Karen Phelan - I'm Sorry I broke Your Company

Здесь есть возможность читать онлайн «Karen Phelan - I'm Sorry I broke Your Company» весь текст электронной книги совершенно бесплатно (целиком полную версию без сокращений). В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Город: San Francisco, Год выпуска: 2013, ISBN: 2013, Издательство: Berrett-Koehler Publishers, Жанр: management, popular_business, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:I'm Sorry I broke Your Company

- Автор:

- Издательство:Berrett-Koehler Publishers

- Жанр:

- Год:2013

- Город:San Francisco

- ISBN:978-1-60994-740-8; 978-1-60994-741-5

- Рейтинг книги:3 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

I'm Sorry I broke Your Company: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «I'm Sorry I broke Your Company»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

I'm Sorry I broke Your Company — читать онлайн бесплатно полную книгу (весь текст) целиком

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «I'm Sorry I broke Your Company», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

The idea behind all this analysis and documentation and charting is that this discipline will uncover the roots of your business problems. However, the best things about human-based problems are that we are self-aware and we can communicate. We can tell you what's wrong, but you do have to ask. In my experience, for the majority of business problems, at least one person knows exactly what is causing it. If not, partial knowledge of the cause resides in multiple heads, and you need to bring them together to get the full problem. These root cause and problem-solving tools are effective when you bring people together who normally don’t have a chance to communicate with each other. The tools by themselves are pretty useless. Using a tool or a methodology or a piece of software as an excuse to hold a meeting or kick off a cross-functional team is an effective problem-solving method. People like to use tools. That's how we evolved into a civilization. The caution is thinking that the tool holds the solution and can be effective without bringing the people together, and unfortunately, that's how many of these methodologies evolve. They start out as people-based techniques, and then someone decides to eliminate the messy human variable. The next thing you know, you have a data- and documentation-heavy methodology that requires an inordinate amount of time for consulting analysts to complete, and if they are lucky, their analyses will stumble upon the right answer. But all that effort could have been used to just ask the people involved and to work on the problem together in a creative and collaborative way. Yet we don't have time to work on process problems together because we are too busy inputting data, documenting flowcharts, installing software, analyzing data, and creating reports to do any meaningful improvement work.

Documents, reports, and plans are not the real deliverables. As with strategic plans, the value is in the thinking, learning, and creating and not in the resulting paperwork. The document will be obsolete before you print it anyway. Any tool, method, program, or initiative that promises to solve your business problems without including everyone involved in your business problem will fail. Whether it is a software program or change initiative, the only way to improve your operations is to get all your people together to work on them. Then it doesn't really matter what tool or methodology you choose. Your people are both the problem and the solution.

3. Metrics Are the Means, Not the Ends

Numerical Targets Are Measure-mental

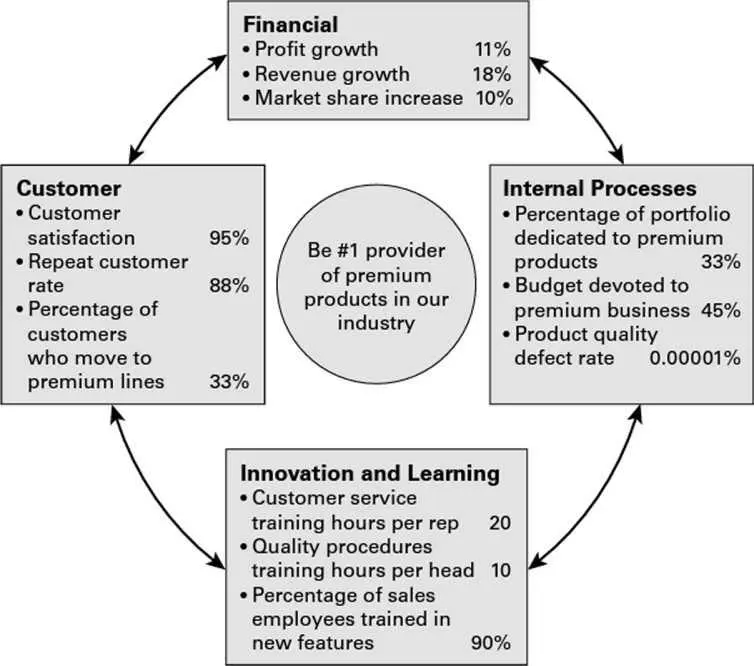

Because of the obsession with financial measures that arose in the 1980s, someone was bound to note that it takes more than just managing the financials to run a business. Those someones were Robert Kaplan and David Norton, who published a paper on the balanced scorecard (BSC) in the Harvard Business Review (HBR) in 1992. The premise of the BSC is that four categories of measures are needed to manage a business successfully — financial, customer satisfaction, internal processes, and innovation and learning. Ideally, the measures in these four categories would be determined by the business’s strategic goals, and the scorecard could be used to operationalize a strategic plan. The BSC would include both internal and external objectives for implementing the strategy with numerical targets that would let you know your progress. See figure 2 for an example.

This BSC aligns an organization around creating premium products with the purpose of improving profits, revenues, and market share with those as the designated financial measures with end-of-year targets. The other categories help operationalize the strategy: process goals include the number of premium products in development, percentage of budget devoted to premium products, and defect rate; customer goals include satisfaction rate, retention, and percentage who purchase the premium lines; and learning goals include customer service training hours and R&D training budget. (There are no innovation goals in this example.) All these measures contribute to achieving the premium provider market leader status as the strategy.

Figure 2 Balanced scorecard

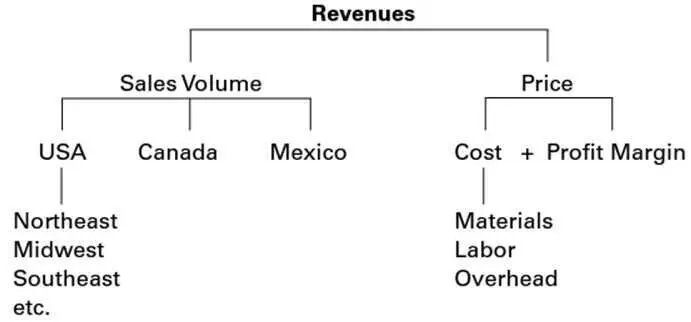

However, if the BSC was going to help implement a new strategy, it didn't go far enough. High-level objectives are fine for the C suite, but how do the workers contribute to market share or training budget goals? The next logical step was called «key performance indicators» (KPIs). Each of the balanced scorecard measures could be broken down into It's component measures— for instance, revenue consists of sales volume and price. Each of those measures could be further broken down and then the resulting measures also broken down. For example, total sales is broken down into country sales and then into regional sales; price is broken down into unit cost and profit margin (see figure 3). This process of breaking down metrics into a hierarchy of component measures was sometimes called «cascading» key performance indicators. This way, every level in the organization could contribute to implementing the strategy and achieving the strategic objectives. As a machine operator or customer service representative, I could see how my role contributed to the overall objectives through the use of this hierarchy of submetrics.

Figure 3 Cascading key performance indicators

We consultants took to this measurement system like remoras to a shark. The problem with most consulting at the time was that the firms did the analysis, developed the strategy or new process, created a recommended implementation plan, and then left for another client. Executing the strategy was left to the client. The process work helped but often didn't cover all the strategic objectives, and it was up to the clients management team to enforce both the new processes and the new strategic plan. One doesn't make much money in consulting by trusting managers to do their jobs well. If they did, they wouldn't need us. Now we had tools to monitor the implementation and results of our efforts.

With the balanced scorecard, we could break the strategy down into strategic objectives in the four areas and add targets. Combined with new work processes, this system of measures was a surefire method of implementing the strategy. In this way, how each person in the organization contributed to the strategic objectives could be monitored and measured. It provided discipline to the messy business of organizational change. This structure was wonderfully appealing to both consultants and clients alike. The result would be an entire company aligned around specific goals and targets, with everyone able to measure how well she is doing her part — a complete command-and-control system for implementing strategic objectives. Even better, consultants could sell the balanced scorecard and cascading key performance indicators as a stand-alone service.

Pretty much every consulting project I’ve been involved with over the last two decades has had some metrics component. The use of metrics for any kind of project is so widespread that people rarely ever question the value of collecting and monitoring measurements. It's a given that you need a system of measures to accomplish anything. The following two points are from a PowerPoint presentation I have often used in client engagements that seem to be a mainstay in pretty much every consultant's repertoire:

You can't manage what you can't measure!

Читать дальшеИнтервал:

Закладка:

Похожие книги на «I'm Sorry I broke Your Company»

Представляем Вашему вниманию похожие книги на «I'm Sorry I broke Your Company» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «I'm Sorry I broke Your Company» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.