Campbell R. Harvey - DeFi and the Future of Finance

Здесь есть возможность читать онлайн «Campbell R. Harvey - DeFi and the Future of Finance» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:DeFi and the Future of Finance

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

DeFi and the Future of Finance: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «DeFi and the Future of Finance»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

In

, Campbell R. Harvey, Ashwin Ramachandran and Joey Santoro, introduce the new world of Decentralized Finance. The book argues that the current financial landscape is ripe for disruption and we are seeing, in real time, the reinvention of finance.

The authors provide the reader with a clear assessment of the problems with the current financial system and how DeFi solves many of these problems. The essence of DeFi is that we interact with peers—there is no brick and mortar and all of the associated costs. Savings and lending are reinvented. Trading takes place with algorithms far removed from traditional brokerages.

The book conducts a deep dive on some of the most innovative protocols such as Uniswap and Compound. Many of the companies featured in the book you might not have heard of—however, you will in the future.

As with any new technology, there are a myriad of risks and the authors carefully catalogue these risks and assess which ones can be successfully mitigated.

Ideally suited for people working in any part of the finance industry as well as financial policy makers,

gives readers a vision of the future. The world of finance will fundamentally be changed over the coming decade. The book enables you to become part of the disruption – not the target of the disruption.

DeFi and the Future of Finance — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «DeFi and the Future of Finance», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

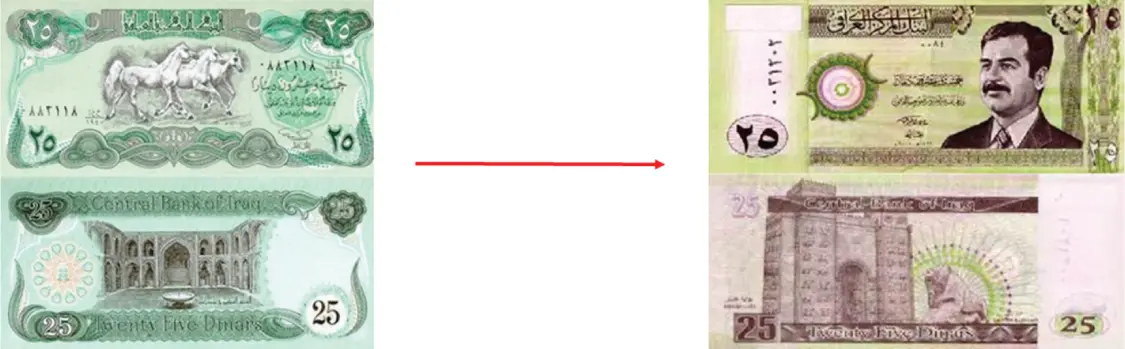

Figure 2.2Iraqi Swiss dinars and new dinars

Source: Central Bank of Iraq

The features of Bitcoin that we have mentioned – particularly scarcity and self-sovereignty – make it a potential store of value and possible hedge to political and economic unrest at the hands of global governments. As the network grows, the value proposition only increases due to increased trust and liquidity. Although Bitcoin was originally intended as a peer-to-peer currency, its deflationary characteristics and flat fees discourage its use in small transactions. We argue that Bitcoin is the flagship of a new asset class, namely, cryptocurrencies, which can have varied use cases based on the construction of their networks. Bitcoin itself, we believe, will continue to grow as an important store of value and a potential inflation hedge over long horizons. 11

The original cryptocurrencies offered an alternative to a financial system that had been dominated by governments and centralized institutions such as central banks. They arose largely from a desire to replace inefficient, siloed financial systems with immutable, borderless, open-source algorithms. These new currencies can adjust their parameters such as inflation and mechanism for consensus via their underlying blockchain to create different value propositions. We will discuss blockchain and cryptocurrency in greater depth later on but for now will focus on a particular cryptocurrency with special relevance to DeFi.

ETHEREUM AND DeFi

Ethereum (ETH) is currently the second largest cryptocurrency by market cap ($260b). Vitalik Buterin introduced the idea in 2014, and Ethereum mined its first block in 2015. Ethereum is in some sense a logical extension of the applications of Bitcoin because it allows for smart contracts – which are code that lives on a blockchain, can control assets and data, and define interactions between the assets, data, and network participants. The capacity for smart contracts defines Ethereum as a smart contract platform .

Ethereum and other smart contract platforms specifically gave rise to the decentralized application, or dApp . The backend components of these applications are built with interoperable, transparent smart contracts that continue to exist if the chain they live on exists. dApps allow peers to interact directly and remove the need for a company to act as a central clearing house for app interactions. It quickly became apparent that the first killer dApps would be financial ones.

The drive toward financial dApps became the DeFi movement, which seeks to build and combine open-source financial building blocks into sophisticated products with minimized friction and maximized value to users. Because it costs no more at an organization level to provide services to a customer with $100 or $100 million in assets, DeFi proponents believe that all meaningful financial infrastructure will be replaced by smart contracts, which can provide more value to a larger group of users. Anyone can simply pay the flat fee to use the contract and benefit from the innovations of DeFi. We will discuss smart contract platforms and dApps in more depth in Chapter 3.

DeFi is fundamentally a competitive marketplace of financial dApps that function as various financial “primitives” such as exchange, lend, and tokenize. They benefit from the network effects of combining and recombining DeFi products and attracting increasingly more market share from the traditional financial ecosystem. Our goal in this book is to give an overview of the problems that DeFi solves, describe the current and rapidly growing DeFi landscape, and present a vision of the future opportunities that DeFi unlocks.

NOTES

1 1.Alan White, “David Graeber's Debt: The First 5000 Years,” Credit Slips: A Discussion on Credit, Finance, and Bankruptcy, June 18, 2020, https://www.creditslips.org/creditslips/2020/06/david-graebers-debt-the-first-5000-years.html.

2 2.Ibid. See also Euromoney. 2001. “Forex Goes into Future Shock.” (October), https://faculty.fuqua.duke.edu/~charvey/Media/2001/EuromoneyOct01.pdf.

3 3.PayPal, founded as Confinity in 1998, did not begin offering a payments function until it merged with X.comin 2000.

4 4.Other examples include Cash App, Braintree, Venmo, and Robinhood.

5 5.C. R. Harvey, “The History of Digital Money,” 2020, https://faculty.fuqua.duke.edu/~charvey/Teaching/697_2020/Public_Presentations_697/History_of_Digital_Money_2020_697.pdf.

6 6.Satoshi Nakamoto, “Bitcoin: A Peer-to-Peer Electronic Cash System,” 2008, https://bitcoin.org/bitcoin.pdf.

7 7.Stuart Haber and W. Scott Stornetta, “How to Time-Stamp a Digital Document,” Journal of Cryptology, 3, no. 2 (1991), https://dl.acm.org/doi/10.1007/BF00196791.

8 8.Adam Back, “Hashcash – A Denial of Service Counter-Measure,” August 1, 2002, http://www.hashcash.org/papers/hashcash.pdf.

9 9.Paul Jones and Lorenzo Giorgianni, “Market Outlook: Macro Perspective,” Jameson Lopp, n.d., https://www.lopp.net/pdf/BVI-Macro-Outlook.pdf.

10 10.C. Erb and C. R. Harvey, “The Golden Dilemma,” Financial Analysts Journal, 69, no. 4 (2013): 10–42, shows that gold is an unreliable inflation hedge over short- and medium-term horizons.

11 11.Similar to gold, Bitcoin is likely too volatile to be a reliable inflation hedge over short horizons. While theoretically decoupled from any country's money supply or economy, in the brief history of Bitcoin we have not experienced any inflation surge. Therefore, there is no empirical evidence of its efficacy.

III DeFi INFRASTRUCTURE

In this chapter, we discuss the innovations that led to DeFi and lay out the terminology.

BLOCKCHAIN

The key to all DeFi is the decentralizing backbone: a blockchain. Fundamentally, blockchains are software protocols that allow multiple parties to operate under shared assumptions and data without trusting each other. These data can be anything, such as location and destination information of items in a supply chain or account balances of a token. Updates are packaged into “blocks” and are “chained” together cryptographically to allow an audit of the prior history – hence the name.

Blockchains are possible because of consensus protocols – sets of rules that determine what kinds of blocks can become part of the chain and thus the “truth.” These consensus protocols are designed to resist malicious tampering up to a certain security bound. The blockchains we focus on currently use the proof of work (PoW) consensus protocol, which relies on a computationally and energy intensive lottery to determine which block to add. The participants agree that the longest chain of blocks is the truth. If attackers want to make a longer chain that contains malicious transactions, they must outpace all the computational work of the entire rest of the network. In theory, they would need most of the network power (“hash rate”) to accomplish this – hence, the famous 51 percent attack being the boundary of PoW security. Luckily, it is extraordinarily difficult for any actor, even an entire country, to amass this much network power on the most widely used blockchains, such as Bitcoin or Ethereum. Even if most of the network power can be temporarily acquired, the amount of block history that can be overwritten is constrained by how long this majority can be maintained.

As long as no malicious party can acquire majority control of the network computational power, the transactions will be processed by the good faith actors and appended to the ledger when a block is “won.”

Читать дальшеИнтервал:

Закладка:

Похожие книги на «DeFi and the Future of Finance»

Представляем Вашему вниманию похожие книги на «DeFi and the Future of Finance» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «DeFi and the Future of Finance» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.