Campbell R. Harvey - DeFi and the Future of Finance

Здесь есть возможность читать онлайн «Campbell R. Harvey - DeFi and the Future of Finance» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:DeFi and the Future of Finance

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

DeFi and the Future of Finance: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «DeFi and the Future of Finance»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

In

, Campbell R. Harvey, Ashwin Ramachandran and Joey Santoro, introduce the new world of Decentralized Finance. The book argues that the current financial landscape is ripe for disruption and we are seeing, in real time, the reinvention of finance.

The authors provide the reader with a clear assessment of the problems with the current financial system and how DeFi solves many of these problems. The essence of DeFi is that we interact with peers—there is no brick and mortar and all of the associated costs. Savings and lending are reinvented. Trading takes place with algorithms far removed from traditional brokerages.

The book conducts a deep dive on some of the most innovative protocols such as Uniswap and Compound. Many of the companies featured in the book you might not have heard of—however, you will in the future.

As with any new technology, there are a myriad of risks and the authors carefully catalogue these risks and assess which ones can be successfully mitigated.

Ideally suited for people working in any part of the finance industry as well as financial policy makers,

gives readers a vision of the future. The world of finance will fundamentally be changed over the coming decade. The book enables you to become part of the disruption – not the target of the disruption.

DeFi and the Future of Finance — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «DeFi and the Future of Finance», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

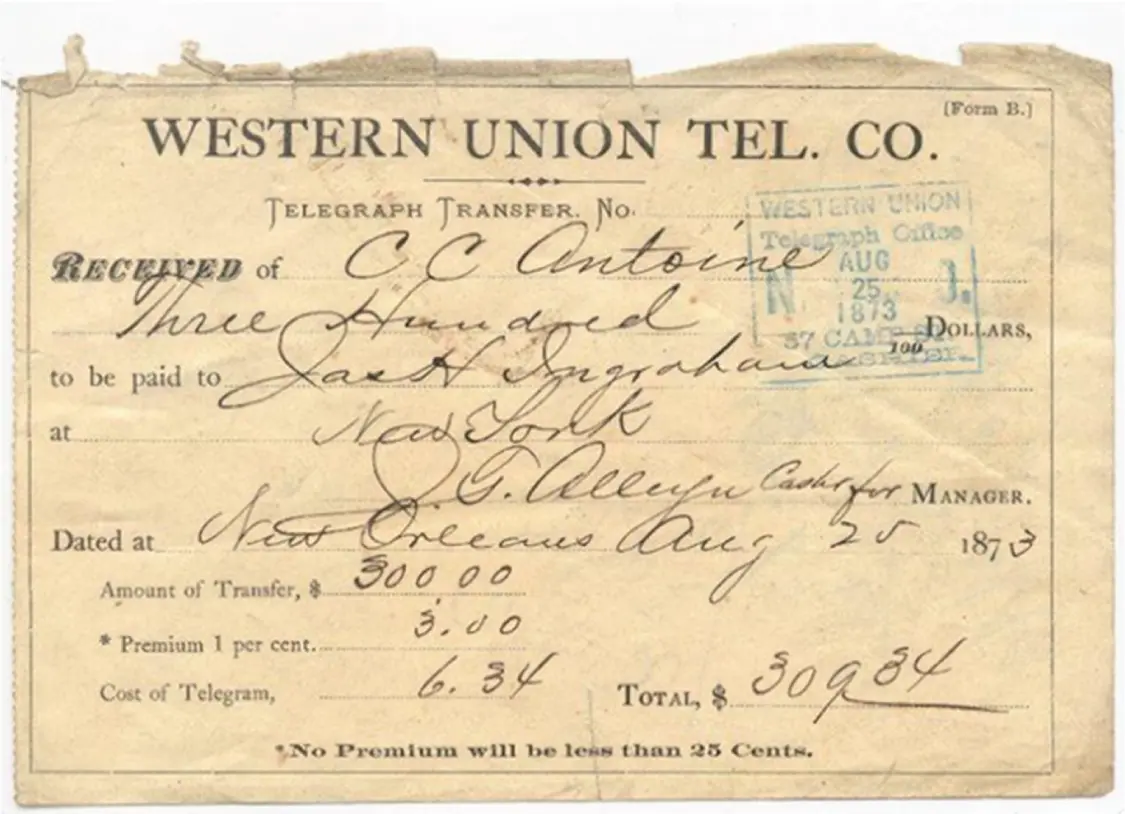

Figure 2.1Western Union transfer from 1873

Source: Western Union Holdings, Inc.

The last 75 years has seen many firsts in the financial world: credit card in 1950 (Diners Club); automated teller machine (ATM) in 1967 (Barclays Bank); telephone banking in 1983 (Bank of Scotland); Internet banking in 1994 (Stanford Federal Credit Union); radio-frequency identification (RFID) payments in 1997 (Mobil Speedpass); chip-and-pin credit cards in 2005 (Mastercard); and Apple Pay with a mobile device in 2014 (Apple).

Importantly, all these innovations were built on the backbone of centralized finance. While there have been some technological advances, the structure of today’s banking system has not changed much in the past 150 years. That is, digitization still supported a legacy structure. The high costs associated with this legacy system has spurred further advances known as fintech .

FINTECH

When costs are high, innovation will arise to capitalize on inefficiencies. Sometimes, however, a powerful layer of middle people can slow this process. An early example of decentralized finance emerged in the foreign currency (forex) market 20 years ago. At the time, large corporations used their investment banks to manage their forex needs. For example, a U.S.-based corporation might need €50 million at the end of September to make a payment on some goods purchased in Germany. Its bank would quote a rate for the transaction. At the same time, another client of the bank might need to sell €50 million at the end of September. The bank would quote a different rate. The difference in the rate is known as the spread – the profit the bank makes for being the intermediary. Given the multitrillion-dollar forex market, this was an important part of bank profits.

In early 2001, a fintech startup offered the following idea. 2 Instead of individual corporations querying various banks to get the best rate, why not have an electronic system match the buyers and sellers directly at an agreed upon price and no spread? Indeed, the bank could offer this service to its own customers and collect a modest fee (compared with the spread). Furthermore, given that some customers deal with multiple banks, it would be possible to connect customers at all banks participating in the peer-to-peer network.

You can imagine the reception. The bank might say: “Are you telling me we should invest in an electronic system that will cannibalize our business and largely eliminate a very important profit center?” However, even 20 years ago, banks realized that their largest customers were very unhappy with the current system. As globalization surged, these customers faced unnecessary forex transactions costs.

An even earlier example was the rise of dark pool stock trading. In 1979, the U.S. Securities and Exchange Commission (SEC) instituted Rule 19c3, which allowed stocks listed on one exchange, such as the New York Stock Exchange (NYSE), to be traded off-exchange. Many large institutions moved their trading large blocks to these dark pools, where they traded peer to peer with far lower costs than traditional exchange-based trading.

The excessive costs of transacting has ushered in many fintech innovations. PayPal, 3 founded more than 20 years ago, is a forerunner in the payments space; in 2017, seven of the largest U.S. banks added their own payment system called Zelle. 4 An important commonality of these cost-reducing fintech advances is that they rely on the centralized backbone of the current financial infrastructure.

BITCOIN AND CRYPTOCURRENCY

The dozens of digital currency initiatives beginning in the early 1980s all failed. 5 The landscape shifted, however, with the publication of the famous Satoshi Nakamoto Bitcoin white paper 6 in 2008, which presents a peer-to-peer system that is decentralized and uses the concept of blockchain . Invented in 1991 by Haber and Stornetta, 7 blockchain was initially primarily envisioned to be a time-stamping system to keep track of different versions of a document. The key innovation of Bitcoin was to combine the idea of blockchain (time stamping) with a consensus mechanism called proof of work (introduced by Back 8 in 2002). The technology produced an immutable ledger that eliminated a key problem with any digital asset: you can make perfect copies and spend them multiple times. Blockchains allow for the important features desirable in a store of value, which were never before simultaneously present in a single asset. Blockchains allow for cryptographic scarcity (Bitcoin has a fixed supply cap of 21 million), censorship resistance and user sovereignty (no entity other than the user can determine how to use funds), and portability (can send any quantity anywhere for a low flat fee). These features combined in a single technology make cryptocurrency a powerful innovation.

The value proposition of Bitcoin is important and can be best understood juxtaposed with that of other financial assets. For example, consider the U.S. dollar (USD). It used to be backed by gold before the gold standard was abandoned in 1971. Now, the demand for USD comes from (a) taxes, (b) purchase of U.S. goods denominated in USD, and (c) repayment of debt denominated by USD. These three cases create value that is not intrinsic but rather is based on the network that is the U.S. economy. Expansion or contraction in these components can impact the price of the USD. Additionally, shocks to the supply of USD adjust its price at a given level of demand. The Fed can adjust the supply of USD through monetary policy in an attempt to achieve financial or political goals. Inflation eats away at the value of USD, decreasing its ability to store value over time. One might be concerned with runaway inflation – what Paul Tudor Jones calls the great monetary inflation – which would lead to a flight to inflation-resistant assets. 9 Gold has proven to be a successful inflation hedge due to its practically limited supply, concrete utility, and general global trustworthiness. However, given that gold is a volatile asset, its historical hedging ability is realized only at extremely long horizons. 10

Many argue that Bitcoin has no “tangible” value and therefore should be worthless. Continuing the gold comparison, approximately two-thirds of gold is used for jewelry, and an additional amount is used in technology hardware. Gold has tangible value. The U.S. dollar, while a fiat currency, has value as “legal tender.” However, there are many examples from history whereby currency emerged without any backing that had value.

A relatively recent example is the Iraqi Swiss dinar. This was the currency of Iraq until the first Gulf War in 1990. The printing plates were manufactured in Switzerland (hence the name), and the printing was outsourced to the United Kingdom. In 1991, Iraq was divided, with the Kurds controlling the north and Saddam Hussein the south. Due to sanctions, Iraq could not import dinars from the UK and had to start local production. In May 1993, the Central Bank of Iraq announced that citizens had three weeks to exchange old 25 dinars for new ones ( Figure 2.2). Afterwards, the old dinar would be unredeemable.

The old Iraqi Swiss dinar, however, continued to be used in the north. In the south, the new dinar suffered from extreme inflation. Eventually, the exchange rate was 300 new dinars for a single Iraqi Swiss dinar. The key insight here is that the Iraqi Swiss dinar had no official backing – but it was accepted as money. There was no tangible value, yet it had value. Importantly, value can be derived from both tangible and intangible sources.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «DeFi and the Future of Finance»

Представляем Вашему вниманию похожие книги на «DeFi and the Future of Finance» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «DeFi and the Future of Finance» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.