Eric Tyson - Home Buying Kit For Dummies

Здесь есть возможность читать онлайн «Eric Tyson - Home Buying Kit For Dummies» — ознакомительный отрывок электронной книги совершенно бесплатно, а после прочтения отрывка купить полную версию. В некоторых случаях можно слушать аудио, скачать через торрент в формате fb2 и присутствует краткое содержание. Жанр: unrecognised, на английском языке. Описание произведения, (предисловие) а так же отзывы посетителей доступны на портале библиотеки ЛибКат.

- Название:Home Buying Kit For Dummies

- Автор:

- Жанр:

- Год:неизвестен

- ISBN:нет данных

- Рейтинг книги:5 / 5. Голосов: 1

-

Избранное:Добавить в избранное

- Отзывы:

-

Ваша оценка:

Home Buying Kit For Dummies: краткое содержание, описание и аннотация

Предлагаем к чтению аннотацию, описание, краткое содержание или предисловие (зависит от того, что написал сам автор книги «Home Buying Kit For Dummies»). Если вы не нашли необходимую информацию о книге — напишите в комментариях, мы постараемся отыскать её.

When it comes to buying a home, it's hard to know where to begin. You want to buy at a fair price at the right time—not always easy in a fast-changing market. The updated

has all you need: strategies to secure the optimal deal, the ins and outs of home financing, how to evaluate rent vs. buy, and the latest on regulations around mortgage interest and property tax. Whether a first-time buyer or veteran homeowner, this book will help you make the smart decisions that move you into your dream home in no time!

Get your finances in order Improve your credit score Choose the right mortgage Build your real estate team Maximize your financial health Inspect and protect your home Understand and minimize closing costs

Home Buying Kit For Dummies — читать онлайн ознакомительный отрывок

Ниже представлен текст книги, разбитый по страницам. Система сохранения места последней прочитанной страницы, позволяет с удобством читать онлайн бесплатно книгу «Home Buying Kit For Dummies», без необходимости каждый раз заново искать на чём Вы остановились. Поставьте закладку, и сможете в любой момент перейти на страницу, на которой закончили чтение.

Интервал:

Закладка:

Unfortunately, Peter bought a place that stretched his budget and required lots of attention and maintenance. Adding insult to injury, Peter went to graduate school clear across the country (something he knew he was likely to do at the time he bought) three years after he purchased. During these three years of his ownership, home prices dropped 10 percent in Peter’s neighborhood. So after paying the expenses of sale and closing costs, Peter ended up losing his entire down payment when he sold.

Conversely, some people who continue to rent should buy. In her late 20s, Melody didn’t want to buy a home, because she didn’t like the idea of settling down. Her monthly rent seemed so cheap compared with the sticker prices on homes for sale.

As it always does, time passed. Melody’s 20s turned into 30s, which melted into 40s and then 50s, and she was still renting. Her rent skyrocketed to eight times what it was when she first started renting. She fearfully looked ahead to escalating rental rates in the decades when she hoped to be retired.

Ownership advantages

Most people should eventually buy homes, but not everyone and not at every point in their lives. To decide whether now’s the time for you to buy, consider the advantages of buying and whether they apply to you.

Owning should be less expensive than renting

You probably didn’t appreciate it growing up, but in addition to the diaper changes, patience during potty training, help with homework, bandaging of bruised knees, and countless meals, your folks made sure that you had a roof over your head. Most of us take shelter for granted, unless we don’t have it or are confronted for the first time with paying for it ourselves.

Remember your first apartment when you graduated from college or when your folks finally booted you out? That place probably made you appreciate the good deal you had before — even those cramped college dormitories may have seemed more attractive!

But even if you pay several hundred to a thousand dollars or more per month in rent, that expense may not seem so steep if you happen to peek at a home for sale. In most parts of the United States, we’re talking about a big number — $150,000, $225,000, $350,000, or more for the sticker price. (Of course, if you’re a higher-income earner, you may think that you can’t find a habitable place to live for less than a half-million dollars, especially if you live in costly places such as New York City, Boston, Chicago, Los Angeles, or San Francisco.)

Here’s a guideline that may change the way you view your seemingly cheap monthly rent. To figure out the price of a home you can buy for approximately the same monthly cost as your current rent, simply do the following calculation:

Here’s a guideline that may change the way you view your seemingly cheap monthly rent. To figure out the price of a home you can buy for approximately the same monthly cost as your current rent, simply do the following calculation:

Take your monthly rent and multiply by 200, and you come up with the purchase price of a home.

$ _________ per month × 200 = $ _________

Example: $ 1,000 × 200 = $200,000

So, in the preceding example, if you were paying rent of $1,000 per month, you would pay approximately the same amount per month to own a $200,000 home (factoring in modest tax savings). Now your monthly rent doesn’t sound quite so cheap compared with the cost of buying a home, does it? (Note that in Chapter 3we show you how to accurately calculate the total costs of owning a home.)

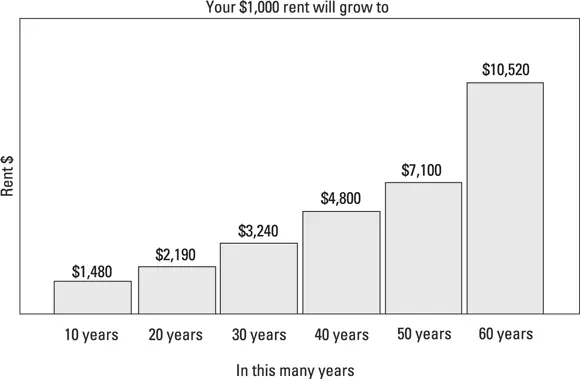

Even more important than the cost today of buying versus renting is the cost in the future. As a renter, your rent is fully exposed to increases in the cost of living, also known as inflation. A reasonable expectation for annual increases in your rent is 4 percent per year. Figure 1-1 shows what happens to a $1,000 monthly rent at just 4 percent annual rental inflation.

Even more important than the cost today of buying versus renting is the cost in the future. As a renter, your rent is fully exposed to increases in the cost of living, also known as inflation. A reasonable expectation for annual increases in your rent is 4 percent per year. Figure 1-1 shows what happens to a $1,000 monthly rent at just 4 percent annual rental inflation.

© John Wiley & Sons, Inc.

FIGURE 1-1:The skyrocketing cost of renting.

When you’re in your 20s or 30s, you may not be thinking or caring about your golden years, but look what happens to your rent over the decades ahead with just modest inflation! Then remember that paying $1,000 rent per month now is the equivalent of buying a home for $200,000. Well, in 40 years, with 4 percent inflation per year, your $1,000-per-month rent will balloon to $4,800 per month. That’s like buying a house for $960,000!

In our example, we picked $1,000 for rent to show you what happens to that rent with a modest 4 percent annual rate of inflation. To see what may happen to your current rent at that rate of inflation (as well as at a slightly higher one), simply complete Table 1-1. (You can also access Table 1-1online at

In our example, we picked $1,000 for rent to show you what happens to that rent with a modest 4 percent annual rate of inflation. To see what may happen to your current rent at that rate of inflation (as well as at a slightly higher one), simply complete Table 1-1. (You can also access Table 1-1online at www.dummies.com/go/homebuyingkit7e .)

If you’re middle-aged or retired, you may not plan on having 40 to 60 years ahead of you. On the other hand, don’t underestimate how many more years of housing you’ll need. U.S. health statistics indicate that at age 50, you have a life expectancy of 30+ more years, and at age 65, 20+ more years (women on average tend to live a few years longer).

If you’re middle-aged or retired, you may not plan on having 40 to 60 years ahead of you. On the other hand, don’t underestimate how many more years of housing you’ll need. U.S. health statistics indicate that at age 50, you have a life expectancy of 30+ more years, and at age 65, 20+ more years (women on average tend to live a few years longer).

TABLE 1-1Figuring Future Rent

| Your Current Monthly Rent | Multiplication Factor to Determine Rent in Future Years at 4 Percent Annual Inflation Rate | Projected Future Rent |

| $__________ | × 1.48 | = $___________ in 10 years |

| $__________ | × 2.19 | = $___________ in 20 years |

| $__________ | × 3.24 | = $___________ in 30 years |

| $__________ | × 4.80 | = $___________ in 40 years |

| $__________ | × 7.11 | = $___________ in 50 years |

| $__________ | × 10.52 | = $___________ in 60 years |

| Your Current Monthly Rent | Multiplication Factor to Determine Rent in Future Years at 6 Percent Annual Inflation Rate | Projected Future Rent |

| $__________ | × 1.79 | = $___________ in 10 years |

| $__________ | × 3.21 | = $___________ in 20 years |

| $__________ | × 5.74 | = $___________ in 30 years |

| $__________ | × 10.29 | = $___________ in 40 years |

| $__________ | × 18.42 | = $___________ in 50 years |

| $__________ | × 32.99 | = $___________ in 60 years |

Although the cost of purchasing a home generally increases over the years, after you purchase a home, the bulk of your housing costs aren’t exposed to inflation if you use a fixed-rate mortgage to finance the purchase. As we explain in Chapter 6, a fixed-rate mortgage locks your mortgage payment in at a fixed amount (as opposed to an adjustable-rate mortgage payment that fluctuates in value with changes in interest rates). Therefore, only the comparatively smaller property taxes, insurance, and maintenance expenses will increase over time with inflation. (In Chapter 3, we cover in excruciating detail what buying and owning a home costs.)

Читать дальшеИнтервал:

Закладка:

Похожие книги на «Home Buying Kit For Dummies»

Представляем Вашему вниманию похожие книги на «Home Buying Kit For Dummies» списком для выбора. Мы отобрали схожую по названию и смыслу литературу в надежде предоставить читателям больше вариантов отыскать новые, интересные, ещё непрочитанные произведения.

Обсуждение, отзывы о книге «Home Buying Kit For Dummies» и просто собственные мнения читателей. Оставьте ваши комментарии, напишите, что Вы думаете о произведении, его смысле или главных героях. Укажите что конкретно понравилось, а что нет, и почему Вы так считаете.