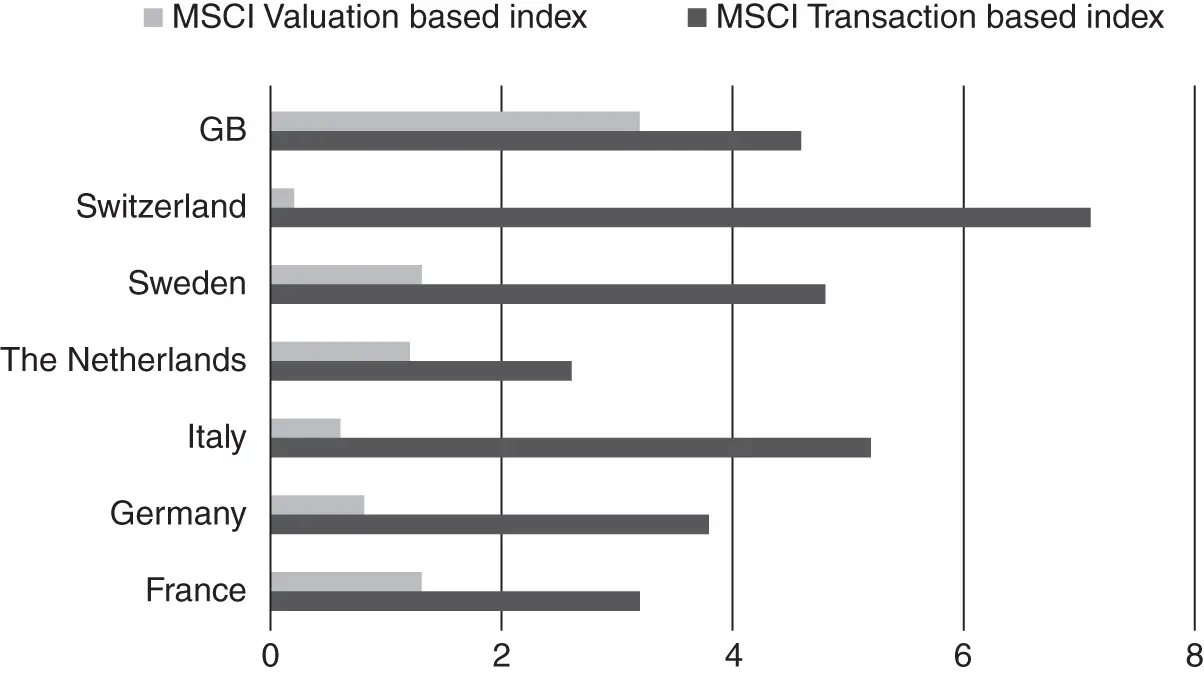

Source: MSCI (2019).

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Australia | 0.4 | −0.1 | 0.0 | 1.8 | 1.3 | 0.4 | 6.0 | 11.8 | 3.5 | −4.6 | 1.4 | 3.6 | −0.3 | 3.2 | 7.4 | 12.2 | 4.2 | 8.0 | 5.9 |

| Canada | −1.3 | 0.7 | 2.0 | 2.5 | 6.5 | 5.5 | 15.4 | 10.4 | 5.8 | −0.4 | 1.5 | 6.8 | 14.4 | 3.6 | −0.4 | 11.8 | 7.7 | 6.1 | 8.1 |

| France | 2.5 | −0.2 | 1.2 | 2.5 | 8.8 | 8.6 | 12.9 | 10.4 | 3.5 | 0.9 | 5.6 | 10.6 | 5.9 | 5.1 | 3.7 | 9.2 | 5.3 | 7.5 | 9.5 |

| Germany | 3.6 | 1.2 | −3.3 | −4.8 | −1.1 | 0.8 | 0.0 | 11.5 | 9.7 | −3.0 | 5.2 | 7.3 | 4.2 | 2.8 | 4.0 | 6.5 | 6.1 | 13.8 | 6.5 |

| Italy | −5.5 | 12.7 | 7.9 | 19.1 | 1.0 | 6.1 | 13.9 | 16.2 | 3.9 | 0.9 | 3.1 | 1.9 | −4.4 | 0.1 | 2.4 | 0.3 | 7.1 | 1.0 | |

| Japan | 4.2 | 11.8 | 21.0 | 7.1 | 11.5 | 4.8 | −8.5 | −3.6 | −2.1 | −3.4 | 2.3 | 9.1 | 10.1 | 4.9 | 8.0 | 9.5 | |||

| Netherlands | 7.6 | 2.2 | 6.2 | 2.6 | 4.7 | 5.2 | 4.6 | 10.5 | 2.8 | −5.3 | 2.1 | 1.9 | −0.2 | −6.0 | −1.4 | −1.5 | 3.5 | 3.8 | 4.4 |

| South Africa | 0.5 | −3.0 | 0.5 | 1.4 | −0.4 | 6.7 | 0.4 | 18.1 | 1.4 | 6.6 | 0.8 | 5.4 | 6.4 | 7.7 | −0.3 | 1.3 | 1.1 | 0.7 | −0.6 |

| Sweden | −8.7 | 4.8 | 5.9 | 4.5 | 7.3 | 7.5 | 21.3 | 10.8 | −7.7 | 12.9 | 0.9 | 15.0 | 4.7 | 5.9 | 1.2 | 7.3 | 4.0 | 2.5 | 1.1 |

| Switzerland | 19.8 | 6.2 | 4.4 | 0.7 | 5.9 | 6.6 | 7.3 | 13.0 | 9.7 | 9.0 | 9.9 | 5.8 | 5.3 | 15.4 | 20.6 | 18.5 | 8.2 | ||

| UK | 3.8 | 3.4 | 5.1 | 5.5 | 6.0 | 5.8 | 6.6 | 2.9 | −2.9 | 3.8 | 5.2 | 6.2 | 2.7 | 7.3 | 8.6 | 6.2 | 3.0 | 6.2 | 4.5 |

| USA | −1.5 | 1.0 | 4.2 | 4.4 | 5.5 | 7.4 | 7.5 | 4.8 | −4.3 | −10.3 | 4.8 | 5.2 | 4.5 | 2.2 | 5.2 | 5.6 | 0.6 | 3.1 | 2.3 |

| Other | 3.8 | 6.2 | 5.8 | 6.2 | 11.2 | 12.5 | 13.3 | 9.4 | 5.6 | −0.7 | 1.3 | 5.8 | 2.6 | −0.1 | 0.4 | 6.8 | 11.1 | 5.8 | 10.7 |

| Global | 0.9 | 2.2 | 3.6 | 3.9 | 5.4 | 6.4 | 7.4 | 7.6 | 0.1 | 0.0 | 2.4 | 6.1 | 4.2 | 3.4 | 4.7 | 6.7 | 3.6 | 5.5 | 4.7 |

These analyses assume that sale prices are independent of valuations. However, Baum et al. (2000) found that valuations were not independent of prices and prior valuations played an important part in deciding which properties were bought and sold – and at what minimum price. On this basis, it would be expected that prices would exceed valuations generally, as funds are less likely to sell or buy at prices that do not meet the last valuation or the next prospective valuation. Some funds struggled to get trustee approval for selling at less than prior valuation and some buying funds checked formally that their portfolio valuer would at least confirm the purchase price at the next valuation before proceeding to purchase. Another example is that of German open-ended funds where the rules governing these funds prohibit sales of assets at amounts that are more than a few percentage points below the valuation. Prospective sale prices at less than valuation would not be completed, so the samples of sales would be biased towards cases where prices exceeded the prior or prospective market valuation. Therefore, a positive bias in any accuracy study should be expected.

The expectation that valuers will lag and smooth the peaks and troughs in prices has been discussed by Geltner et al. (2003) and in Geltner et al. (2007). These authors are not alone in suggesting that one of the reasons for valuations lagging market movements is anchoring by valuers on the information contained in past comparable transactions and valuations. Anchoring refers to a psychological tendency to rely on an initial known figure (such as a prior valuation) by more than would be justified from its relevance to the appraisal at hand. This is arguably quite rational behaviour given the nature of the valuation process and the need to minimise errors that arise from noisy contemporaneous market signals (Quan and Quigley 1991), as well as the possible requirement to justify the valuation in court. In less liquid markets (where liquidity is defined as the depth of transaction activity), the anchoring on past valuations is likely to be stronger.

However, the accuracy studies show that the gap between prices and valuations increases in booms, which is where transaction activity is at its greatest. This suggests that the speed or extent of value change has a major impact. New information may be available, but it might not be fed into valuations quickly enough to keep them abreast of rapidly rising prices. This raises questions for the organisation of valuation services. In some jurisdictions, valuers are separate from the marketplace and are housed within specialist firms. Yet, in many mature markets, valuations are undertaken by the same firms that carry out agency functions, thereby improving access to market intelligence or “soft” information that can feed into a valuation. This is in addition to past valuations and evidence from completed transactions.

S moothing relates to the extent to which valuations reduce the volatility of actual prices by missing the cyclical peaks and troughs of price movements. The impact of smoothing has been studied using individual valuations and valuation-based property performance indices. This includes attempts to quantify its extent, as summarised in Geltner et al. (2003). More recent analysis of a transaction index based on sales from the MSCI UK dataset (Devaney and Martinez Diaz (2011)) indicates that the current level of smoothing might be less than that found in previous studies, with the index being 1.4 times more volatile than an appraisal-based counterpart. Yet perhaps the most interesting finding was that, unlike other studies, particularly for the US (e.g. Fisher et al. 2007), the turning points appeared to be the same in both appraisal and transaction-based indices, suggesting that valuers might have smoothed the peaks and troughs, but not lagged turning points in the most recent cycle.

Figure 1.2 Volatility of valuation and transaction-based series (SD % pq): Q1 2002 to Q3 2019.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Property Investment Appraisal»

Представляем Вашему вниманию похожие книги на «Property Investment Appraisal» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Property Investment Appraisal» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.