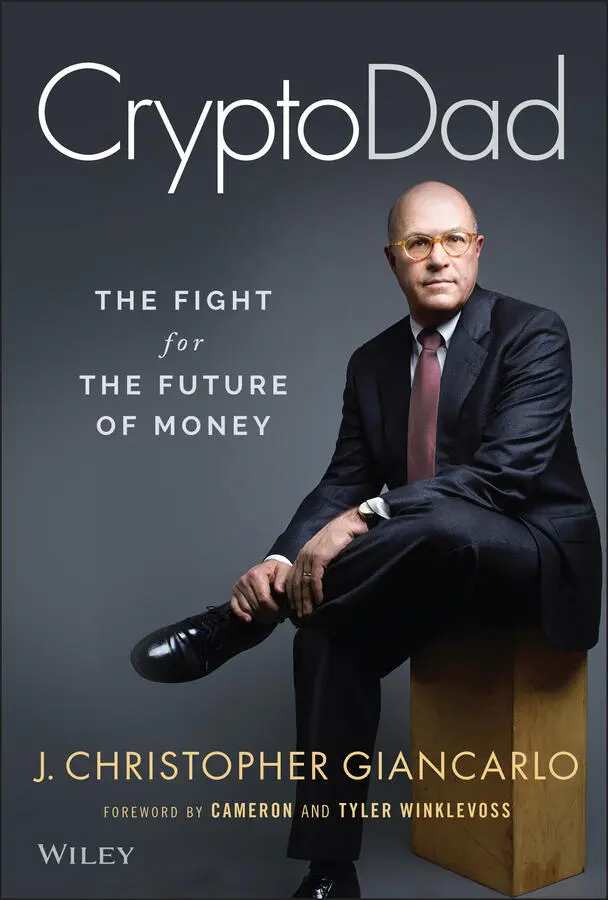

J. Christopher Giancarlo - CryptoDad

Здесь есть возможность читать онлайн «J. Christopher Giancarlo - CryptoDad» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:CryptoDad

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:4 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

CryptoDad: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «CryptoDad»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

describes Giancarlo’s own reckoning with the future of the global economy—at the intersection of markets, technology, and public policy—and lays out the fight for a Digital Dollar.

CryptoDad CryptoDad A thorough exploration of digital change and how it affects the lives of everyone in a global economy A revolutionary consideration of regulatory responses to the rapid pace of technological innovation A call to update our aging financial organizations, particularly the infrastructure of money itself, and focus on renewed faith and confidence in free market innovation A foreword by Cameron and Tyler Winklevoss, two of the biggest names in cryptocurrencies

argues that the next digital wave will be the coming Internet of Value, where cryptocurrencies will do the Internet of Information did to immaterial things: make them accessible, distributable, and movable instantly across the globe. This book is an ideal introduction to the importance of technology in the marketplace.

CryptoDad — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «CryptoDad», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

This decision was an essential step in allowing swaps trading some of the flexibility that Dodd–Frank authorized.

Action by No Action

A greater breakthrough came the following January 2016, almost a year after the white paper's publication. It was my first day back in Washington after Christmas break at our home in New Jersey. In the office, I met with my staff to hear their analysis of the agency's proposed individual permanent registrations for the first 18 Swap Execution Facilities. We went through each application. My staff counsel, Amir Zaidi, a rigorous lawyer and former analyst at the Federal Reserve Bank of New York, identified the different business models offered by each firm.

It quickly became apparent that the applications reflected a comprehensive range of business models. These included hybrid electronic and voice-based systems, mechanisms called “request for quote” and “central limit order books,” as well as fully electronic auction systems. Some of the applicants sought to serve primarily wholesale—or “sell side”—market participants, while others sought to serve both “sell-side” and “buy-side” players. Some of the SEFs focused on just a few types of swaps, while others planned to handle a wide range. It was clear that the staff had bent over backwards to allow SEFs to operate by “any means of interstate commerce” as Congress had promised in Dodd–Frank.

Though delighted with the result, I was disappointed by the elaborate, administrative procedure that produced it. That result was a fair amount of circumvention of the ill-conceived SEF rules. Those peculiar rules, by their terms, required SEFs to restrict their business models to just two means of interstate commerce: “request for quote” and “central limit order books.” CFTC staff were now recommending, however, approval of SEF registrations that allowed a broad set of trading methods. In my view, that was exactly the right outcome, because that was what Congress had always envisioned and specified in the language of the Act. But what a ridiculous, roundabout way to do the right thing.

The guts of the workaround hinged on conditioning SEF approvals on applicants' compliance with five staff letters, called “no-action letters.” Each letter effectively waived flawed swaps trading rules that I had identified in my white paper.

This was bad administrative law on several levels. First, rather than the CFTC lifting the inappropriate limits on SEF business models, the CFTC was just ignoring those limits. Second, the opaque mechanisms being used would make it very hard for other market participants to understand what modes of swap execution the CFTC was really permitting. Observers would have to pore over the fine print of each and every SEF registration that was approved and then extrapolate the unstated rules that were quietly being applied. Third, relying on a hodgepodge of “no action” letters would force market participants to jump through pointless hoops of make-work.

I told my staff I intended to issue a blistering public statement. I would declare that the whole thing was a sham and that “the Emperor had no clothes.”

Amir's face turned down. I asked why. He told me that market participants were sorely afraid of my doing so. Everyone knew that it was a charade to pretend that SEFs were being restricted in their business models when, in fact, they were being allowed to operate competitively. But the industry also knew that Dodd-Frank advocates needed to maintain the appearance that they were “cracking down” on Wall Street. If I was candid about what the staff had done, then Dodd–Frank proponents might have to profess shock and foist more restrictions on SEFs. In short, everybody was hoping that I would keep my mouth shut. I got the point.

So what had started with a bang was ending with a whimper. The CFTC staff had folded their tent on the flawed SEF rules. My white paper had served its purpose. I could not take credit, however, for a good outcome that no one wanted to admit had taken place. We had arrived at the right outcome but through the wrong means. The right means would have been for the commission to openly acknowledge that economic freedom, never having been abridged by Congress, could not be abridged by an unelected regulatory body like the CFTC.

The situation was not satisfactory in the long term. What the staff permitted today, it might not permit tomorrow. The only right thing to do would be to change CFTC rules. I would keep my mouth shut for now. But I made up my mind to try to change the rules in the unlikely event I ever got the chance.

Position Limits

Buoyed by the success of the white paper, I returned to the fray on another contentious issue: position limits. Position limits are pre-set restrictions on the amount of futures contracts that may be held by traders. They had been put in place and managed by the exchanges and the CFTC for decades. The purpose of position limits is to prevent market participants, especially large traders, or groups of traders, from manipulating large positions to unduly affect market prices or exert control over markets.

The renewed debate on position limits began before I joined the commission and, as it would turn out, continued after my departure. Dodd–Frank required the CFTC to establish a new and broader set of position limits as necessary to prevent “the burdens associated with excessive speculation causing sudden or unreasonable fluctuations or unwarranted changes in price.” It was one of the few Dodd–Frank mandates the agency had still not successfully implemented when I arrived.

The CFTC had actually adopted a comprehensive position limits rule back in 2011 amidst a huge behind-the-scenes dogfight. But a year later a federal court struck it down, ruling that the CFTC had not, as required by the language of the Dodd–Frank Act, made a formal finding that the limits it sought to impose were necessary to prevent burdens on interstate commerce.

In December 2013, the agency put out a revised position limits proposal, expressly finding that its limits were “necessary.” But market participants—especially agriculture and energy producers—heavily criticized the proposal as overly restrictive, which it was.

Now, in 2015, the commission was getting ready to revise that 2013 proposal. I wanted to make sure we got it right.

Years before, as a practicing lawyer, I always made a point of visiting new clients at their places of business to learn what they did and how they did it. I couldn't really help a client, I felt, until I understood how the client made a living.

When I joined the CFTC, I knew better than most people in Washington how Wall Street banks used swaps and other derivatives to make a living. Still, I knew little about how American farmers, ranchers, oilmen, and manufacturers used derivatives to make their livings. Now, as a commissioner, I decided to find out. I would go visit them.

Over my five years at the CFTC, I would travel across well over half the country to meet with thousands of Americans who depended on CFTC-regulated derivatives in their livelihoods. I eventually visited 22 states that depended on CFTC regulated products to hedge the prices of agriculture, mineral, or energy that they produced. In the course of those travels, I descended 900 feet underground in a Kentucky coal mine, climbed 90 feet in the air on a North Dakota natural gas rig and went even higher in an Arkansas crop duster. I walked factory floors in Illinois, oil refineries in Texas, grain elevators in Indiana, and power plants in Ohio. I milked dairy cows with family farmers in Melrose, Minnesota. I met with grain and livestock producers in New York, Montana, Iowa, and Louisiana. In Kansas, I met Mary and Pat Ross at their feedlot in Lawrence, traveled to Ken McCauley's corn farm in White Cloud, and visited Pat O'Trimble's soybean fields in Perry. In Michigan, I toured the Ford Rouge automobile manufacturing plant, visited a grain mill in Frankenmuth, and met with farmers and agricultural product suppliers at a fertilizer depot in Henderson.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «CryptoDad»

Представляем Вашему вниманию похожие книги на «CryptoDad» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «CryptoDad» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.