Sunil K. Parameswaran - Fundamentals of Financial Instruments

Здесь есть возможность читать онлайн «Sunil K. Parameswaran - Fundamentals of Financial Instruments» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Fundamentals of Financial Instruments

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Fundamentals of Financial Instruments: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Fundamentals of Financial Instruments»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

, renowned finance trainer Sunil Parameswaran delivers a comprehensive introduction to the full range of financial products commonly offered in the financial markets. Using clear, worked examples of everything from basic equity and debt securities to complex instruments—like derivatives and mortgage-backed securities – the author outlines the structure and dynamics of the free-market system and explores the environment in which financial instruments are traded. This one-of-a-kind book also includes: New discussions on interest rate derivatives, bonds with embedded options, mutual funds, ETFs, pension plans, financial macroeconomics, orders and exchanges, and Excel functions for finance Supplementary materials to enhance the reader’s ability to apply the material contained within A foundational exploration of interest rates and the time value of money

is the ideal resource for business school students at the undergraduate and graduate levels, as well as anyone studying financial management or the financial markets. It also belongs on the bookshelves of executive education students and finance professionals seeking a refresher on the fundamentals of their industry.

Fundamentals of Financial Instruments — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Fundamentals of Financial Instruments», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

When a person is given a right to transact in the underlying asset, the right can obviously take on one of two forms. That is, that person may either have the right to buy the underlying asset, or the right to sell the underlying asset. Options contracts that give the holder the right to acquire the underlying asset are known as Call options. If the buyer of such an option were to exercise that right, the seller of the option is obliged to deliver the underlying asset as per the terms of the contract. Peter, in the previous example, obviously possesses a call option.

There exist options contracts that give the holder the right to sell the underlying asset. These are known as Put options. In the case of such contracts, if the holder were to decide to exercise his option, the seller of the put is obliged to take delivery of the underlying asset.

Options give the holder the right to buy or sell the underlying asset. If the contract were to permit exercise only at the time of expiration, the option, whether a call or a put, is known as a European option. If such an option were not to be exercised at the time of expiration, then the contract itself would expire. There exists another type of contract, where the holder has the right to transact at any point between the time of acquisition of the right and the expiration date of the contract. These are referred to as American options. Quite obviously, the expiration date is the only point in time at which a European option can be exercised, and the last point in time at which an American option can be exercised.

An options contract, whether a call or a put, requires the buyer to pay a price to the seller at the outset, for giving the right to transact. This price is known as the option price or option premium. This price is nonrefundable if the contract were not to be exercised subsequently. If and when an options contract is exercised, the buyer will have to pay a price per unit of the underlying asset if exercising a call option, and will have to receive a price per unit of the underlying asset if exercising a put option. This price is known as the exercise price or the strike price . The difference between the two prices is that while the option premium has to be paid at the very outset, the exercise price enters the picture only if the option is exercised subsequently. Thus, the exercise price may or may not be paid/received eventually. Futures contracts are termed as commitment contracts , for they represent a binding commitment for both parties. Options, on the other hand, are termed as contingent contracts for they will be exercised by the holder only in the event of it being profitable. In the case of calls, this will be contingent on the asset price being greater than the exercise price, whereas in the case of puts, it will be contingent on the asset price being lower than the exercise price.

Futures and forward contracts, however, do not require either party to make a payment at the outset, because they impose an equivalent obligation on both the buyer and the seller. The futures price, which is the price at which the buyer will acquire the asset on a future date, will be set in such a way that the value of the futures contract at inception is zero, from the standpoint of both the buyer as well as the seller.

SWAPS

A swap is a contractual agreement between two parties to exchange cash flows calculated on the basis of prespecified terms at predefined points in time.

The cash flows being exchanged represent interest payments on a specified principal amount, which are computed using two different yardsticks. For instance, one interest payment may be computed using a fixed rate of interest, while the other may be based on a variable benchmark such as the T-bill rate.

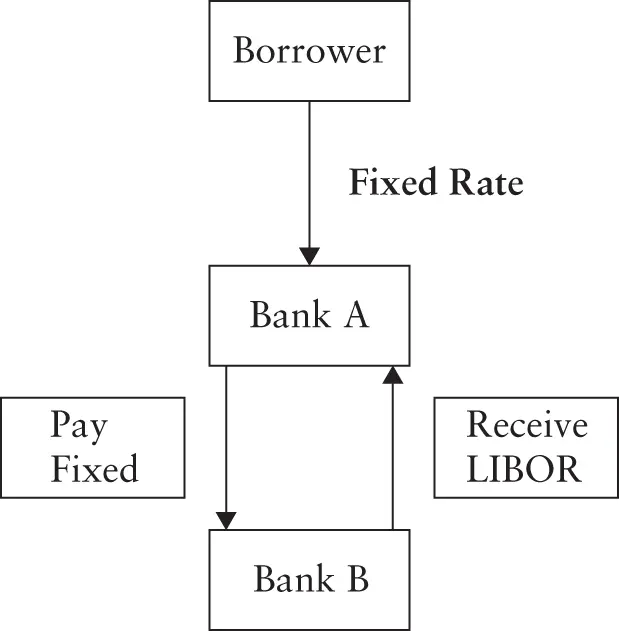

A swap where both payments are denominated in the same currency is referred to as an Interest Rate Swap. The motivation for such a transaction may be understood as follows. Consider the case of a commercial bank that has entered into a fixed rate loan with one of its clients. It may now be of the opinion that interest rates are going to rise. Renegotiation of the loan may not be feasible. Even if it were, it would involve substantial legal and administrative efforts. It would be much easier for the bank concerned to enter into a swap transaction with an institution, perhaps another commercial bank, wherein it pays a fixed rate of interest and receives a variable rate based on a benchmark such as LIBOR. By doing so it would have converted its fixed rate income stream to a floating rate income stream and would stand to benefit if interest rates rise as anticipated. Thus, in a nutshell, the objective of a swap is to enable a party to dispose of a cash flow stream in exchange for another cash flow stream. Diagrammatically we can depict the above transaction as follows ( Figure 1.1).

FIGURE 1.1

There also exist swaps where two parties exchange cash flows denominated in two different currencies. Such swaps are referred to as Currency Swaps.

MORTGAGES AND MORTGAGE-BACKED SECURITIES

A mortgage is a loan that is backed by the collateral of specified real estate property. The borrower of funds, the mortgagor, is obliged to make periodic payments to the lender, the mortgagee, to retire the debt. In the event of the mortgagor defaulting, the lender can foreclose the mortgage, which means that the lender can take over the property to recover the balance due.

A mortgage by itself is an illiquid asset for the party that makes the loan to the home buyer. Such lenders are called originators. To rotate their capital, lenders will typically pool mortgage loans and issue debt securities backed by the underlying pool. Such securities, the cash flows for which arise from the payments made by borrowers of the underlying loans, are referred to as mortgage-backed securities. The process of converting an illiquid asset such as a home loan into liquid marketable securities is referred to as securitization . The process of securitization, although it is common in the case of mortgage lending, is not restricted to such loans. In practice, receivables from automobile loans and credit card receivables are also securitized. The securities generated in the process are referred to as asset-backed securities.

HYBRID SECURITIES

A hybrid security combines the features of more than one type of basic security. We will discuss two such assets, namely convertible bonds and warrants.

A convertible bond is a debt security that permits the investor to convert the bond into shares of equity at a predetermined rate. Until and unless the investor converts the bond, it will continue to trade in the form of a standard debt security. The interest rate on such bonds will be lower than the rate on securities without the option to convert because the conversion feature will be perceived as a sweetener by potential investors. The rate of conversion from debt into equity will typically be set in such a way that the conversion price is higher than the market price prevailing at the time of issue of the debt. For instance, a bond with a principal value of $1,000 may be convertible to 25 shares of equity. In this case the conversion price is $40, and the share price prevailing at the time of issue of the convertible will be less than $40.

A warrant is a right given to investors which allows them to subscribe to the equity shares of the company at a future date at a predetermined price. Such rights are usually offered along with debt securities to make the bonds more attractive to investors. Once issued, the warrants can be detached from the parent security, and can be traded in the secondary market.

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Fundamentals of Financial Instruments»

Представляем Вашему вниманию похожие книги на «Fundamentals of Financial Instruments» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Fundamentals of Financial Instruments» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.